Here's what most people in this situation don't know: bad credit does not automatically disqualify you from getting a probate bond. It complicates things — the cost goes up, the process takes longer, and you'll need a more strategic approach — but workable paths exist for most applicants.

This article walks through exactly how credit affects probate bond applications, what your options are, and where the actual hard lines are.

TLDR

- Bad credit raises your premium and routes your application to specialty markets, but rarely blocks approval outright

- Serious disqualifiers are specific: active bankruptcy, fraud convictions, prior bond forfeitures, or prior fiduciary misconduct

- Co-signers, co-indemnity from heirs, and blocked account arrangements each improve your approval position

- Probate bond base rates start at 0.5%–1% of the bond amount; poor credit can push rates to 2%–5% or more

- A bond-only agency with specialty market access — like Atlantic Coast Surety — finds solutions that general insurance brokers typically can't

What Is a Probate Bond?

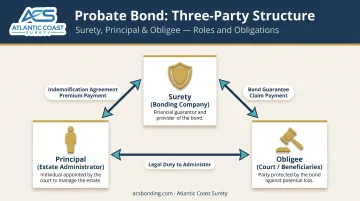

A probate bond (sometimes called a fiduciary bond or estate bond) is a court-required surety bond that protects an estate's beneficiaries and creditors. It guarantees that the estate administrator will manage assets lawfully, follow court orders, and account for everything properly.

The Three-Party Structure

Every probate bond involves three parties:

- The principal — the estate administrator or executor who must obtain the bond

- The obligee — the court and, ultimately, the estate's beneficiaries and creditors

- The surety — the bonding company that issues the bond and backs the guarantee

Probate bonds work differently from insurance. If the administrator mismanages the estate and the surety pays a beneficiary's claim, the administrator must reimburse the surety in full under a personal indemnification agreement signed at application. The surety fronts the payment — it does not absorb the loss.

That repayment obligation is what puts your personal finances under the microscope during underwriting.

Why Surety Companies Check Your Credit for Probate Bonds

Surety underwriters treat credit history as evidence of financial responsibility — specifically, whether you can be trusted to manage someone else's assets and, if needed, repay the surety for any claims paid out.

What Underwriters Actually Look At

Underwriters look well beyond a single score. They evaluate:

- Payment history and past-due amounts

- Credit utilization and available credit limits

- Outstanding judgments, tax liens, or civil actions

- Prior bankruptcies, foreclosures, repossessions, or charge-offs

- Whether any prior bond claims have been filed or paid against you

- Criminal history involving dishonesty or fraud

Atlantic Coast Surety's probate bond application specifically asks whether applicants have suits, liens, or judgments filed against them, have ever filed for bankruptcy, or have ever had a bond claim paid — all of which feed directly into the underwriting decision.

Credit Is One Factor, Not the Only Factor

The full picture includes:

- Size of the estate and complexity of its assets

- Whether an attorney is involved in administration

- Relationships among heirs and any disputes between them

- Pending or active litigation connected to the estate

A weak credit profile doesn't automatically sink an application — but it raises the bar for everything else.

Some agencies offer instant-issue probate bonds with no credit check for smaller estates. Thresholds vary by agency and carrier, but certain providers apply this to estates below approximately $150,000 — not a universal rule, but worth asking about.

How Bad Credit Affects Your Probate Bond Application

Premium Impact

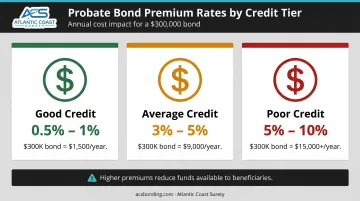

Standard probate bond rates are relatively modest. According to SuretyBonds.com, premiums start at 0.5% of the bond amount for the first $250,000 of coverage. Surety Place notes rates typically fall between 0.5% and 1%, with exceptions up to 3% in complex cases.

Poor credit changes that calculus. While probate-specific credit-tier rate tables aren't publicly standardized, general bad-credit surety benchmarks from SuretyBonds.com show average-credit applicants paying 3%–5% and poor-credit applicants paying 5%–10% of the bond amount. Probate bonds placed through specialty markets for high-risk applicants will likely fall toward the higher end of that range.

On a $300,000 bond, a 0.5% rate costs $1,350 annually. At 5%, that same bond costs $15,000 per year — money that comes directly out of what's available to beneficiaries.

Beyond cost, poor credit changes the approval path entirely. Applications get routed to non-standard or specialty surety markets, which means fewer carriers, additional documentation requirements, and longer processing times. The underlying reason is the repayment obligation: surety underwriters need confidence that a principal can reimburse them if a claim is paid. As JW Surety explains, weak credit signals weaker repayment ability, which drives both higher premiums and tighter scrutiny.

Red Flags vs. Complicating Factors

Not all credit problems carry the same weight. A low score complicates an application; the following issues can push it toward declination in standard markets:

- Active bankruptcy proceedings

- Unresolved tax liens or civil judgments

- Recent foreclosures or repossessions

- Prior bond claims filed or paid against you

The more of these present, the more restricted the available market — and in some cases, the application moves toward declination in standard markets entirely.

How to Get a Probate Bond with Bad Credit

Step 1: Know Your Credit Profile Before Applying

Pull your credit report before submitting any application. AnnualCreditReport.com is the only federally authorized source for free annual reports from all three bureaus. Knowing what an underwriter will see lets you address discrepancies, prepare explanations, and avoid surprises that slow the process.

Step 2: Use a Co-Signer or Co-Indemnitor

A creditworthy co-signer — another heir, a trusted family member, or another interested party — shares indemnification responsibility. This distributes the surety's repayment risk across multiple parties, which can improve approval odds or bring the premium down.

When all estate beneficiaries agree to co-sign the indemnification agreement, the surety's exposure spreads across the entire group. That makes approval more accessible even when the primary administrator has credit challenges.

Step 3: Consider a Blocked Account Arrangement

A blocked account restricts the administrator's access to estate funds without prior court approval. Because the surety's exposure is effectively reduced when funds can't be moved without a court order, the required bond amount decreases — and a smaller bond is easier to obtain, even for higher-risk applicants.

Both California Probate Code and Texas Estates Code explicitly permit administrators to deposit estate assets into restricted accounts to reduce or eliminate bond requirements. Courts in counties like Santa Clara and San Diego have specific forms for this process. Consult an attorney about this option before submitting a bond application — the right structure can simplify placement considerably.

Step 4: Work with the Right Agency

A general insurance broker who handles bonds occasionally is not the same as a bond-only agency with established specialty market relationships. Atlantic Coast Surety operates exclusively in surety bonds, which means faster placement and more options when a standard market says no. Key advantages for hard-to-place applicants include:

- In-house underwriting authority for expedited decisions

- Access to A-rated, Treasury-listed carriers in both standard and specialty markets

- Coverage across commercial, contract, court, and probate bond lines

- Established relationships with specialty markets when standard markets decline

What Disqualifies You from Getting a Probate Bond?

Bad credit alone is rarely a disqualifier. These circumstances are different:

| Factor | Typical Impact |

|---|---|

| Active bankruptcy | Likely disqualifying in standard markets; may require collateral in specialty markets |

| Felony conviction involving fraud or dishonesty | Near-universal disqualifier across most markets |

| Prior surety bond default or forfeiture | Major red flag; limits market access significantly |

| Prior court finding of fiduciary misconduct | Typically disqualifying; may affect legal eligibility to serve |

| Unresolved judgments or tax liens | Serious complicating factor; may still be placeable with additional requirements |

Some disqualifying factors are situational rather than absolute. A resolved bankruptcy may allow placement through specialty markets, sometimes with collateral requirements such as cash deposits or an irrevocable letter of credit equal to a portion of the bond amount. An active, open bankruptcy is a different matter entirely and will close most standard market doors.

State law also affects eligibility directly. New York's Surrogate's Court Procedure Act lists felons and persons found to have demonstrated dishonesty or improvidence as ineligible to receive letters. Florida statute requires removal of a personal representative convicted of a felony. California law allows removal for fraud, waste, or mismanagement.

These are legal eligibility issues — distinct from the bonding question — but the two often intersect. If a court has already found grounds to disqualify you from serving as fiduciary, no bond will resolve that underlying problem.

What Happens If You Can't Get a Probate Bond?

Without the required bond, the court will not issue letters of administration. Assets can't be distributed, creditors can't be paid, and the estate sits in limbo until the bonding requirement is resolved or the court approves an alternative arrangement.

The practical options at that point:

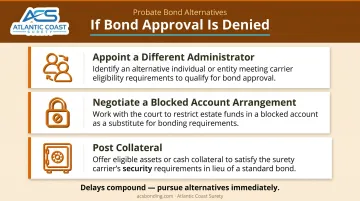

- Appoint a different administrator: Another heir with stronger credit, a professional fiduciary, or a corporate trustee can petition the court to serve instead. Courts generally prefer that all heirs agree on the substitute to avoid additional proceedings.

- Negotiate a blocked account arrangement: Placing estate funds in a court-controlled blocked account may reduce the bond amount to a level where approval becomes achievable — useful when credit is the only barrier.

- Post collateral: In some markets, posting cash or an irrevocable letter of credit equal to the bond amount can substitute for creditworthiness, typically when no substitute administrator is available.

Delays compound quickly. Each week the estate remains unbonded extends the timeline before beneficiaries see any distribution — making it worth pursuing alternatives immediately rather than waiting for the credit situation to resolve on its own.

Frequently Asked Questions

How do I get a probate bond with bad credit?

Apply through a specialty surety agency that has non-standard market access — then consider adding a creditworthy co-signer or requesting a blocked account arrangement to reduce the required bond amount. Atlantic Coast Surety focuses exclusively on bonds, including probate fiduciary placements, and is well-positioned to find workable options for difficult credit profiles.

What disqualifies you from being bonded?

The most common hard disqualifiers are active bankruptcy, felony convictions for financial fraud or dishonesty, prior bond forfeitures, and prior court findings of fiduciary misconduct. Poor credit alone raises costs and routes applications to specialty markets — it is not an automatic bar.

What happens if you can't get a probate bond?

The court will not allow the appointed administrator to proceed. At that point, the estate's heirs can petition to appoint a substitute — another family member with stronger credit, a professional fiduciary, or a corporate trustee — with courts generally preferring unanimous heir agreement on any replacement.

Does bad credit automatically disqualify me from being an estate administrator?

No. Bad credit typically results in higher premiums, additional underwriting requirements (co-signers, collateral), or placement through specialty markets — not automatic disqualification. Most applicants with credit challenges still have clear paths to bonding.

How much more does a probate bond cost with bad credit?

Standard probate bond premiums start at 0.5%–1% of the bond amount, while bad-credit applicants typically fall in the 5%–10% range versus 3%–5% for average credit. Actual probate rates vary by carrier, estate size, and the full underwriting picture.

Can a co-signer help me qualify for a probate bond?

Yes. A creditworthy co-signer shares the indemnification obligation with you, which reduces the surety's repayment risk. This can improve approval odds, bring the premium down, or both — particularly when the co-signer is another heir who has a stake in the estate being properly administered.