Introduction

Being named executor or administrator of an estate comes with real responsibility — and a requirement most people never see coming. Before the probate court grants you authority to act, you'll likely need to obtain a probate bond.

Most people encounter this requirement without knowing what a surety bond is, who issues one, or what it costs. At an already stressful time, it can feel like an unexpected obstacle.

This guide cuts through the confusion. It covers:

- What a probate bond is and how it works

- Who is required to get one

- How costs are calculated

- How to obtain a bond

- What happens if the bond lapses or a claim is filed

TL;DR

- A probate bond protects estate beneficiaries if the personal representative mismanages or misappropriates estate assets.

- Three parties are involved: the personal representative (principal), the court/beneficiaries (obligee), and the surety company guaranteeing the bond.

- The court sets the bond amount based on estate value; the representative pays only a small premium, typically a percentage of that total.

- That premium is usually reimbursable from estate assets, so the representative rarely bears it out of pocket.

- Courts can waive the bond in some cases, but it stays in force until the court formally discharges the personal representative.

What Is a Probate Bond and How Does It Work?

A probate bond — also called a fiduciary bond or executor's bond — is a court-required surety bond guaranteeing that a personal representative (executor or administrator) will faithfully carry out their legal duties in managing and distributing an estate.

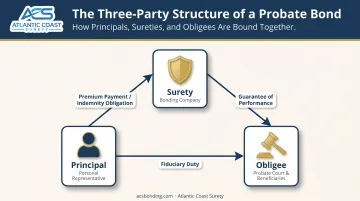

The Three-Party Structure

Unlike insurance, a surety bond involves three distinct parties:

- Principal — the personal representative required to obtain the bond

- Obligee — the probate court and estate beneficiaries who are protected

- Surety — the bonding company that guarantees the principal's performance

The Surety & Fidelity Association of America (SFAA) defines a surety bond as a written, legally required, three-party agreement — and classifies fiduciary bonds as those furnished by fiduciaries to comply with court orders and statute.

The Indemnity Obligation

Unlike insurance, a probate bond carries a repayment obligation: if the surety pays a claim to beneficiaries because of the executor's misconduct, the personal representative is personally obligated to repay the surety. The bond is a financial accountability tool, not a passive safety net.

What the Bond Covers

According to the American Bar Association's The Law of Probate Bonds, covered conduct includes:

- Theft, embezzlement, or misappropriation of estate funds

- Self-dealing or conflicts of interest

- Improper expenditures or distributions

- Failure to marshal estate assets properly

- Accounting errors and negligent asset management

That coverage stays in effect for the full duration of the executor's appointment.

When the Bond Is Active

The bond takes effect when the court issues Letters Testamentary or Letters of Administration — and remains in force until the court formally discharges the personal representative. Under California Probate Code Section 8480, for example, a bond must be given before letters issue. Requirements vary by state, so confirming local rules before filing is essential.

Who Needs a Probate Bond?

Bond requirements vary by state and by the specifics of each estate. Here's a practical breakdown.

Fiduciaries Who May Be Required to Bond

- Executors named in a will

- Administrators appointed when there is no will (intestate estates)

- Guardians of minors or incapacitated adults

- Conservators managing assets for incapacitated individuals

- Trustees in certain court-supervised arrangements

Atlantic Coast Surety places bonds for all of these roles, including temporary, permanent, successor, and additional bonds.

Circumstances That Typically Trigger a Requirement

Even when a will is silent on the bond, courts often require one when:

- The executor lives out of state (New Jersey Revised Statutes Section 3B:15-1 specifically requires nonresident executors to provide bond unless the will states otherwise)

- The estate is high-value, creating greater risk to beneficiaries

- The will is contested

- A creditor or interested party with a claim over $1,000 demands one (Minnesota Statutes Section 524.3-605)

- The originally named executor cannot serve and a substitute is appointed

Not every estate triggers a bond requirement, though. Courts also have defined pathways for waiving it.

When Courts May Waive the Bond

Three scenarios commonly allow a waiver:

- Will waiver — the decedent explicitly waived the bond requirement in the will

- Beneficiary waiver — all adult beneficiaries sign a written waiver filed with the court

- Corporate fiduciary — a bank or trust company acting as personal representative

Even with a valid waiver, courts retain discretion to require a bond. California Probate Code Section 8481 allows the court to impose a bond requirement "for good cause" regardless of the waiver.

Failing to secure a required bond has immediate consequences. The court will not issue Letters Testamentary or Letters of Administration, meaning the representative cannot legally collect assets, sell property, or act on behalf of the estate.

How Probate Bond Amounts and Costs Are Calculated

How Courts Set the Bond Amount

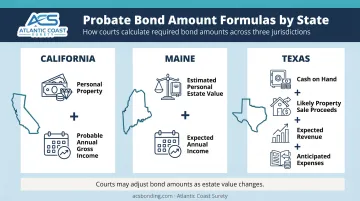

The bond amount is not arbitrary — it follows a statutory formula tied to estate value. Three common frameworks:

| Jurisdiction | Bond Amount Formula |

|---|---|

| California (§ 8482) | Estimated personal property + probable annual gross income; may include real property equity if representative has authority to sell |

| Maine (Title 18-C § 3-604) | Estimated personal estate value + income expected from personal and real estate in the next year |

| Texas (§ 305.153) | Cash on hand + likely cash from property sales + expected revenue next 12 months + anticipated expenses |

Courts can adjust the bond amount up or down as the estate's value changes during administration.

The Premium: What the Representative Actually Pays

The personal representative does not pay the full bond amount — they pay a premium, which is a percentage of the total bond amount. According to SuretyBonds.com:

- 0.5% for the first $250,000 of coverage

- 0.75% to 2% or more for larger estate values

Illustrative example: A $500,000 bond at a 0.5% rate would cost approximately $2,500 in premium. Actual rates vary based on underwriting, state, and individual factors.

What Affects Your Premium Rate

Atlantic Coast Surety's underwriting review evaluates:

- Personal credit history and financial stability

- Prior bond claims filed or paid

- Suits, liens, or judgments against the applicant

- Prior custody of estate or ward's assets

- Felony convictions or crimes involving dishonesty

- Dissension among heirs or beneficiaries

- Whether an attorney remains involved through discharge

- Court-required annual or biannual accounting

A straightforward application — creditworthy applicant, no prior claims, attorney involved, no heir conflict — will typically secure a lower rate. Complex or contested estates trend toward the higher end.

Who Ultimately Pays

The personal representative pays the premium upfront, but this cost is reimbursable from estate assets as a standard administration expense. The probate bond premium is generally treated as a reimbursable administrative cost subject to court approval, so the estate bears the cost, not the executor personally.

One important caveat: the premium is non-refundable once the bond period begins. If the bond is cancelled before a renewal period starts and was never filed with the court, a partial refund may be available depending on the surety's terms.

How to Obtain a Probate Bond

The Application Process

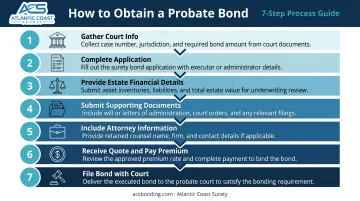

Obtaining a probate bond involves several steps, and preparation speeds the process:

- Gather court and case information — court name and county, docket number, effective date, bond amount, and the name of the deceased or ward

- Complete the bond application — this includes personal information (full name, SSN or FEIN, address, contact details), current occupation, and relationship to the deceased or ward

- Provide estate financial details — a breakdown of assets (cash, stocks, personal property, real estate) and liabilities (mortgages, credit cards, other debts), plus the number of heirs

- Submit supporting documents — a complete copy of all court documents, the bond form the court requires (if any), and a copy of the will or trust if one exists

- Include attorney information — the attorney's name, firm, address, and contact details are required as part of the submission

- Receive a quote and pay the premium — upon underwriting approval, the surety issues the bond document

- File the bond with the probate court — Letters are issued once the filed bond is confirmed

Atlantic Coast Surety's application also requires a witness signature from an independent party — not a spouse or family member. If a business entity is the applicant, the president or authorized officer must sign, and personal indemnity from the owner may be required.

Working with a Specialized Bond Provider

Atlantic Coast Surety operates as a wholesale surety bond broker with in-house underwriting authority. For probate bonds, that structure shortens the approval timeline. Underwriting decisions happen in-house rather than moving through an external carrier's queue, so turnaround estimates are available as soon as the application is complete.

For complex estates where premium costs are significant, working through a bond-only agency with access to multiple A-rated and T-listed surety markets means competitive pricing across carriers, not just one company's rate. One additional factor worth confirming early: courts require bonds from carriers approved to write surety business in that jurisdiction, so verifying carrier eligibility before filing prevents unnecessary delays.

What Happens When a Probate Bond Lapses or a Claim Is Filed?

Consequences of Non-Payment or Bond Lapse

Failing to maintain an active bond is not a minor paperwork issue — courts treat it as disqualifying. Under Minnesota Statutes Section 524.3-605:

- Once a bond demand is made, the representative may not exercise powers (except to preserve the estate) until a bond is filed or excused

- Failure to provide suitable bond within 30 days of notice is cause for removal and appointment of a successor

California Probate Code Section 8480 separately prevents Letters from issuing at all until a required bond is given. The practical result: no bond, no legal authority to manage the estate.

The Claims Process

When a bond is in place, anyone harmed by a breach of fiduciary duty has recourse. Potential claimants — as identified in the ABA's The Law of Probate Bonds — include:

- Beneficiaries and heirs

- Creditors of the estate

- Successor representatives

- Wards (in guardianship contexts)

Under South Carolina law, sureties are jointly and severally liable with the personal representative unless the bond terms state otherwise. That liability can be enforced directly in the probate proceeding.

Reimbursement obligation: When the surety pays a valid claim, the personal representative owes full reimbursement. This indemnity structure is why the bond functions as accountability — not protection — for the executor.

Statute of Limitations on Claims

Timeframes vary by state. Two verified examples:

- California (§ 8488) — no action against sureties unless filed within 4 years from the representative's discharge/removal or final surcharge order, whichever is later; fraud claims run 4 years from discovery

- South Carolina (§ 62-3-606) — no surety proceeding may proceed if the action against the primary obligor is already barred by adjudication or limitation

Always confirm the applicable statute of limitations with an attorney in the relevant jurisdiction.

Frequently Asked Questions

What is the meaning of a probate bond?

A probate bond is a court-required surety bond ensuring that an estate's personal representative faithfully carries out their fiduciary duties — collecting assets, paying debts, and distributing the estate according to law. It protects beneficiaries from financial loss caused by the representative's mismanagement or misconduct.

Who pays for a probate bond?

The personal representative pays the premium upfront. That cost is typically reimbursable from estate assets as a standard administration expense, so the estate effectively absorbs the cost rather than the executor personally.

Do you get probate bond money back?

The premium is generally non-refundable once the bond period begins, though a partial refund may apply if the bond is cancelled before renewal and was never filed with the court. The full bond amount is only paid out if a valid claim occurs.

What happens if a probate bond is not paid?

The court will decline to issue or renew Letters Testamentary or Letters of Administration and may remove the representative from their role. They have no legal authority to manage the estate until a valid bond is reinstated.

Can a probate bond requirement be waived?

Yes, if the will explicitly waives it or all adult beneficiaries sign a written waiver filed with the court. The judge still retains discretion to require a bond if concerns about the representative's conduct arise.

How long does a probate bond last?

A probate bond remains in effect for the entire duration of estate administration — from Letters issuance until the court discharges the personal representative. Depending on estate complexity, that can range from several months to several years.