Introduction

Most contractors hit this question at some point: "Do I need to be bonded?" In most jurisdictions, yes — and failing to get bonded before applying for a license or bidding a project can stall your entire operation.

A contractor license bond is not insurance. It doesn't protect your business from losses. It's a legally binding guarantee to the state or local licensing authority that you'll operate in compliance with applicable laws — and it's a condition of licensure in most states.

This guide covers what a contractor license bond is, how it works, what it costs, and how to get one.

Whether you're a general contractor getting licensed for the first time, a specialty trade contractor (electrical, plumbing, HVAC), or a home improvement contractor navigating renewal requirements, you'll find the requirements, cost factors, and application steps laid out clearly here.

Key Takeaways

- A contractor license bond is a three-party surety agreement guaranteeing compliance with licensing laws, required in most states to operate legally

- It protects the public and the licensing authority, not your business

- Bond cost is a premium percentage based on credit, bond size, and license type — not a flat one-time fee

- It's distinct from performance bonds, payment bonds, and contractor insurance, each of which serves a separate purpose

- Claims paid by the surety must be reimbursed by the contractor

What Is a Contractor License Bond and How Does It Work?

A contractor license bond is a three-party contract. The three parties:

- Principal — the contractor purchasing the bond

- Surety — the bonding company guaranteeing the contractor's obligations

- Obligee — the state or local licensing authority requiring the bond

As NASBP defines it, a surety bond is "a promise to be liable for the debt, default, or failure of another." In licensing contexts, the surety is promising the licensing authority that if the contractor fails to comply with applicable laws, the surety will cover the resulting damages — up to the bond's stated limit.

How a Claim Works

If a contractor abandons a job, violates building codes, or fails to pay workers or suppliers in violation of licensing law, the injured party can file a claim with the surety. If the claim is valid, the surety pays the damaged party up to the penal sum (the maximum payout specified in the bond).

One point contractors frequently overlook: the contractor must reimburse the surety for any claim paid out. A license bond does not absorb your losses — you remain fully financially responsible for whatever the surety covers.

What a License Bond Does NOT Cover

| What you might assume | What actually covers it |

|---|---|

| Project completion if you default | Performance bond |

| Subcontractor/supplier payment disputes | Payment bond |

| Your own business losses or liability claims | General liability insurance |

Mixing these up creates real gaps in coverage. Many clients and licensing authorities require both a bond and insurance — not one instead of the other.

Key Bond Terms to Know

- Penal sum — the maximum the surety will pay per claim (FAR Part 28 defines this as "the amount of money specified in a bond as the maximum payment for which the surety is obligated")

- Aggregate limit — the cap on total payouts across all claims during the bond period; Oregon's CCB bond form, for example, states aggregate liability cannot exceed the penal sum

- Cancellation provision — most bond forms allow the surety to cancel with 30 days' written notice; California's CSLB confirms cancellation takes effect 30 days from the date the notice is received

- Conditional language — most state bond forms use conditional "null and void / full force and effect" language, not a flat forfeiture clause

Bond Amounts Vary by State and Trade

Bond amounts are set by the licensing authority, not the contractor. They differ significantly by state and trade type. A few examples:

- New Jersey (Home Improvement/Home Elevation Contractors): P.L. 2023, c. 237 (signed January 2024) sets tiered requirements — $10,000 for annual volume under $150,000; $25,000 for $150,000–$750,000; $50,000 for $750,000+

- California: $25,000 contractor license bond filed with CSLB; once depleted by claims, a new bond must be purchased

- Oregon: Varies by endorsement type — residential general contractor at $25,000, commercial general contractor Level 1 at $80,000

- Washington: $30,000 for general contractors, $15,000 for specialty contractors (amounts increased July 1, 2024)

Always verify the current requirement with your specific licensing board before purchasing.

Why Contractors Need a License Bond (and What It's Not)

Most states require contractors to post a license bond before a license can be issued or renewed. The requirement exists to protect consumers — not the contractor.

State licensing boards are direct about what the bond covers:

- California CSLB: Bond funds protect consumers damaged by defective construction or licensing law violations, and employees owed unpaid wages

- Oregon CCB: Bond funds are limited — multiple parties may seek recovery from the same bond, which is why the penal sum matters

- Washington L&I: Registered, bonded contractors can bid, advertise, and perform construction work; without the bond, that access closes

Contractor License Bond vs. Contractor Insurance

These two are frequently confused, and frequently required together.

| License Bond | Contractor Insurance | |

|---|---|---|

| Protects | The public / licensing authority | The contractor's business |

| Required by | State/local licensing board | Clients, lenders, project owners |

| Triggered by | Licensing law violation | Third-party liability claim or loss |

| Who pays claims | Surety (contractor reimburses) | Insurance carrier |

Being "bonded and insured" means carrying both. Most clients and project owners require proof of each before signing a contract — they cover different risks and neither replaces the other.

Business Benefits Beyond Compliance

Understanding that distinction also clarifies the business value. A license bond does more than keep you compliant:

- Opens access to government and commercial project bids

- Differentiates your business from unlicensed or unbonded competitors

- Provides a faster dispute resolution path than litigation

- Signals financial accountability to clients who ask for proof of bonding

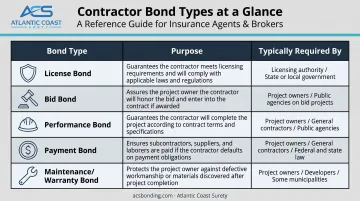

Types of Contractor Bonds

"Contractor bond" is an umbrella term. Depending on your trade, project type, and contract size, you may encounter several different bond types:

| Bond Type | Purpose | Typically Required By |

|---|---|---|

| License Bond (License & Permit Bond) | Guarantees compliance with licensing laws | State/local licensing authority |

| Bid Bond | Guarantees you'll sign the contract and provide required bonds if you win | Public/commercial project owners |

| Performance Bond | Guarantees project completion per contract terms | Project owners on larger contracts |

| Payment Bond | Guarantees subcontractors and suppliers will be paid | Federal projects (Miller Act threshold: contracts over $150,000); many state/local public contracts |

| Maintenance/Warranty Bond | Covers workmanship or material defects during a defined post-completion period | Large commercial projects (typically 1–2 years) |

This guide focuses on license bonds — the most common bond requirement for contractor licensing. If you're bidding public work, you'll likely encounter performance and payment bonds as well. NASBP's bonding guide covers each type in detail, including when they're required and how they work together on a single project.

How Much Does a Contractor License Bond Cost?

Two numbers matter here, and they're not the same:

- Bond amount (face value) — set by the licensing authority; this is what the bond pays out in claims

- Bond premium — what you actually pay; a percentage of the bond amount, determined during underwriting

A $25,000 bond does not cost $25,000. You pay a premium — typically a fraction of that face value — calculated based on your risk profile.

What Underwriters Look At

Your premium rate depends on several factors:

- Personal credit score — the most influential factor for most license bonds; a strong score means a lower rate

- Bond amount required — larger bonds carry more risk and typically higher premiums

- Type of license and state — some trades and jurisdictions carry higher underwriting risk

- Years in business and track record — established contractors with clean histories qualify for better rates

- Prior bond claims or license violations — any history of claims is a red flag in underwriting

- Financial strength of the business — larger bond amounts may require financial statements

Standard vs. Specialty Markets

Contractors with strong credit and clean records typically qualify through standard market carriers at lower rates. Contractors with poor credit, limited history, or prior claims may be placed in specialty markets — still bondable, but at higher premiums or with collateral requirements.

Access to both markets matters. Atlantic Coast Surety works exclusively in surety and maintains relationships across standard and specialty carriers — which means contractors at any credit level can be placed appropriately rather than simply declined.

Renewal and Rate Changes

Most contractor license bonds renew annually, with the premium paid each year. Rates can shift at renewal if your credit score has changed or if a claim was filed during the prior term. Some states use continuous bond structures (Washington's L&I, for example, uses a continuous contractor's surety bond) where the bond stays in force until canceled — but premiums are still typically reviewed annually.

California's CSLB makes this explicit: license renewal dates and bond renewal dates are not always the same. Track both separately to avoid a lapse.

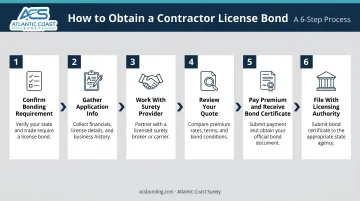

How to Get a Contractor License Bond

The process is straightforward for most contractors. Here's what it looks like step by step:

- Confirm your bonding requirement — Contact your state or local licensing board directly, or check the relevant government agency website. Verify the required bond type, bond amount, and whether the state requires a specific bond form

- Gather your application information — Typically includes business name (exactly as it appears on corporate filings), company type (LLC, S-Corp, etc.), tax ID, owner name, Social Security number, home address, and contact details. Bonds over $25,000 generally require credit authorization

- Work with a licensed surety bond provider — Submit your application through a bond-only agency or licensed surety producer. NASBP describes surety bond producers as specialists who understand market differences and help contractors establish surety relationships

- Review your quote — Your premium is quoted based on underwriting. Compare rates; a qualified provider will explain what's driving the number

- Pay the premium and receive your bond certificate — Once issued, you'll receive an executed bond document

- File the bond with the licensing authority — California requires filing with CSLB before an active license issues; Oregon requires uploading the bond and power of attorney with your CCB application; Washington requires the bond to match your exact business name and carry the surety seal

What to Look for in a Surety Provider

Choosing the right provider matters as much as completing the application. Key criteria:

- Works with A-rated and T-listed carriers — AM Best's "A" rating indicates financial strength; Treasury-listed (Circular 570) means the carrier is approved to write federal bonds

- Access to both standard and specialty markets — essential if your credit isn't perfect

- Specializes in surety bonds — agencies that offer bonds as a sideline won't have the same underwriting depth or carrier relationships as bond-only operations

Atlantic Coast Surety is a wholesale surety bond broker — surety bonds only, no general insurance lines. The agency works exclusively through retail insurance agents and brokers, not directly with contractors. With 20+ years in the market and access to A-rated and T-listed carriers across standard and specialty programs, Atlantic Coast Surety handles contractor license bond placements including NJ tiered compliance bonds and multi-state contractor programs.

Common Pitfalls

- Submitting the wrong bond form for the specific state or agency

- Filing after the license deadline, leaving you unable to operate legally

- Ignoring the cancellation provision — a lapsed bond can suspend your license without warning

- Using a surety not admitted or T-listed in your required state

Frequently Asked Questions

How much does a surety bond for a contractor license cost?

The cost depends on the required bond amount, your credit score, and your license type. You pay a premium — a percentage of the total bond amount — determined during underwriting. The stronger your credit and track record, the lower your rate. Contact a licensed surety bond provider with your bond amount, license type, and state to get an actual quote.

What is the difference between a contractor license bond and a performance bond?

A license bond guarantees your compliance with licensing laws and is required to obtain or renew your contractor's license. A performance bond guarantees completion of a specific project and is typically required by the project owner on larger commercial or public contracts. They're separate bonds serving different purposes.

Do I need a separate contractor license bond for each state I work in?

In most cases, yes. Each state or local jurisdiction with a bonding requirement will require its own bond, issued by a carrier admitted in that state. California bonds are filed with CSLB, Oregon requires a bond specific to the CCB, and Washington requires registration and bonding with L&I. Verify each state's requirements with the relevant licensing board.

What happens if a claim is filed against my contractor license bond?

The surety investigates the claim and, if valid, pays the damaged party up to the bond's penal sum. The contractor is then legally obligated to reimburse the surety for that amount. Most states require a court judgment or arbitration award before funds are released.

How long does it take to get a contractor license bond?

For most standard license bonds, approval can happen within a business day once a completed application is submitted. Applications involving larger bond amounts or adverse credit history typically take several additional business days to underwrite.

Is a contractor license bond the same as being "bonded and insured"?

No. "Bonded and insured" means having both a surety bond (typically a license bond) and business insurance — usually general liability coverage. They protect different parties and cover different risks. Many clients and licensing authorities require proof of both before work begins.