A continuous surety bond is a financial guarantee that stays active indefinitely — renewing each year until formally terminated — rather than covering a single transaction. Contractors, commercial businesses, ERISA plan sponsors, and regular importers typically need one to maintain uninterrupted compliance with licensing, regulatory, or customs requirements.

This guide explains what a continuous surety bond is, who needs one, how the process works end-to-end, what it costs, and the misconceptions that get principals into trouble.

Key Takeaways

- A continuous surety bond renews automatically each year until cancelled — no re-application needed for each covered period

- Required across many contexts: U.S. customs imports, contractor licensing, commercial compliance, and ERISA fiduciary obligations

- Three parties are involved: the principal, the surety (bond provider), and the obligee (the agency requiring the bond)

- The application involves a short submission and underwriting review; standard bonds are often approved within one to two business days

- You pay an annual premium, not the full bond amount, though you remain financially liable for any claims the surety pays out on your behalf

What Is a Continuous Surety Bond?

A continuous surety bond is a legally binding three-party agreement in which a surety company guarantees to an obligee — a government agency, regulator, or counterparty — that the principal will fulfill a specific ongoing obligation. As long as annual premiums are paid, the bond remains in force indefinitely without needing to be re-issued.

The three parties every continuous bond involves:

- Principal: the business or individual required to obtain the bond

- Surety: the bonding company that underwrites and issues the guarantee

- Obligee: the agency or entity requiring the bond as a condition of licensing, compliance, or activity

How It Differs from a Single-Entry Bond

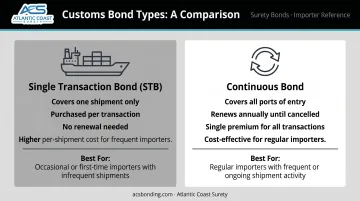

The key difference is scope. CBP Help confirms that a single transaction bond (STB) secures one import shipment, while a continuous bond covers all import transactions at all U.S. ports of entry and renews annually until terminated. The same logic applies outside customs: a term bond covers a fixed period or specific obligation, while a continuous bond provides ongoing coverage with no expiration gap.

Where Continuous Bonds Fit

The Surety & Fidelity Association of America (SFAA) categorizes surety bonds into two broad groups — contract bonds and commercial bonds. Continuous structures appear most often in:

- License and permit bonds: required by government agencies for ongoing business compliance

- Commercial bonds: covers customs/import bonds, ERISA fidelity bonds, and similar regulatory obligations

- Court and fiduciary bonds: apply in legal or probate proceedings where fiduciary duties are recurring

Why Businesses and Importers Need a Continuous Surety Bond

A continuous bond isn't optional in most regulated contexts — it's a prerequisite for operating legally. Here's where the requirement most commonly applies:

U.S. Customs Importers

19 CFR Part 113 governs CBP bond requirements. For regular commercial importers, a continuous bond covers all import transactions at all U.S. ports of entry for a rolling annual period. The alternative — purchasing a single transaction bond for each individual shipment — becomes costly and impractical for businesses that import regularly.

Without an active continuous bond, importers face shipment holds and potential delays across all entry points, not just one port.

Contractors and Licensed Businesses

State licensing authorities require an active bond as a condition of issuing or renewing a contractor's license. Several states are explicit about this:

- California (CSLB): A contractor bond must be in place before the board can issue, reactivate, or renew a license

- Oregon (CCB): Similar requirements apply, with bond amounts updated as recently as January 1, 2024

- Most other states: Follow comparable rules — no active bond means no active license

A lapsed bond can result in license suspension, which means the contractor cannot legally work until coverage is reinstated.

ERISA Plan Sponsors and Fiduciaries

Under ERISA Section 412, plan officials who handle employee benefit plan funds must be covered by a fidelity bond. Per DOL Field Assistance Bulletin No. 2008-04, the bond amount must equal at least the statutory minimum percentage of plan funds handled, subject to the applicable minimum and maximum amounts for most plans (higher limits apply for plans holding employer securities).

The IRS recommends an annual review of bonding requirements as plan assets fluctuate. ERISA fidelity bonds are typically structured as continuous, billed on a three-year term, and often include an inflation guard endorsement that automatically adjusts coverage as plan assets grow — Atlantic Coast Surety places these bonds as part of its standard offerings.

How a Continuous Surety Bond Works

The Three-Party Mechanic

The principal applies for the bond. The surety underwrites and issues it. The obligee (CBP, a state licensing board, a municipality) is the protected party.

If the principal fails to meet their obligations, the obligee files a claim against the surety. The surety pays, then seeks reimbursement from the principal under the indemnity agreement signed at application. That reimbursement obligation is binding — the principal cannot opt out after a claim is paid.

The key distinction between a surety bond and traditional insurance: the principal is always ultimately liable for repaying claims.

Annual Renewal and Termination

A continuous bond does not expire on a fixed date. The surety bills the principal annually, and coverage continues uninterrupted as long as premiums are paid.

Either party can initiate termination. For CBP customs bonds specifically:

- The principal can terminate by written request with at least 10 business days' notice

- The surety must provide at least 30 days' notice to terminate a bond

Critical: Termination does not eliminate liability for obligations incurred before the effective termination date. A claim can still be filed against a terminated bond for transactions that occurred while it was active.

Bond Amount vs. Premium

These are not the same, and confusing them is a common and costly mistake.

| Term | Definition |

|---|---|

| Bond Amount | The maximum the surety will pay if a valid claim is made (set by the obligee) |

| Annual Premium | The fee the principal pays to keep the bond active each year |

The bond amount represents the surety's maximum exposure per claim, not what you pay. Your annual premium is typically a small percentage of that amount.

CBP conducts monthly sufficiency reviews of active continuous import bonds. If your import volume increases and the bond becomes insufficient, you have 15 days to remedy the deficiency or face additional security requirements.

How to Obtain a Continuous Surety Bond: Step-by-Step

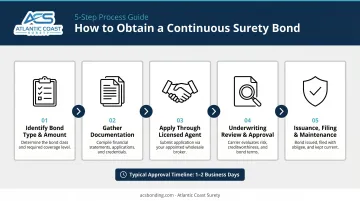

For most standard bond amounts, the process completes in one to two business days. Accuracy at each step directly affects both approval speed and premium cost.

Step 1: Identify the Required Bond Type and Amount

Before anything else, confirm exactly which bond is required and what the minimum amount must be.

- Importers: Per CBP Directive 3510-004, the minimum continuous Activity Code 1 import bond is subject to a mandatory minimum set by CBP. The standard formula is a percentage of duties, taxes, and fees paid in the prior calendar year, rounded in prescribed increments.

- Contractors: The required amount is set by the state licensing authority. Requirements vary by state and license classification.

- ERISA sponsors: A statutory percentage of plan funds handled, subject to the DOL minimums and maximums described above.

Under-bonding creates an "insufficient" bond status — which can trigger regulatory action just as effectively as having no bond at all.

Step 2: Gather Required Documentation

Having the right documents ready upfront prevents underwriting delays. Standard documentation for most continuous bond submissions includes:

- Completed bond application and supplementary questionnaire

- Business identification (EIN, business license, importer number)

- CPA-prepared financial statements for the prior three fiscal years

- Current personal financial statements for owners or authorized officers

- Three months of corporate and personal bank statements

- Executed indemnity agreement

For ERISA bonds, the documentation is more streamlined: plan sponsor details, the number of trustees or administrators with direct fund access, whether the plan covers union or multi-employer funds, and whether the plan contains ESOP-employer securities.

Step 3: Apply Through a Licensed Surety Agent

Continuous surety bonds for federal purposes must be issued by surety companies listed on Treasury Department Circular 570 — which certifies companies holding Certificates of Authority as acceptable sureties on federal bonds.

Working with a bond-only agency like Atlantic Coast Surety gives access to multiple A-rated and T-listed surety markets. A specialized broker with 20+ years across contract, commercial, ERISA, court, and specialty programs can match the right carrier to the specific bond type and risk profile. That matters when a single-carrier shop has no flexibility on harder-to-place risks.

Step 4: Underwriting Review and Approval

The surety evaluates the principal's credit profile, financial history, business type, bond amount, and risk factors. Approval timelines vary:

- Standard bond amounts: Often approved within one to two business days after application

- Larger or higher-risk bonds: May require two to five business days and additional documentation or collateral

Once a bond line is established, subsequent requests for the same principal typically move faster — the financial review is already on file.

Step 5: Bond Issuance, Filing, and Ongoing Maintenance

Once approved, the surety issues the bond and it is filed with the relevant obligee. The principal receives a copy or confirmation.

Keeping the bond in good standing is straightforward, but neglecting any of the following can trigger deficiency notices:

- Paying the annual renewal premium on time

- Notifying the surety of material changes (business name, address, ownership, significant changes in import volume)

- Monitoring bond sufficiency — especially for importers whose duty obligations grow year over year

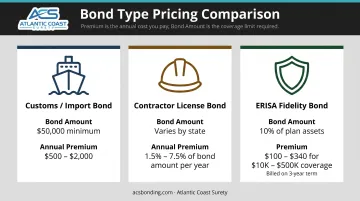

How Much Does a Continuous Surety Bond Cost?

Premium Benchmarks by Bond Type

Annual premiums are a percentage of the bond amount — not the bond amount itself. What principals actually pay depends on bond type and their risk profile.

| Bond Type | Typical Bond Amount | Annual Premium Range |

|---|---|---|

| Customs/Import (continuous) | CBP-required minimum | Competitive rates based on underwriting factors |

| Contractor License Bond | Varies by state | A percentage of the bond amount per year |

| ERISA Fidelity Bond | Statutory percentage of plan assets | Competitive rates based on coverage amount |

For ERISA bonds placed through Atlantic Coast Surety, premiums are structured on a three-year continuous term. Atlantic Coast Surety offers competitive rates through NGM Insurance Company (Spring Valley Mutual in Minnesota). Contact a specialist for current pricing.

Rates are not available in Alaska, California, or Hawaii.

What Drives Premium Variation

Four factors determine your final premium:

- Credit profile — personal and business credit scores are the primary underwriting factor for most standard bonds

- Bond amount — larger bond amounts carry higher premiums in absolute terms

- Industry and risk type — anti-dumping entries, high-volume imports, or specialty commercial bonds increase the risk profile

- Collateral requirements — higher-risk applicants may need to post collateral, which increases the total cost of bonding

Common Misconceptions About Continuous Surety Bonds

"It works like insurance"

This is one of the most common misunderstandings. The SFAA distinguishes surety from traditional insurance explicitly: surety underwriting is designed to prevent loss by prequalifying the principal — not to absorb losses on the principal's behalf. When the surety pays a claim, the principal owes that money back under the indemnity agreement. The premium buys the guarantee; it doesn't cap your exposure.

"Cancelling the bond ends all liability"

CBP confirms this directly: terminating a continuous bond does not release the principal or surety from liability for obligations incurred before the termination date. Any claim tied to activity during the bond's active period can still be pursued — regardless of when the bond was cancelled.

"A continuous bond is always the right structure"

Not necessarily. A single-entry or term bond may be more cost-effective for:

- Importers who ship infrequently at low values

- Businesses facing a one-time or temporary licensing requirement

- Principals with a single contractual obligation rather than a recurring one

The ongoing annual premium commitment only makes sense when the underlying obligation is genuinely continuous. If you're unsure which structure fits your situation, that's the right question to bring to a surety specialist before committing.

Frequently Asked Questions

Frequently Asked Questions

What is a continuous surety bond?

A continuous surety bond is an ongoing financial guarantee between a principal, a surety company, and an obligee. It renews automatically each year until cancelled, providing uninterrupted coverage for licensing, regulatory, or compliance obligations — no new application required each period.

How much does a continuous surety bond cost?

Cost depends on the bond amount and the principal's risk profile. The premium is a percentage of the required bond amount, determined through underwriting. Atlantic Coast Surety offers competitive rates across all continuous bond types through A-rated and T-listed providers.

What are the three types of surety bonds?

The three main categories are contract bonds (guarantee performance and payment on construction or service contracts), license and permit bonds (required by government agencies for business licensing compliance), and court/fiduciary bonds (required in legal or probate proceedings to protect beneficiaries or the court).

How long does it take to get a continuous surety bond?

Standard bond amounts are often approved within one to two business days after a complete application is submitted. Larger or specialty bond amounts requiring full underwriting review may take two to five business days. Electronic filing with the obligee can occur the same day as issuance.

Can a continuous surety bond be cancelled?

Either the principal or the surety can initiate termination with proper notice — 10 business days for the principal on CBP bonds, 30 days for the surety. Termination stops coverage for future obligations but does not eliminate liability for obligations incurred while the bond was active.