The renewal process itself is straightforward for most bond types — but the steps, documents, and costs vary depending on what kind of bond you hold. This guide breaks down exactly what renewal involves, which bonds require it, how much it costs, and what happens if you miss your deadline.

Key Takeaways

- Surety bond renewal extends your existing coverage for a new term — but not every bond type requires it.

- Renewal notices typically arrive 60 days before expiration — track your own deadline rather than waiting for one.

- Most renewals require only payment — no full underwriting review unless your bond details have changed.

- Renewal premiums can shift year to year based on your credit score, claims history, and changes to the required bond amount.

- An expired bond can trigger license suspension, fines, and out-of-pocket liability for uncovered claims.

What Is a Surety Bond Renewal?

A surety bond renewal is an extension of the bond's active term, issued by the surety company so the principal maintains continuous coverage beyond the original expiration date. Rather than starting from scratch with a new bond, the principal pays a fresh premium and receives confirmation — or a new document — that coverage continues. That three-party structure, as NASBP outlines, holds at renewal just as it does at original issuance.

Three parties are involved in every surety bond relationship:

- Principal — the contractor, business owner, or individual required to hold the bond

- Obligee — the government agency or entity requiring the bond

- Surety — the bonding company guaranteeing the principal's obligations

At renewal, the transaction flows from the principal to the surety (payment), and from the surety to the obligee (updated documentation confirming coverage).

Renewal is not the same as getting a new bond. The surety typically doesn't require a new indemnity agreement or fresh application — they review the account, issue a renewal document, and coverage carries forward without interruption.

Which Surety Bonds Need to Be Renewed?

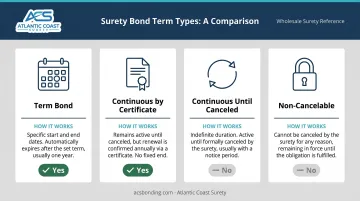

Renewal obligations depend entirely on the bond's term structure. There are four types to know:

| Bond Term Type | How It Works | Renewal Required? |

|---|---|---|

| Term Bond | Fixed start and end dates | Yes — new bond or filing required each term |

| Continuous by Certificate | Remains active when a continuation certificate is issued annually | Yes — certificate must be filed with the obligee |

| Continuous Until Canceled | Stays active as long as premiums are paid | Premium payment required; no new filing typically needed |

| Non-Cancelable | No expiration; only released by the obligee | Premium still owed; no renewal filing required |

Bond Types That Typically Require Annual Action

Bonds that typically require annual renewal action include:

- Contractor license bonds — California, for example, requires continuous bond coverage to avoid license suspension, with the current bond amount set by CSLB requirements

- Motor vehicle dealer bonds — Washington requires a dealer bond at the required state amount; cancellation or exhaustion automatically cancels the dealer license

- **Commercial license and permit bonds** — license and permit bonds guarantee compliance with statutes and ordinances, and most require annual renewal

Court and probate bonds follow a different model. Atlantic Coast Surety places probate bonds — covering administrators, executors, guardians, and trustees — on a non-cancelable basis. These bonds remain active until formally discharged by the court. Principals still owe annual renewal premiums, but no renewal filing is required. The bond stays active until the obligee (the court) officially releases it.

Performance and payment bonds are generally project-specific instruments tied to a contract's completion date. They don't follow a standard renewal schedule.

Step-by-Step: How to Renew Your Surety Bond

The renewal process is straightforward in most cases, though the specific steps depend on your bond term type and whether any details have changed since the original issuance.

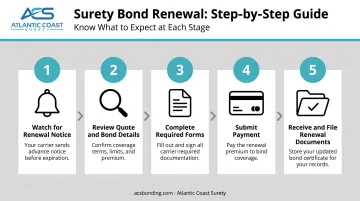

Step 1: Watch for Your Renewal Notice

Sureties typically send renewal notices before the expiration date. Old Republic Surety, for example, generates renewal bills approximately 60 days before the renewal date. The notice usually includes a premium quote and payment instructions.

That said, the responsibility to renew on time stays with the principal — even if no notice arrives. Track your expiration date independently. California's CSLB advises contractors to arrange bond renewal at least four weeks before the old bond expires, since license renewal and bond renewal dates rarely align.

Step 2: Review Your Renewal Quote and Bond Details

The renewal notice includes a premium quote for the next term. Before paying, verify:

- The bond amount matches current obligee requirements

- Your business name and license number are accurate

- The obligee's requirements haven't changed

If anything has changed — bond amount, business structure, or obligee requirements — flag it before paying. Changes can trigger an underwriting review.

Step 3: Complete Any Required Forms

Most straightforward renewals require no additional documents beyond payment. However, if bond details have changed, the surety may request updated materials.

For modified bonds, expect to provide:

- Updated financial statements

- Revised bond amount confirmation

- An addendum or rider request form documenting the specific change

If the surety requires a credit review, the process mirrors the original application. Submit all requested materials promptly — delays here are the most common cause of coverage gaps.

Step 4: Submit Payment

Once forms are complete, pay the renewal premium to the surety. Agents working through a bond-only agency like Atlantic Coast Surety gain access to competitive renewal rates across multiple A-rated and T-listed carriers. With in-house underwriting authority and 20+ years in the surety market, straightforward renewals with no material changes typically move through faster.

Step 5: Receive and File Renewal Documents

What you receive after payment depends on your bond type:

- Term bond: a new bond form requiring filing with the obligee

- Continuous by certificate: a continuation certificate requiring filing with the obligee

- Continuous until canceled: confirmation that coverage continues; no filing typically needed

For term bonds and continuation certificates, filing with the obligee is not optional — missed filings can create compliance gaps even when the bond itself is paid and active.

State requirements vary. California's CSLB requires bond documentation at CSLB headquarters within 90 days of the effective date, with business name and license number matching CSLB records. South Carolina dealer renewals require uploading a Bond Continuation Certificate or proof of a new bond before the license renews.

How Much Does It Cost to Renew a Surety Bond?

Renewal premiums are often close to what you paid originally — but several factors can push the rate up or down.

Key Cost Factors

- Credit score — Stronger credit signals lower risk and reduces premiums; declining scores raise them. Underwriters look at payment history, tax liens, judgments, and bankruptcies.

- Claims history — A prior claim can raise your renewal premium or trigger a declination. In California, a claim that reduces the bond amount can also suspend the bond.

- Bond amount changes — If the obligee has raised the required bond amount, the premium adjusts accordingly. Washington and Oregon, for example, both updated required bond amounts in 2024.

- Market conditions — Surety risk assessments shift with industry trends and carrier appetite, regardless of your own record.

Practical Ways to Secure a Better Rate

- Pay bills on time and address negative credit items before renewal

- Avoid claims where possible — disputes resolved outside the bond preserve your renewal rate

- Ask about multi-year terms — some bond types qualify, cutting annual renewal paperwork

- Work with an agency that accesses multiple surety markets — rate comparison across carriers often yields meaningful savings at renewal

What Happens If You Don't Renew Your Surety Bond on Time?

Missing a renewal deadline sets off a chain of consequencescan trigger consequences that escalate faster than most principals expect.

Immediate Consequence: Notice of Cancellation

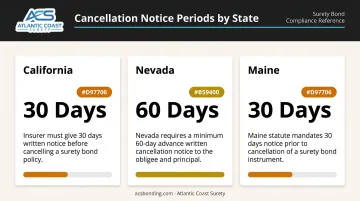

When a bond lapses, the surety typically issues a cancellation notice. Notice periods vary by state and bond type:

- California: license bond is canceled 30 days after CSLB receives a cancellation notice

- Nevada: surety can cancel a contractor bond with 60 days notice to the Nevada State Contractors Board

- Maine: cancellation requires 30 days written notice; liability incurred before that period expires is not affected

An expired bond is not the same as a formally canceled bond. Cancellation still requires written notice to the obligee.

Downstream Consequences

Operating without an active bond puts the principal at serious risk:

Simply not paying the premium does not end all obligations — particularly for court and probate bonds. These bonds remain in force until the court formally discharges them.

The principal, agent, and surety cannot cancel a probate bond after filing. Premium continues to be owed until the obligee releases the bond, regardless of whether the principal stops paying.

Frequently Asked Questions

What does it mean to renew a bond?

Renewing a bond means extending coverage for a new term by paying a fresh premium to the surety. The principal stays compliant with the obligee's bonding requirement without obtaining an entirely new bond.

Are surety bonds renewed annually?

Most renewable bonds follow a 12-month cycle, though multi-year terms exist for certain bond types. Court bonds and one-time project bonds — such as performance and payment bonds — don't follow any renewal schedule.

How do I renew a surety bond?

The process typically follows these steps:

- Watch for your renewal notice around 60 days before expiration

- Review the quote and submit any required forms

- Pay the premium

- File renewal documents with the obligee if your bond type requires it

How much does a surety bond cost?

Bond premiums are typically a percentage of the bond amount. Performance bonds generally run a percentage of the contract price based on underwriting factors. Exact rates depend on bond type, credit profile, and the surety's underwriting criteria.

Can my surety bond renewal cost change from year to year?

Yes. Renewal costs can shift based on credit score changes, claims filed against the bond, increases to the required bond amount, or changes in the surety's risk assessment for your industry.

What happens if I miss my surety bond renewal deadline?

A missed renewal typically triggers a cancellation notice from the surety. Depending on your license type and state, consequences can include:

- Automatic license cancellation

- Fines from the licensing authority

- Personal liability for claims filed during the lapsed period