Missing this requirement doesn't just delay the process. In most states, the guardianship appointment cannot be finalized without it.

This article covers everything you need to know: what a guardianship bond is, why courts require it, when it applies, what it costs, and how to get one.

TL;DR

- A guardianship bond is a surety bond (not insurance) that protects a ward's financial assets from guardian mismanagement or fraud

- It's a three-party agreement: the guardian, the court, and the surety company

- Courts require it before a guardian can legally manage a ward's estate

- Annual premiums typically range from 0.5% to 3% of the court-set bond amount

- Guardians with poor credit may face higher rates or difficulty qualifying

What Is a Guardianship Bond?

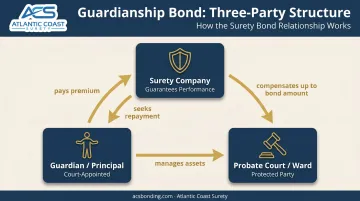

A guardianship bond is a type of surety bond that a court-appointed guardian must obtain before managing a ward's finances or assets. It is a legally binding, three-party agreement involving:

- The guardian (principal) — the person appointed by the court

- The probate court or protected individual (obligee) — the party the bond protects

- The surety company — which guarantees the guardian's performance

The surety company doesn't just issue a piece of paper. It stands behind the guardian's obligation to fulfill their court-ordered duties. If the guardian misappropriates funds, neglects responsibilities, or commits fraud, a claim can be filed against the bond. The surety compensates the ward up to the bond amount. From there, the surety seeks full repayment from the guardian personally.

Guardianship of the Estate vs. Guardianship of the Person

There are two categories of guardianship, and the bond requirement applies almost exclusively to one of them:

- Guardianship of the estate — the guardian manages the ward's financial assets and property. A bond is typically required.

- Guardianship of the person — the guardian oversees personal care decisions (housing, medical). No money management means no bond requirement in most states. Ohio Revised Code Section 2109.04, for example, confirms that guardians of the person typically do not need to post bond unless the court finds specific cause.

The Key Distinction: Bond vs. Insurance

A guardianship bond is not insurance — a distinction that matters. Insurance protects the policyholder. A surety bond protects the ward. If a valid claim is paid out, the guardian is personally obligated to reimburse the surety — making this a financial accountability tool, not a safety net for the guardian.

Guardianship bonds fall within the broader fiduciary and probate bond category, alongside conservatorship bonds, administrator bonds, and executor bonds. Understanding where guardianship bonds fit within this family helps clarify what courts expect — and what happens when those expectations aren't met.

Why a Guardianship Bond Matters

Wards — minors and incapacitated adults alike — have no way to protect their own financial interests in court. A guardianship bond exists to do that for them, holding the guardian financially accountable for every decision made with the ward's assets.

The scale of the problem this addresses is significant. FinCEN reported that financial institutions filed 155,415 Bank Secrecy Act reports tied to elder financial exploitation over the one-year period ending June 2023, involving approximately $27 billion in suspicious activity — with roughly 20% of cases involving theft by trusted persons. Guardians fall directly into that "trusted person" category.

What the Bond Actually Does

The bond requirement creates a real accountability layer:

- Guardians must keep accurate financial records

- Courts require regular reporting on the ward's estate

- Misconduct can trigger a bond claim — and personal financial liability

That last point is where the bond's deterrent value lives. A guardian who knows they will personally owe the surety company for any validated claim has a direct financial reason to manage the ward's estate responsibly.

Consequences of Not Having a Bond

Failing to obtain a required guardianship bond has real legal consequences:

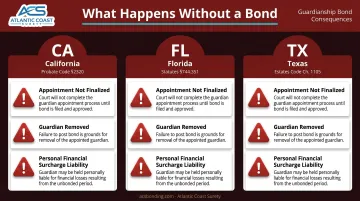

- California Probate Code Section 2320 requires a guardian to file bond before the court issues letters of guardianship

- Florida Statutes Section 744.351 requires bond before the guardian exercises any authority

- Texas Estates Code Chapter 1105 requires a guardian of the estate to post bond before letters issue, unless exempt

When a guardian fails to post bond or is denied, the consequences follow quickly. Courts can refuse to finalize the appointment, remove the guardian entirely, or impose personal financial liability — known as a surcharge — under statutes like Florida Statutes Section 744.446.

When Is a Guardianship Bond Required?

Guardianship of a Minor

When a minor inherits money, receives an insurance settlement, or holds other financial assets, the court typically requires the appointed guardian to post a bond before managing those funds. The larger the estate, the more critical the bond becomes.

Even when parents have a will designating a guardian, some courts still require a bond — unless the will explicitly waived it. California Probate Code Section 2324 permits waiver when the nominating party waived bond, but the court retains discretion to require one anyway.

Guardianship of an Incapacitated Adult

When an adult is legally deemed incapacitated — due to dementia, severe disability, or mental illness — and a guardian is appointed to manage their finances, a bond is typically required. Incapacitated adults frequently hold substantial assets — retirement accounts, real property, Social Security income, and pensions — making financial oversight through a bond especially important.

Maryland's court guidelines note that bond may be required when a disabled person's property is valued at more than $10,000. That low threshold reflects how broadly courts apply the requirement.

When Can the Requirement Be Waived?

Courts in some states have discretion to waive or reduce the bond requirement under specific conditions:

- The ward's assets are minimal

- Funds are placed in a restricted, court-supervised bank account (which may reduce or eliminate the required bond amount)

- The ward's own legal documents explicitly waived the bond

- The guardian demonstrates other compelling reasons to the court's satisfaction

Both California (Probate Code Section 2321) and Florida (Statutes Section 744.351) allow courts to waive or reduce bond for good cause. Requirements vary significantly by state, so confirming local probate court rules is essential.

How Much Does a Guardianship Bond Cost?

Bond Amount vs. Premium — Two Different Numbers

Guardians often encounter two separate figures when applying for a bond — and confusing them leads to budget miscalculations:

- Bond amount — the total coverage set by the court, based on the ward's assets. This is what the surety guarantees.

- Bond premium — the annual cost the guardian actually pays. This is a percentage of the bond amount.

These are not the same figure, and confusing them leads to serious budget miscalculations.

How the Bond Amount Is Calculated

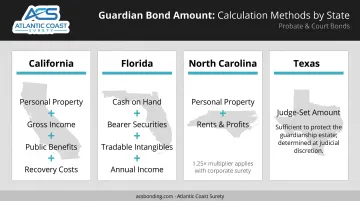

Bond amount formulas vary by state. A few examples:

| State | Bond Amount Basis |

|---|---|

| California | Personal property + probable annual gross income + public benefits income + recovery cost estimate |

| Florida | At minimum: cash on hand, bearer securities, readily tradable intangibles, and annual income |

| North Carolina | Personal property + rents/profits; corporate surety may require 1.25x; over $100,000, court may accept 110% |

| Texas | Judge sets amount sufficient to protect the guardianship and creditors; reduced if cash/securities deposited under court order |

Real estate is generally excluded from the formula unless the guardian has authority to sell it.

What You'll Actually Pay

Guardianship bond premiums generally start at around 0.5% for the first $250,000 of coverage, according to SuretyBonds.com, with larger or riskier estates running 0.75% to 2% or more. An illustrative range of 0.5% to 3% covers most standard cases, though individual rates depend on the guardian's credit history and financial standing.

Practical examples:

- $10,000 bond at 0.5%–3% = $50 to $300 per year

- $50,000 bond at 0.5%–3% = $250 to $1,500 per year

The bond must stay active for the duration of the guardianship, and renewal premiums are due until the court officially discharges the bond. This is an ongoing cost, not a one-time expense.

How to Obtain a Guardianship Bond

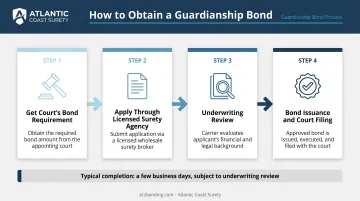

The process follows a consistent sequence:

- Get the court's bond requirement — the court order or letters process determines whether a bond is required and specifies the amount. Do not skip this step; you need the court's number before approaching a surety.

- **Apply through a licensed surety agency** — provide personal financial information and documentation about the ward's estate. Atlantic Coast Surety's probate bond application, for instance, collects estate asset breakdowns (cash, stocks, personal property, real estate), estate liabilities, the applicant's relationship to the ward, and underwriting disclosures covering prior criminal history, bankruptcy, and prior bond claims.

- Underwriting review : the surety evaluates credit history, financial standing, background, and risk factors specific to the estate. Maryland's court guidance confirms that qualification depends on credit rating, income and resources, debts, and bankruptcy history.

- Bond issuance and court filing : once approved, the bond is signed and filed with the probate court before the guardianship is officially activated. California requires this before letters of guardianship issue; Florida requires it before the guardian exercises any authority.

What Can Complicate Approval

Guardians with poor credit, prior financial misconduct, or a bankruptcy history may face higher premiums or difficulty qualifying outright. If bonding proves difficult, the guardian's obligation is to notify the court immediately so the court can adjust the arrangement or redirect the appointment accordingly.

Not all surety agencies handle fiduciary and probate bonds. This is a specialized area requiring experience with court-specific requirements, state-by-state statutory differences, and the underwriting factors unique to estate management.

Atlantic Coast Surety, a bond-only agency with over 20 years of experience and access to A-rated, T-listed providers, focuses specifically on this type of placement, covering both minor and adult guardianship bonds. In-house underwriting authority allows for faster decisions on qualifying applications.

Frequently Asked Questions

Frequently Asked Questions

Why does a guardian need to be bonded?

Courts require guardians to post bond to protect the ward's financial assets from mismanagement, negligence, or fraud. Because wards — whether minors or incapacitated adults — cannot legally protect their own financial interests, the bond serves as a court-enforced accountability mechanism.

How much do you have to pay for a $10,000 guardianship bond?

The annual premium on a $10,000 guardianship bond typically falls between $50 and $300, based on a 0.5%–3% rate range. The exact figure depends on the guardian's credit history, financial profile, and the surety's underwriting assessment.

How much is the bond for guardianship in Texas?

Under Texas Estates Code Chapter 1105, the judge sets the bond amount in a sum sufficient to protect the guardianship and its creditors. The guardian then pays an annual market-rate premium (a percentage of that court-set amount) to the surety company. There is no fixed state premium rate; it varies by underwriter.

Can a guardianship bond requirement be waived?

Yes, in some states. Courts may waive bond when the estate is minimal, funds are placed in a restricted account, or the ward's own legal documents included a bond waiver. This is not automatic: it must be specifically requested and approved by the court.

What happens if a guardian mismanages the ward's assets?

An affected party can file a claim with the surety company. If validated, the surety compensates the ward up to the bond amount, and the guardian is personally obligated to reimburse the surety in full.

How long does it take to get a guardianship bond?

Straightforward cases with clean credit are often approved within a few business days. Complex estates or credit issues can extend the timeline, so submitting all court documents and estate details upfront keeps the process moving.