This guide explains what a non-resident executor bond is, which states require one, how much it costs, and how to get one — including when the requirement can be waived.

Key Takeaways

- Expect to post a surety bond as an out-of-state executor — even when a local executor in the same role would be exempt

- Probate courts set bond amounts — typically equal to, or up to double, the estate's personal property value

- Annual premiums are a percentage of the bond amount, based on underwriting factors

- Bond rules are governed by the state where probate is filed, not where you live

- Waivers are possible but rarely granted — courts require strong justification before waiving the bond for out-of-state executors

What a Non-Resident Executor Bond Is and Why It Exists

A non-resident executor bond (sometimes called a foreign executor bond or probate fiduciary bond) is a court-required financial guarantee. Before an out-of-state executor can legally manage or distribute estate assets, the probate court requires this bond as proof that they'll fulfill their duties faithfully.

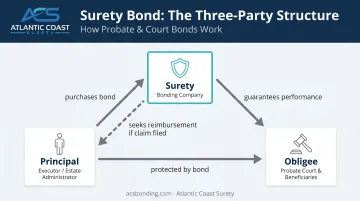

The Three-Party Structure

This is not insurance for the executor. It's a three-party surety agreement that protects the estate's beneficiaries and creditors:

- Principal — the executor who purchases the bond

- Obligee — the probate court and beneficiaries protected by it

- Surety — the bonding company that guarantees the executor's performance

If a valid claim arises (for example, an executor misappropriates estate funds), the surety pays harmed parties and then seeks reimbursement from the executor personally.

Why Courts Treat Out-of-State Executors Differently

The core problem is jurisdictional. A probate court has limited ability to compel a non-resident's appearance, enforce judgments across state lines, or monitor day-to-day estate management from a distance. North Carolina's courts state it plainly: out-of-state executors generally must pay a bond to protect creditors and heirs from potential losses.

The bond covers losses from:

- Misappropriation or theft of estate assets

- Failure to pay valid debts, taxes, or expenses

- Improper or inequitable distribution to beneficiaries

- General mismanagement of estate affairs

Non-Resident vs. Foreign National Executors

These aren't the same thing. A non-resident executor is simply someone who lives outside the probate state. A foreign national is a non-U.S. citizen — and citizenship is generally not the legal disqualifier.

What matters is residency status and the ability to fulfill fiduciary duties within the U.S. probate system. New York, for example, restricts "non-domiciliary aliens" specifically unless they serve alongside a New York resident co-fiduciary.

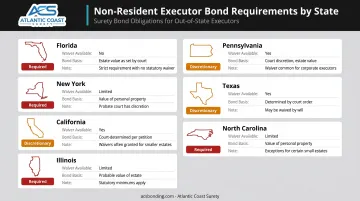

Which States Require Bonds for Non-Resident Executors

Bond requirements are set by the state where probate is filed, not where the executor lives. Most states either mandate bonds for non-resident executors automatically or give courts broad discretion to require them, even when the will attempts a waiver.

State-by-State Overview

| State | Non-Resident Bond Rule | Waiver Allowed? | Bond Amount Basis |

|---|---|---|---|

| Florida | Non-domiciliaries face strict eligibility limits (Fla. Stat. 733.304); bond required under 733.402 unless waived | Will or court waiver possible; resident agent also required | Court-set |

| New York | Non-domiciliary executors subject to SCPA 710 bond treatment; non-domiciliary aliens restricted under SCPA 707 | Limited waiver routes | Personal property + 18 months gross rents |

| California | Bond required before letters issue; court may require bond for non-residents despite will waiver (Prob. Code 8571) | Will and beneficiary waivers allowed, but court can override | Personal property + annual gross income |

| Illinois | Court may require non-resident executor bond despite will waiver (755 ILCS 5/6-13(d)); executor must be U.S. resident | Will may excuse bond, but court discretion overrides | 2x personal estate (individual surety); 1.5x with surety company |

| Pennsylvania | Bond generally required; exceptions exist when a resident co-representative holds all assets (20 Pa. C.S. 3174) | Conditional — not a blanket waiver | Considers personal estate value under representative control |

| Texas | Non-residents disqualified without a resident agent (Tex. Est. Code 304); bond required for qualification | Limited | Personal property + 12 months estimated revenue |

| North Carolina | Out-of-state executors generally must post bond before letters (G.S. 28A-8-1) | Statutory exceptions apply | Court-set |

Always verify current statutes with a local probate attorney — rules change and vary by county court practice.

The Resident Agent Requirement

Several states go further than just requiring a bond. Florida (Probate Rule 5.110) and Texas (Estates Code 304) both impose a resident agent requirement on top of the bond obligation. Before a court issues letters testamentary in these states, non-resident executors must:

- Designate a local resident agent (typically an attorney) to receive legal notices on their behalf

- Obtain a qualifying bond in the amount set by the court

Multi-State Estates and Ancillary Probate

If the decedent owned real property in multiple states, ancillary probate may be required in each state where real property is located. Each state's bond rules apply independently. A bond obtained in the primary probate state does not carry over. Separate bonds are typically required for each jurisdiction where ancillary probate is filed.

How Bond Amounts and Costs Are Determined

How Courts Set the Bond Amount

The probate court sets the bond amount — called the penal sum — based on the estate's value. There is no single national formula. Common approaches include:

- Equal to the personal property value plus estimated annual income (California, Texas)

- Personal property plus 18 months of rents (New York)

- Up to double the personal estate value — Illinois requires 2x with individual sureties, 1.5x with a surety company

- Some states consider only in-state probate assets when calculating the amount

The bond amount represents the maximum coverage, not what you pay out of pocket.

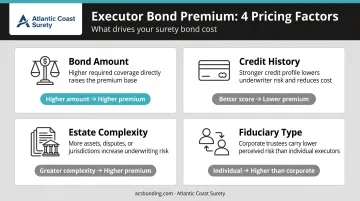

What You'll Actually Pay: The Premium

You pay an annual premium, a percentage of the total bond amount, until the estate is settled. The rate is determined by underwriting factors including the bond amount, credit profile, and estate complexity. Actual pricing varies by surety and applicant profile.

Factors that affect your premium:

- Total bond amount: larger estates may have tiered rates that decrease at higher thresholds

- Credit history: most sureties run a credit check, and stronger credit typically means lower rates

- Estate complexity: ongoing businesses, disputed assets, or multiple beneficiaries can affect pricing

- Individual vs. corporate fiduciary: corporate trustees typically qualify under different underwriting criteria

Premiums are generally reimbursable from the estate as a legitimate administration expense, with court approval.

How to Obtain a Non-Resident Executor Bond

The sequence matters. Courts issue letters testamentary — your legal authority to act — only after you've qualified, which includes posting any required bond.

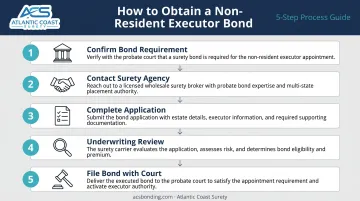

Step-by-Step Process

Confirm the bond requirement and amount with the probate court where the estate is filed. Obtain the court order or petition documents specifying the required bond amount and any court-mandated bond form wording.

**Contact a licensed surety bond agency** that specializes in probate and fiduciary bonds. Atlantic Coast Surety has placed court and probate bonds — including executor bonds — for over 20 years through A-rated and T-listed carriers. We can confirm upfront whether your situation falls within our in-house underwriting authority, which typically accelerates approval timelines.

Complete the bond application. Expect to provide:

- Full personal information (name, address, SSN or FEIN)

- A complete copy of court documents

- Estate asset breakdown: cash, stocks, personal property, real estate values

- Estate liabilities

- Number of heirs and your relationship to the deceased

- Disclosure of any prior bond claims, felony convictions, liens, or judgments

- Copy of the will or trust, if applicable

Underwriting review. Most probate bonds for non-resident executors involve a credit review. Approval timelines vary — simpler estates with clean credit histories move faster. Allowing adequate review time reduces the risk of declination; rushed underwriting on complex estates rarely works in the applicant's favor.

File the bond with the court. Once the surety issues the bond document, file it with the probate court. Letters testamentary are issued after this step is complete.

Ongoing Obligations

The bond stays active until the estate is fully administered and the court formally discharges it. Key obligations during that period include:

- Annual renewals — missing a renewal creates a lapse that can suspend your legal authority as executor

- Personal liability exposure — a lapsed bond leaves you unprotected against surety-backed claims

- Coverage adjustments — if the court uncovers additional assets and revises the required bond amount, you'll need to update coverage accordingly

Can You Waive or Reduce the Bond Requirement?

Grounds for Full Waiver

Waivers are possible but not guaranteed, especially for non-residents. Common grounds:

- Will-based waiver — the will explicitly waives the bond, and the state permits that waiver for non-residents. California (Prob. Code 8571) and Illinois (6-13(d)) both allow courts to override will waivers for out-of-state executors; Florida and Maryland recognize will waivers but carry the same court override authority.

- Beneficiary consent — in California (Prob. Code 8481), all adult beneficiaries can sign written waivers attached to the petition. This route is state-specific and doesn't apply universally.

- Statutory exemptions exist in select states — Pennsylvania, for example, allows a no-bond exception when a resident co-representative holds all estate assets (20 Pa. C.S. 3174). Sole-beneficiary status may qualify in others.

Grounds for Reduction

When a full waiver isn't available, reduction is the next option. Courts will consider lowering the bond amount when:

- All estate debts and creditors have been fully paid

- Estate value falls below a statutory threshold

- Assets are held in restricted accounts that limit the executor's unilateral access

- A resident co-fiduciary is named

Reduction requires a motion, potential court hearing, and supporting evidence — a process that can itself take weeks.

Practical Advice

Even when a waiver appears available, probate courts exercise wide discretion with non-resident executors — don't assume approval. The safest approach is to consult a local probate attorney about the waiver strategy while pursuing the bond application in parallel. If the waiver is denied, you'll have lost nothing. If it's granted, you cancel the bond. Either way, the estate keeps moving.

Frequently Asked Questions

Can a non-U.S. citizen be an executor?

U.S. citizenship is generally not required, but executors must be of legal age, have legal capacity, and not be a convicted felon. Non-citizen non-residents often face added court scrutiny and bond requirements — New York, for example, restricts "non-domiciliary aliens" unless paired with a local co-fiduciary. Verify the specific rules with a local probate attorney.

How much does a foreign executor bond cost?

The annual premium for a non-resident executor bond is a percentage of the required bond amount, determined by underwriting factors including your credit profile and the underwriting surety. Atlantic Coast Surety offers competitive rates through A-rated and T-listed providers. Premiums are paid annually until the estate closes.

What is the purpose of a foreign executor bond?

The bond financially protects the estate's beneficiaries and creditors against losses caused by the executor's misconduct, mismanagement, or breach of fiduciary duty. It gives the court assurance that an out-of-state executor will administer the estate faithfully, with a financial remedy available if they fail to do so.

Can an out-of-state executor waive the bond requirement?

It depends on state law. Some states honor a will's bond waiver for non-residents; others, including California and Illinois, allow courts to require bonds regardless of what the will says. Written consent from all adult beneficiaries can substitute in some states, but not universally.

Who pays for the non-resident executor bond?

The executor pays the premium upfront but is generally entitled to reimbursement from estate assets as a legitimate administration expense. With court approval, the estate ultimately bears the cost.

How long does a non-resident executor bond stay in effect?

The bond remains active until the estate is fully administered, the court approves final accounts, and assets are distributed — a process that can range from several months to several years, with annual renewals required throughout.