All existing contractor registrations expired March 31, 2025. Renewals require proof of a compliant bond — no exceptions.

Many contractors understand they need the bond but aren't sure what it actually is, how much it costs, or how the claim process works. This guide covers all of it, using the official statutory requirements from P.L. 2023, c.237 and the NJ Division of Consumer Affairs registration guidance.

Key Takeaways

- A contractor license bond guarantees you'll perform as contracted — it protects consumers, not you

- The 2025 CBRA amendments made bonds mandatory; renewals after March 31, 2025 must include proof of a compliant bond

- Required bond amounts are tiered — determined by your active contract values and prior 12-month volume

- Bond premiums are credit-driven; you pay a percentage of the bond amount, not the full amount

- Exemptions apply to contractors working solely on their own property and licensed professionals operating within their specialty

What Is a New Jersey Contractor License Bond and Why Is It Required?

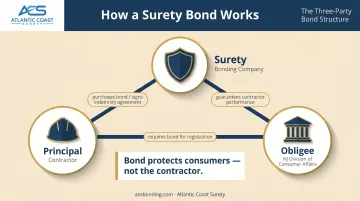

The Three-Party Structure

A New Jersey contractor license bond — referred to in CBRA language as a "compliance bond" — is a legally binding agreement between three parties:

- Principal — the contractor who purchases the bond

- Surety — the bonding company that guarantees the contractor's performance

- Obligee — the NJ Division of Consumer Affairs, acting on behalf of consumers

As NASBP explains, a surety bond is not an insurance policy. It's a financial guarantee. The surety backs the contractor's obligations, and if those obligations aren't met, consumers have recourse through a bond claim.

This is the core distinction that trips up most contractors: general liability insurance protects you; the surety bond protects your clients.

Why the State Requires It

That three-party structure exists for a reason. The NJ Division of Consumer Affairs receives thousands of complaints each year from consumers who hire home contractors — missed deadlines, shoddy workmanship, and deposits taken without work being completed are among the most common grievances. The 2025 CBRA amendments were designed to raise the financial accountability floor for every registered contractor.

The amended law, effective immediately upon signing, created the New Jersey State Board of Home Improvement and Home Elevation Contractors and mandated surety bonds as part of contractor registration. All existing registrations expired March 31, 2025. Renewals now require a compliant bond alongside other documentation.

NJ Contractor Bond Amount Requirements

NJ contractor bond amounts follow a three-tier structure set by statute. Your required amount is determined by two separate metrics: the value of your largest active contract and your total contract volume over the prior 12 months.

Current Active Contract Value

| Largest Active Contract Value | Required Bond Amount |

|---|---|

| Below the lower threshold | First tier amount |

| Between the lower and upper thresholds | Middle tier amount |

| Above the upper threshold | Maximum tier amount |

Prior 12-Month Contract Volume

| Total Volume — Prior 12 Months | Required Bond Amount |

|---|---|

| Below the lower volume threshold | First tier amount |

| Between the lower and upper volume thresholds | Middle tier amount |

| Above the upper volume threshold | Maximum tier amount |

The statute connects these two criteria with "or," meaning whichever tier applies to your situation sets your required amount. Review both tables and confirm which tier your business falls under before applying. See the NJ DCA FAQ for additional guidance.

Accompanying Insurance Requirements

The bond doesn't replace your liability coverage — both are required under CBRA, and they serve different purposes:

- HICBs: The minimum commercial general liability per occurrence required by statute

- HECBs: A higher minimum commercial general liability per occurrence required by statute

Workers' compensation coverage is also required unless you qualify for an exemption.

How the NJ Contractor Bond Works

What Triggers a Claim

Not every dispute leads to a valid bond claim. The compliance bond responds to specific contractor failures:

- Deliberately abandoning a project after receiving payment

- Misappropriating client deposits

- Materially breaching contract terms without performing the work

Routine disagreements over quality or minor scope disputes aren't typically grounds for a bond claim — those situations fall under general liability or contractual resolution. The bond exists for clear-cut non-performance.

The Reimbursement Obligation

The bond is not insurance — it doesn't absorb losses on the contractor's behalf. If a consumer files a valid claim and the surety pays out, the contractor must reimburse the surety in full: principal, expenses, and any associated costs. The General Agreement of Indemnity, signed at purchase, makes this legally enforceable.

In practice, it works more like a line of credit the surety extends on your behalf. Draw on it, and you pay it back.

Additional Mechanics Under NJ Law

The statute includes several provisions worth knowing:

- Replenishment: If a claim is paid, you must replenish the bond to its full required amount

- Aggregate cap: The surety's total liability doesn't exceed the bond amount

- Cancellation notice: A bond can't be cancelled or non-renewed without at least 10 days' written notice to the contractor

- Scope limitation: The bond covers CBRA violations and consumer losses — it does not cover treble damages under the Consumer Fraud Act

- Renewal rates: A clean claims history keeps your bond renewal costs lower and makes future bonding easier to secure

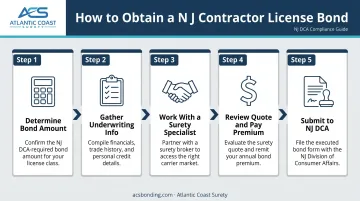

How to Get Your NJ Contractor License Bond

Step 1 — Determine Your Required Bond Amount

Review both tier tables above. Identify your largest active contract value and calculate your total contract volume over the prior 12 months. Confirm which bond tier applies based on those figures.

Step 2 — Gather Your Underwriting Information

Sureties evaluate several factors before issuing a bond. Have the following ready:

- Company name as it appears on the corporate seal

- Business entity type (LLC, S-Corp, C-Corp, LLP)

- Tax ID, street address, phone, and email

- Owner's name, Social Security number, and home address

- Summary of contracting history and years in business

- Any prior bond claims or credit issues to disclose

For bonds above the applicable threshold, expect a credit check — the surety will pull both corporate and personal credit reports as part of underwriting.

Step 3 — Work With a Surety Specialist

Shopping a single carrier limits your options and may not get you the best rate for your situation. Working with a specialist who accesses multiple markets means your application is priced competitively from the start.

Atlantic Coast Surety, based in Mahwah, NJ, places contractor compliance bonds for qualifying amounts through A-rated, T-listed providers. With 20+ years in the NJ market and in-house underwriting authority, the team can evaluate your application without routing it through multiple external approvals — a real advantage when you're working against a registration deadline.

Step 4 — Review Your Quote and Pay the Premium

Your quote will be expressed as a percentage of the bond amount. That percentage — your annual premium — depends on your credit profile, bonding history, and years in business. You pay the premium annually to keep the bond active throughout your registration period.

Step 5 — Submit Your Documentation to NJ DCA

Along with your bond certificate, your HICB or HECB registration or renewal application requires:

- Certificate of commercial general liability insurance

- Workers' compensation proof (or exemption documentation)

- Background check results

- Applicable registration fee

Submit everything together to the New Jersey Division of Consumer Affairs to complete your registration.

Common Misconceptions About NJ Contractor Bonds

"The bond is the same as my contractor insurance."

Not even close. General liability insurance protects you from third-party injury and property damage claims. The surety bond protects your clients if you fail to perform. Both are required under CBRA — they're complementary, not interchangeable.

"Only large contractors need to be bonded."

The requirement applies at every tier. Even a contractor whose largest contract falls below the lower threshold must carry the minimum required bond. Volume scales the amount up, but the obligation exists from day one of registration.

"Getting bonded takes weeks."

For contractors with solid credit and a clean history, the process can move quickly. Atlantic Coast Surety's in-house underwriting authority lets decisions move without waiting on external carrier review cycles.

Contractors with credit challenges or prior claims may take longer, as the surety assesses the risk profile more carefully. Starting the process early gives you room to work through any underwriting questions before your registration deadline.

Frequently Asked Questions

How much is a compliance bond in NJ?

Bond amounts are tiered depending on your active contract values and prior 12-month volume. The premium you pay is a percentage of that amount, with the exact rate driven by your credit profile and experience. Atlantic Coast Surety offers competitive rates through A-rated and T-listed providers.

What are the bond requirements for contractors in New Jersey?

Under the 2025 CBRA amendments, HICBs and HECBs must secure a surety bond at the applicable tier, along with the required commercial general liability insurance and workers' compensation coverage, as a condition of registration with the NJ Division of Consumer Affairs.

How long does it take to get a contractor bond?

Contractors with strong credit and clean histories can often get bonded within a few business days. Those with credit challenges or prior claims should expect additional time as the surety conducts a more thorough underwriting review.

What is the difference between a contractor bond and contractor insurance in NJ?

The bond protects consumers — it guarantees you'll perform as contracted and provides recourse if you don't. General liability insurance protects you from claims of property damage or bodily injury caused during your work. Both are required under CBRA, but they serve entirely different functions.

What happens if a claim is made against my NJ contractor bond?

The surety investigates the claim and may pay the consumer up to the bond limit. You are then personally obligated to reimburse the surety in full — the bond is not insurance; you bear the financial liability. Claims also affect your renewal rates and future bonding eligibility.

Do all NJ contractors need a surety bond, or are there exemptions?

Most HICBs and HECBs are required to carry the bond, but exemptions exist for contractors working solely on their own or a family member's property, those performing work without compensation, and licensed professionals (plumbers, electricians) working within their licensed specialty. Review the full exemption list on the NJ Division of Consumer Affairs website before assuming an exemption applies to your situation.