A fiduciary bond is a court-required surety instrument that protects beneficiaries, creditors, and estates if the appointed fiduciary commits fraud, negligence, or misconduct. Without it, you typically can't begin administering an estate or managing someone's assets.

This guide covers everything you need to know: what fiduciary bonds are, who needs one, what they cover, how much they cost, and how to get one.

TL;DR

- A fiduciary bond guarantees a court-appointed individual will perform their duties honestly and faithfully

- Executors, trustees, guardians, and conservators are the most common roles that trigger a bond requirement

- ERISA mandates separate fidelity bonds for anyone handling employee benefit plan assets — federally required, regardless of state law

- Bond premiums vary based on bond amount and the applicant's financial profile — Ohio's published rate of $2.50 per $1,000 of bonded assets is a common benchmark

- The estate can often reimburse the premium as an administrative expense — California Probate Code §8486 explicitly permits this

What Is a Fiduciary Bond and How Does It Work

The Basic Definition

A fiduciary bond — also called a probate bond, estate bond, or court bond — is a written guarantee required by a court that a fiduciary will carry out their duties honestly and in accordance with the law. California's Judicial Council describes it as essentially an insurance policy for estate assets that may be stolen or mismanaged by an administrator or executor.

The bond doesn't protect the fiduciary. It protects the estate and its beneficiaries.

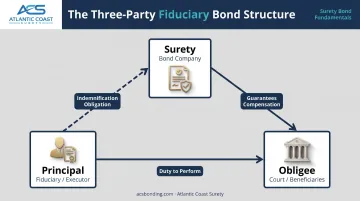

The Three-Party Structure

Every fiduciary bond involves three parties:

- The Principal — the fiduciary (executor, trustee, guardian, etc.) who is required to obtain the bond

- The Obligee — the court or beneficiaries who require and benefit from the bond

- The Surety — the bond company that underwrites and guarantees compensation if the principal breaches their duty

If the fiduciary commits fraud, theft, embezzlement, or acts with gross negligence, the surety compensates the estate or beneficiaries up to the bond amount. The fiduciary is then personally obligated to reimburse the surety — a process called indemnification. Unlike a standard insurance policy, the bond shifts ultimate financial responsibility back to the fiduciary, not the surety.

How Bond Amounts Are Set

Courts calculate the required bond amount based on the assets under the fiduciary's control — not the gross estate value. State statutes govern the specific formula, and approaches vary:

- California (Probate Code §8482): Bond equals estimated personal property value plus probable annual gross income from estate property

- Maryland: Bond is capped at the probable maximum value of personal property during administration

Most states follow comparable logic — tying the bond amount to controllable assets, not total estate value.

Bond vs. Fiduciary Liability Insurance

These two products protect different parties:

| Aspect | Fiduciary Bond | Fiduciary Liability Insurance |

|---|---|---|

| Protects | Estate and beneficiaries | The fiduciary themselves |

| Required by | Court order | Voluntary (not required by courts) |

| Covers | Fraud, theft, misconduct, negligence | Mismanagement claims, administrative errors |

Some fiduciaries carry both — the bond satisfies the court requirement, while the insurance covers their own exposure from lawsuits that don't rise to the level of a bond claim.

Who Needs a Fiduciary Bond

Bond requirements vary by state and by the type of proceeding. Most states require a bond in probate cases — particularly when someone dies without a will or when the will doesn't include a bond waiver. California, for example, requires it by statute: under Probate Code §8480, every appointed personal representative must provide a court-approved bond before letters are issued.

Common Roles That Trigger a Bond Requirement

- Executor or Administrator — managing and distributing a decedent's estate

- Trustee — overseeing assets held in trust

- Guardian — managing finances for a minor

- Conservator — overseeing financial affairs for someone unable to manage them independently

Note: Trustee bonds are not always required. In California, §15602 generally waives the requirement unless the trust instrument or a court specifically mandates one.

According to a 2014 ABA survey — the most recent available national tally, approximately 20 states mandate conservator bonds outright, while 19 require bonds but give courts some discretion. For guardians, 12 states require a bond by statute. State laws change, so verifying current requirements with local counsel or a surety specialist is advisable.

ERISA: A Federal Mandate

Section 412 of ERISA requires every fiduciary of an employee benefit plan — and anyone who "handles" plan funds — to be bonded. This applies to 401(k) plans, pension plans, and other employee benefit arrangements. ERISA bonds are federally required regardless of what state law says, and they're distinct from probate fiduciary bonds.

Court-Ordered Bonds

Beneficiaries or creditors can petition the court to impose a bond requirement even when one wasn't originally mandated — typically when they have concerns about a fiduciary's honesty, financial stability, or judgment. Courts retain discretion to require a bond even after an earlier waiver.

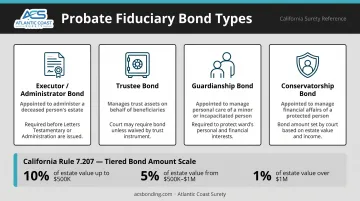

Types of Fiduciary Bonds

Probate Fiduciary Bonds

Probate fiduciary bonds cover four distinct roles, each tied to a specific court-supervised responsibility:

- Executor/Administrator Bond — for individuals managing and distributing a decedent's estate; required in most states absent a will waiver

- Trustee Bond — for trustees managing trust assets; requirement varies by state and trust instrument

- Guardianship Bond — for guardians managing finances for a minor or incapacitated person

- Conservatorship Bond — for conservators overseeing financial affairs for adults unable to care for themselves

California Rule 7.207 provides a useful example of how conservator/guardian bond amounts are calculated: 10% of estate value up to $500,000, 5% of value between $500,000–$1,000,000, and 1% of value over $1,000,000.

ERISA bonds operate under an entirely different framework — federal law rather than state probate courts. Here's how the requirements break down:

ERISA Fidelity Bonds

- Who needs one: Any plan administrator, trustee, or person who "handles" employee benefit plan assets

- Required amount: At least 10% of plan funds handled in the preceding year

- Minimum bond: $1,000

- Maximum required bond: $500,000 (or $1,000,000 for plans holding employer securities)

- Premium structure: Atlantic Coast Surety's ERISA bond rates run from $100 for bonds under $10,000 to $340 for $500,000 bonds, billed on a three-year term — and include an inflation guard endorsement that automatically increases coverage as plan assets grow

- Carriers: Must be obtained from sureties listed on Treasury Department Circular 570

Atlantic Coast Surety places ERISA bonds and probate fiduciary bonds as separate products with distinct underwriting processes. Plan sponsors who hold both roles need both bonds; one does not satisfy the other.

What Fiduciary Bonds Cover — and What They Don't

What's Covered

A fiduciary bond responds to financial losses caused by:

- Fraud and intentional misconduct — theft, embezzlement, forgery, deliberate misappropriation of estate assets

- Negligent acts — careless handling of assets that results in measurable harm to the estate or beneficiaries

Coverage isn't limited to intentional wrongdoing. A fiduciary who loses estate funds through careless management can trigger a valid claim.

What's Not Covered

Bonds don't respond to every complaint. Common exclusions include:

- Good-faith judgment calls — investment strategy decisions, distribution timing, or discretionary choices made honestly and in good faith. The Uniform Prudent Investor Act (adopted in most states) evaluates trustee conduct based on facts at the time of the decision, not hindsight

- Market losses — portfolio declines caused by external market forces, not fiduciary error

- Non-breach disputes — disagreements between heirs or beneficiaries that don't involve actual misconduct

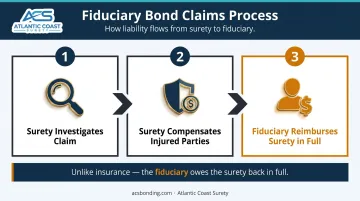

The Claims and Indemnification Process

When a valid claim is filed:

- The surety investigates the claim

- If legitimate, the surety compensates injured parties up to the bond amount

- The fiduciary is personally liable to reimburse the surety in full

That third step is what separates a fiduciary bond from insurance. As the SFAA Surety Claims Guide puts it, the principal must reimburse the surety for any loss suffered by extending surety credit. A paid claim means the fiduciary owes the surety that money back — in full — making this a direct personal financial consequence, not a covered loss.

How Much Does a Fiduciary Bond Cost

Pricing Structure

Fiduciary bond premiums are calculated as a percentage of the total bond amount. A practical benchmark: CBA Law's Ohio probate bond schedule shows a general rate of $2.50 per $1,000 of bonded assets, with a minimum bond amount of $40,000 costing $100. For bonds over $500,000, the rate decreases on a sliding scale, so larger estates pay a lower effective percentage on incremental coverage.

Example: A $200,000 probate bond at $2.50 per $1,000 = $500 annual premium.

Factors That Influence Your Rate

- Bond amount — larger bonds benefit from lower effective rates on the incremental coverage

- Credit history — the applicant's personal credit profile is a key factor in rate determination

- Bond type — ERISA bonds, executor bonds, and conservatorship bonds each have different risk profiles

- Risk factors — Atlantic Coast Surety's underwriting evaluates prior felony convictions, previous bond claims, existing suits or liens, dissension among heirs, and whether an attorney remains involved through bond discharge

Annual Renewal and Reimbursement

Probate bonds are typically issued for one-year terms, renewed annually, and remain in force until the court officially releases the bond. Neither the principal, agent, nor surety can cancel without court approval.

The fiduciary pays the premium out of pocket initially, but it is often a reimbursable expense — many jurisdictions allow the estate to cover this as a legitimate administrative cost. California Probate Code §8486 explicitly allows the personal representative to recover the reasonable bond cost for every year it remains in force.

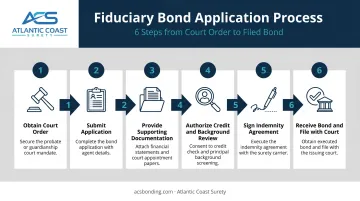

How to Get a Fiduciary Bond

Step-by-Step Application Process

- Obtain your court order — get the court paperwork specifying the bond requirement and the required bond amount

- Submit a completed application — provide personal information including full name, Social Security number, address, and contact details

- Provide supporting documentation, which typically includes:

- Complete copy of all court documents and the specific bond form required

- Estate assets breakdown (cash, stocks, personal property, real estate)

- Estate liabilities (mortgages, debts)

- Personal financial statement

- Information about number of heirs and their relationship to the deceased/ward

- Attorney involvement details

- Authorize credit and background review — the surety will review your credit history and may ask about prior felony convictions, previous bond claims, or existing judgments

- Sign the indemnity agreement — must be witnessed by an independent party (not a spouse or family member)

- Receive the bond and file with the court — once issued, the bond is presented to the court to authorize you to proceed

Issuance Timeline

Standard probate bonds can often be issued within 24 hours for straightforward cases. Complex situations — larger bond amounts, estates with active litigation, dissension among heirs, or going businesses in the estate — take longer. Once a complete application is submitted, a provider with court bond experience can give you a realistic timeline estimate specific to your situation.

Working with a Specialized Provider

Atlantic Coast Surety, a bond-only agency with 20+ years of experience, places fiduciary bonds for probate fiduciaries and ERISA plan sponsors through A-rated, T-listed carriers. Their ERISA bond program runs through NGM Insurance Company (and Spring Valley Mutual in Minnesota), with in-house underwriting authority that can accelerate approvals compared to routing through a generalist insurer unfamiliar with court bond requirements.

For attorneys managing multiple probate matters or agents placing bonds on behalf of fiduciary clients, a wholesale specialist with dedicated court bond expertise and established carrier relationships typically produces faster approvals and better pricing. Generalist insurers unfamiliar with court bond requirements add friction that a specialist avoids by design.

Frequently Asked Questions

What is a fiduciary surety bond and how does it differ from other surety bonds?

A fiduciary bond is a court-required surety instrument guaranteeing that an appointed fiduciary will fulfill their duties faithfully. Unlike contract or license bonds — which cover construction performance and regulatory compliance — fiduciary bonds operate in a judicial or probate context, protecting beneficiaries and estates from misconduct or negligence.

What is the purpose of a fiduciary bond?

The purpose is to protect estates, trusts, and beneficiaries from financial harm caused by a fiduciary's fraud, negligence, or misconduct. It gives courts assurance that appointed individuals — who often have unsupervised access to significant assets — will manage them responsibly on behalf of those they serve.

How much does a fiduciary surety bond cost?

Premiums are calculated as a percentage of the bond amount. Ohio's published benchmark is $2.50 per $1,000 of bonded assets, with a sliding scale for larger bonds. Your credit history, the type of fiduciary role, and specific risk factors in the estate all influence the final rate.

Who pays for a fiduciary bond?

The fiduciary purchases and pays the premium. However, in many probate jurisdictions — including California under Probate Code §8486 — the estate can reimburse this cost as a legitimate administrative expense.

Can a fiduciary bond requirement be waived?

Yes, in many states. A bond can be waived if the testator explicitly included a waiver in their will, if all beneficiaries consent in writing, or if the court exercises its discretion. However, courts can still require a bond for good cause even after a waiver — and waiving the bond removes all financial protection for beneficiaries.

Is an ERISA bond the same as a fiduciary bond?

ERISA bonds are a specialized subcategory of fiduciary bond, federally mandated under the Employee Retirement Income Security Act for anyone who handles employee benefit plan assets. They share the three-party surety structure but carry distinct federal requirements: minimum coverage of 10% of plan assets handled, a $500,000 cap (or $1,000,000 for plans holding employer securities), and mandatory placement through Treasury-listed carriers.