Introduction

New York doesn't issue a single statewide contractor license — and that means there's no single statewide bonding requirement either. Instead, licensing happens at the local level, and so do the bond obligations that come with it.

For contractors working in New York City, Suffolk County, Putnam County, Westchester, or Rockland County, a surety bond may be a non-negotiable part of the licensing process. Getting the wrong bond amount, naming the wrong obligee, or skipping the bond entirely can result in license denial or legal exposure.

This guide covers what a New York contractor license bond is, which jurisdictions require one, the required bond amounts, what it costs, and how to get one.

Key Takeaways

- NY contractor license bonds are required by local authorities, not the state — requirements vary by jurisdiction

- NYC DCWP: bond at the required amount (or Trust Fund enrollment at the applicable fee); Putnam County, Suffolk County: bond amounts set by local authority

- Annual premiums are a percentage of the bond amount based on underwriting factors

- Apply through a licensed surety agency — they underwrite and issue the bond on your behalf

- A lapsed bond can trigger license suspension — renew it every year without gaps

What Is a New York Contractor License Bond?

Before you can pull permits or operate legally in most New York jurisdictions, you'll need to understand what you're actually buying. A contractor license bond is a three-party surety agreement between:

- The principal — the contractor who purchases the bond

- The obligee — the local licensing authority (or, in some cases, the consumer) requiring the bond

- The surety — the bonding company that guarantees the contractor's obligations

The bond is not insurance for the contractor. It's a financial guarantee to the obligee and public that the contractor will comply with licensing laws and fulfill their obligations. If they don't, affected parties can file a claim against the bond.

How the Bond Protects Consumers

If a contractor abandons a job, causes property damage, or violates licensing rules, an aggrieved party can file a claim with the surety. The surety investigates and, if the claim is valid, pays the claimant up to the bond's full amount (its "penal sum"). The contractor then owes that money back to the surety (covered in detail in the claims section below).

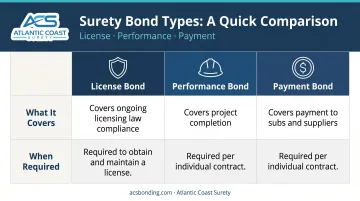

License Bond vs. Other Bond Types

Contractors encounter several bond types. Here's how they differ:

| Bond Type | What It Covers | When It's Required |

|---|---|---|

| License Bond | Ongoing compliance with licensing laws | Required to obtain/maintain a license |

| Performance Bond | Completion of a specific project | Required for individual contracts |

| Payment Bond | Payment to subs and suppliers on a job | Required for individual contracts |

A license bond follows your license, not any single project — so one bond covers your entire scope of work for the year.

NYC's Trust Fund Option

NYC DCWP gives home improvement contractors two ways to satisfy this requirement: enroll in the NYC HIC Trust Fund at the current enrollment fee or submit a surety bond at the required amount. The bond is one of two valid paths — not the only one.

Who Needs a Contractor License Bond in New York?

Bond requirements depend entirely on where you work. Here's a jurisdiction-by-jurisdiction breakdown.

New York City (DCWP Home Improvement Contractor License)

NYC DCWP requires a Home Improvement Contractor (HIC) license for any construction, repair, remodeling, or home improvement work on NYC residential property above the applicable minimum cost threshold. As part of the licensing application, contractors must either:

- Enroll in the DCWP Trust Fund at the current enrollment fee, or

- Submit a copy of a surety bond at the required amount

The bond must name the Department of Consumer and Worker Protection as the Certificate Holder (not "City of New York"). Use the exact DCWP checklist language when instructing your surety.

This applies to general home improvement contractors, remodelers, roofers, siding contractors, and similar trades. Note that certain work types — including electrical, plumbing, painting, new construction, and work in buildings with more than four units — are exempt from the HIC license under NYC311 guidance.

Other New York Counties With Bond Requirements

Suffolk County Suffolk County Consumer Affairs may require a surety bond as evidence of financial responsibility. Key requirements include:

- Bond amount set by the Director (confirm your specific amount directly with Suffolk Consumer Affairs)

- Public liability/property damage insurance at the minimum required by the county

Because the amount is discretionary, contact Suffolk Consumer Affairs before applying to confirm what's required.

Putnam County Putnam County requires home improvement contractor registrants to furnish a License & Permit Bond at the required amount. The bond must:

- Run for the full two-year registration term

- Name Putnam County Dept. of Consumer Affairs as the obligee

- Be signed by the principal if it's a new bond

Westchester County Westchester's Director or Sealer may require a bond or cash security up to the maximum set by the County Attorney. Key details:

- Bond runs to the County of Westchester

- Requirement is discretionary (not every applicant will be asked for one)

Confirm your status directly with the Westchester Department of Consumer Protection before proceeding.

Rockland County Rockland County Chapter 286 sets a surety bond requirement within a defined range for contractors using the applicable application pathway. Key details:

- Bond runs to the County of Rockland

- Exact amount varies — call Rockland's Consumer Protection office to verify before ordering

Nassau County Nassau's official licensing pages did not specify a surety bond requirement for home improvement contractors in the materials reviewed. Don't assume no bond is needed — call Nassau County Consumer Affairs directly to confirm current requirements before applying.

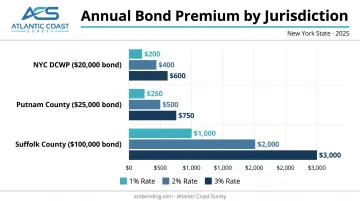

How Much Does a New York Contractor License Bond Cost?

You don't pay the full bond amount. You pay an annual premium — a percentage of the bond's penal sum.

Premium Rate Benchmarks

According to NFP's license and permit bond data, applicants with strong credit typically pay a lower percentage of the bond amount annually. Those with lower scores or financial risk factors can see rates climb significantly higher.

Example Premium Calculations

Premiums are calculated as a percentage of the required bond amount. The exact rate depends on your credit profile and the surety's underwriting criteria. Contact a licensed surety provider for current rate information based on your jurisdiction's required bond amount.

What Affects Your Rate

Sureties evaluate several factors when setting your premium:

- Personal credit score — the single biggest driver

- Years in business — longer track records signal lower risk

- Claims history — prior bond claims increase your rate

- Business financials — revenue, cash flow, and outstanding liabilities

- Bond amount required — larger bonds receive more scrutiny

Improving any of these factors before applying — especially your credit score — can move your rate toward the lower end of the range.

Renewal and Continuity

You pay bond premiums annually. The bond must remain active for as long as you hold your license — if it lapses, your license can be suspended or revoked. Factor renewal costs into your yearly expenses, and confirm renewal terms when you first purchase the bond.

How to Get a New York Contractor License Bond

Step-by-Step Process

Confirm the requirement — Contact the licensing authority in your jurisdiction (NYC DCWP, Suffolk Consumer Affairs, Putnam County, etc.) and get the exact bond amount and obligee name before ordering anything.

Gather your application information — You'll typically need:

- Business name, entity type (LLC, S-Corp, C-Corp), and address

- Owner's name, Social Security number, and home address

- Tax ID and contact information

- For larger bonds: financial statements, bonding history, work-in-progress details, and CPA information

Apply through a licensed surety agency — Work with a surety-focused agency that has access to multiple A-rated, Treasury-listed carriers. The surety underwrites the risk, issues a quote, and — if approved — produces the bond document.

Submit the bond to the licensing authority — Some jurisdictions accept copies; others (like Putnam) require the original. Confirm the delivery requirements before you apply.

What to Expect for Turnaround

Once you've submitted your application, turnaround depends mostly on bond size and underwriting complexity. Most standard contractor license bonds below the standard threshold can be issued same-day or within 24–48 hours. Larger bonds — or those requiring full financial underwriting — typically take several business days as the surety reviews financials and work history.

Choosing a Surety Agency

Look for a bond-only agency with access to both standard and specialty markets. This matters most if your credit history is mixed or your business profile is complex — specialty market access means more options and fewer declined applications.

Atlantic Coast Surety is a wholesale surety broker in Mahwah, NJ, with 20+ years placing contractor bonds through A-rated, Treasury-listed carriers. New York contractors access Atlantic Coast Surety through their retail insurance agent or broker, who handles the application submission. That structure connects contractors to Atlantic Coast Surety's carrier relationships and in-house underwriting authority, which speeds up approvals and keeps pricing competitive.

What Happens If a Claim Is Filed Against Your Bond?

The Claims Process

If a consumer or licensing authority believes you've violated the terms of the bond — failed to complete work, caused property damage, or breached licensing regulations — they can file a claim with the surety. The surety investigates and, if the claim is valid, pays the claimant up to the bond's penal sum (the maximum covered amount).

The Critical Distinction: You Are Not Protected

This is where contractors sometimes get confused. The bond protects the consumer and the licensing authority — not you. When the surety pays a claim, you owe that money back. You formalize this reimbursement obligation by signing an indemnity agreement when you purchase the bond.

As NASBP's guidance on indemnity agreements states, contractors and indemnitors are legally bound to protect the surety from losses — meaning a paid claim becomes your personal financial liability, not a cost the surety absorbs.

Consequences of a Paid Claim

- The claim does not eliminate your obligation to pay the claimant or reimburse the surety

- Sureties evaluate claims history during underwriting, so a paid claim can affect future bond applications and pricing

- Maintaining a clean bond record keeps your premiums low and your license intact

Operate ethically, complete your work, and communicate with clients when problems arise. If a dispute does escalate to a claim, your exposure goes beyond that single payout — it follows you into every future bond application and renewal.

Frequently Asked Questions

How much does a New York contractor license bond cost?

Costs depend on the bond amount your jurisdiction requires and your credit profile. Most contractors with good credit pay a lower annual rate as a percentage of the required bond amount. See the cost section above for guidance on how rates are determined.

What types of bonds can be required from a New York contractor?

The three main types are: a license bond (required by the local licensing authority and tied to your license), a performance bond (guarantees project completion), and a payment bond (ensures subs and suppliers get paid). Of these, license bonds are the ongoing requirement most NY contractors must maintain.

How long does it take to get a New York contractor license bond?

Many standard bonds below the typical threshold are issued the same day or within 24–48 hours. Larger bonds may take longer because they typically require a credit check and additional financial review.

Is a contractor license bond the same as contractor insurance?

No. Insurance covers the contractor against losses such as property damage claims or injuries. A bond is a financial guarantee that protects consumers and the licensing authority. Most jurisdictions require both — they serve different purposes and neither replaces the other.

What happens if a claim is filed against my New York contractor license bond?

The surety investigates and, if valid, pays the claimant — but you must reimburse that amount under your indemnity agreement. A paid claim can make future bonding harder to obtain and typically drives up your premiums.

Do I need a bond to work as a contractor in every New York county?

No — requirements vary by jurisdiction. NYC (DCWP), Putnam County, Suffolk County, Westchester, and Rockland all have bond requirements, though some are discretionary. Nassau County's requirements were not confirmed from official sources reviewed. Check directly with your local licensing authority to confirm what's required before submitting your license application.