A continuation certificate bond is the document that keeps an existing surety bond in force for a new term without the cost and paperwork of issuing a brand-new bond. For licensed professionals, contractors, ERISA plan fiduciaries, and others who hold ongoing compliance bonds, understanding this distinction can mean the difference between uninterrupted coverage and an unexpected license suspension.

This article covers what a continuation certificate bond is, how it works, who needs one, and what happens if the deadline slips.

Key Takeaways

- A continuation certificate is issued by the surety company to extend an existing bond into a new coverage term

- All original bond terms and regulations carry over — the continuation certificate holds the same legal weight

- The bond amount does not change when a continuation certificate is issued

- License, permit, and contractor bonds most commonly require continuation certificates to stay compliant

- Missing the filing deadline risks coverage lapses, license suspension, or having to obtain a completely new bond

What Is a Continuation Certificate Bond?

A continuation certificate bond is an official document issued by a surety company that formally extends the coverage of a previously issued surety bond into a new term — without requiring the principal to apply for and execute an entirely new bond.

Every surety bond involves three parties:

- The principal — the bonded party (a contractor, auto dealer, plan fiduciary, etc.)

- The surety — the company issuing the bond

- The obligee — the government agency, licensing board, or organization requiring the bond

The continuation certificate is an agreement between the principal and the surety, which is then submitted to the obligee to confirm uninterrupted coverage.

Legally, a continuation certificate is treated as a bond in its own right. Under 27 CFR § 25.97, the TTB regulatory framework for brewers' bonds states that a continuation certificate "will constitute a bond" and that all laws and regulations applicable to the original bond apply equally to the certificate. That distinction matters when evaluating how it differs from the alternatives obligees may accept:

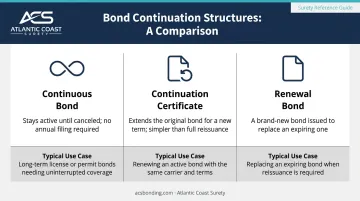

| Structure | How It Works | Typical Use Case |

|---|---|---|

| Continuous bond | Stays active indefinitely until canceled — no annual filing required | Preferred by obligees who want automatic coverage without renewals |

| Renewal bond | A brand-new bond document issued and filed to replace the expiring one | Required when the obligee does not accept continuation certificates |

| Continuation certificate | Extends the original bond for a new term with a simpler document than a full new bond | Used when the obligee accepts certificate-based extensions in lieu of reissuance |

Understanding how these structures differ sets up a practical question: what does the continuation certificate itself actually contain?

What Does a Continuation Certificate Bond Look Like?

A typical continuation certificate includes:

- Bond number and original bond reference

- Principal's name and surety company name

- Obligee identification

- Original bond amount (unchanged)

- New coverage period dates

- Signatures from both the principal and the surety — often executed under penalty of perjury

Filing requirements vary by obligee. The TTB's Form 5130.23, for example, requires two copies with original ink signatures — photocopies are not accepted. Other obligees, such as those using NMLS for mortgage licensees, manage bond continuation electronically through their own systems. Always confirm the obligee's specific requirements before submitting.

How Does a Continuation Certificate Bond Work?

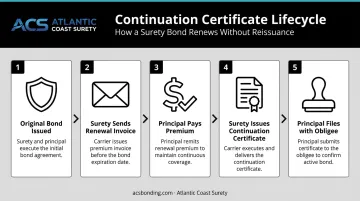

The lifecycle follows a straightforward sequence:

- Original bond is issued with a defined coverage term (typically one year)

- Surety generates a renewal invoice as the expiration date approaches

- **Principal pays the renewal premium** before the deadline

- Surety issues the continuation certificate, extending coverage into the new term

- Principal files the certificate with the obligee before the expiration date

Note that the continuation certificate does not increase the penal sum. If a contractor's license bond was originally written for $25,000, the continuation certificate renews it at $25,000 — the surety's maximum liability stays exactly the same.

Obligee-Directed Filing Rules

The obligee controls how and when you must file. Some require the principal to submit the certificate directly to their office. Others — like NMLS for mortgage licensees — handle it electronically, where the surety submits confirmation on the principal's behalf. The Colorado Auto Industry Division, for instance, specifically requires dealers to provide a surety bond or continuation certificate in the $50,000 amount at renewal.

Filing method depends entirely on the obligee — there is no universal process.

Timing Matters

Most bond professionals recommend renewing at least 30 days before the expiration date — enough lead time for the obligee to receive and process the certificate before coverage lapses. Once the surety issues the continuation certificate, it can typically be delivered to the principal by mail or email. The filing responsibility rests with the principal, not the surety or their agent.

Who Needs a Continuation Certificate Bond?

Not every surety bond requires a continuation certificate. One-time bonds — like a construction performance bond tied to a specific project, or certain court bonds — simply expire at completion. Continuation certificates apply specifically to term-based bonds that must stay active for ongoing compliance.

The bond types most commonly requiring continuation certificates include:

- License and permit bonds: Contractors, auto dealers, mortgage brokers, and other licensed professionals typically hold annual bonds required by state agencies. These must be renewed each year to keep the license active.

- Contractor license bonds — General contractors and specialty tradespeople bonded by state licensing boards need continuous coverage. California's CSLB, for example, requires a contractor bond for issuance, reactivation, and maintenance of an active license.

- ERISA fidelity bonds: Federal law requires fiduciaries of employee benefit plans to maintain bonding coverage. DOL guidance confirms bonds must generally equal 10% of plan assets handled, with a $500,000 maximum (or $1,000,000 for plans holding employer securities). When the bond term expires, coverage must continue without a gap.

- Probate and fiduciary bonds — Court-appointed fiduciaries such as administrators, guardians, and trustees may hold bonds requiring periodic renewal for the full duration of the estate or trust administration — sometimes running three to five years or longer.

Who Is Responsible for Filing?

The principal is always responsible for ensuring the continuation certificate reaches the obligee — even though the surety issues the document. Business owners and contractors should confirm with their agent that filing is handled, not assume it happens automatically.

For businesses holding multiple bonds across several states, tracking continuation certificate deadlines becomes particularly important. A lapse in one bond can affect licensure in multiple jurisdictions simultaneously.

What Happens If You Don't File a Continuation Certificate?

A lapsed bond can trigger cascading problems faster than most contractors expect. California's Contractors State License Board provides one of the clearest examples: if a surety cancels required bond coverage, the CSLB places the contractor's license under bond suspension. If the bond is not received within 90 days of the bond effective date, the ability to retroactively lift the suspension is limited. Operating without a license carries additional consequences — a second offense under California law carries a mandatory 90-day jail sentence and a fine of 20% of the contract price or $5,000, whichever is greater.

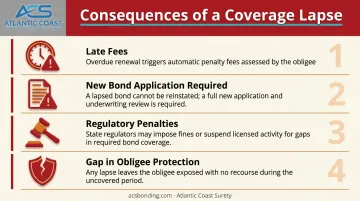

Beyond license suspension, other risks include:

- Late fees imposed by the obligee

- Requirement to apply for a brand-new bond, which may involve fresh underwriting, credit review, and higher premiums

- Regulatory penalties that vary by bond type and jurisdiction

- Gaps in obligee protection, since the surety's liability ends when coverage lapses

Reapplying for a new bond after a lapse means fresh underwriting scrutiny — and potentially higher premiums if your credit profile has changed. Filing a continuation certificate on time sidesteps all of that.

How to Obtain a Continuation Certificate Bond

The process is manageable if you stay ahead of the calendar:

- Mark the expiration date at least 60 days out — earlier for complex bond types

- Pay the renewal invoice from your surety company before the deadline

- Review the continuation certificate once issued for accuracy (bond amount, coverage dates, parties listed)

- File the certificate with the obligee before the expiration date, using the obligee's required method

Working with a specialized surety bond agency — rather than a general insurance broker — saves time and reduces filing errors. A bond-only agency understands obligee-specific filing requirements, tracks renewal timelines across multiple bond types, and has direct carrier relationships to expedite issuance.

Atlantic Coast Surety, based in Mahwah, NJ, is a wholesale surety bond broker with over 20 years of experience across standard and specialty markets. The agency works exclusively with A-rated and T-listed surety providers and carries in-house underwriting authority, which means faster turnaround on qualifying bonds without waiting on individual carrier decisions. Their portfolio covers contractors, ERISA plan sponsors, probate fiduciaries, commercial businesses, and more.

For retail agents and brokers managing clients with ongoing bond obligations, established bond lines at ACS make renewal requests faster and more straightforward. Contact Anthony Spina at aspina@acsbonding.com or 201.661.2381.

Frequently Asked Questions

What is a bond continuation certificate?

A bond continuation certificate is an official document issued by a surety company to extend a previously issued surety bond into a new coverage term. It allows the original bond to remain in force without requiring the execution of a completely new bond.

How does a continuation certificate bond work?

When a term-based bond approaches expiration, the principal pays the renewal premium and the surety issues a continuation certificate. The principal then files that certificate with the obligee before the expiration date to maintain uninterrupted coverage.

What is the difference between a continuation certificate bond and a letter of credit?

A continuation certificate bond is backed by a licensed surety company, so no principal capital is tied up as collateral. A letter of credit requires the business to pledge its own cash or credit line, which can limit borrowing capacity and freeze working capital.

Does a continuation certificate bond change the original bond amount?

No. A continuation certificate renews the bond at the exact same penal sum as the original. The surety's maximum liability remains unchanged throughout the continuation.

How far in advance should I file a continuation certificate?

Most bond professionals recommend renewing and filing at least 30 days before the bond's expiration date. This gives the obligee enough time to process the certificate before coverage lapses.

What happens if I don't file my continuation certificate on time?

A missed deadline causes a lapse in bond coverage, which can trigger license suspension and regulatory penalties. You may also need to apply for and underwrite a brand-new bond, typically at greater time and cost than a timely renewal.