The gap between those two scenarios isn't random. It comes down to five variables: bond type, bond amount, your credit profile, how complex the underwriting is, and whether your application is complete the first time you submit it.

This article breaks down realistic timelines by bond type, explains what actually drives delays, and gives you a clear picture of what to prepare before you apply.

Key Takeaways

- Most standard surety bonds are approved within 1 to 3 business days

- Simple license and permit bonds can be issued same-day or within hours

- Large contract or subdivision bonds may take 1 to 4 weeks depending on underwriting scope

- Credit profile, bond amount, and application completeness are the biggest speed factors

- A bond-only specialist routes your submission to the right carrier immediately — no detours through generalist agents

How Long Does It Take to Get a Surety Bond Approved?

The honest answer: anywhere from minutes to several weeks, depending on what you're bonding and who you are on paper.

For most standard surety bonds, approval lands somewhere in the 1 to 3 business day range. But that middle ground hides a wide spread. At Atlantic Coast Surety, the team describes it plainly: "Some bonds can be ready to go in a matter of minutes while some could take much, much longer." The variables are bond type, bond size, and the individual circumstances of the applicant.

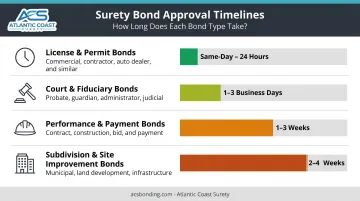

Approval Timelines by Bond Type

| Bond Type | Typical Timeline |

|---|---|

| License & permit bonds | Same-day to 24 hours |

| Court & fiduciary bonds | 1–3 business days |

| Performance & payment bonds | 1–3 weeks |

| Subdivision & site improvement bonds | 2–4 weeks |

License and permit bonds are the fastest category. Many are instant-issue — Colonial Surety notes that applicants can quote, apply, and instantly purchase license and permit bonds online. These bonds are typically low-dollar (often under $25,000), use standardized forms, and require minimal applicant information. Contractor license bonds, motor vehicle dealer bonds, and notary bonds generally fall here.

Court and fiduciary bonds (probate, guardianship, executor, and ERISA) usually process in 1 to 3 business days when documentation is complete. Delays happen when court orders are missing, estate valuations are unclear, or bond amounts push past thresholds that trigger full underwriting review — CNA's fiduciary rate schedules, for example, require full review above $500,000.

Performance and payment bonds for construction contracts require full financial underwriting before a contractor can bid. NASBP's 2024 contract surety guide is clear that prequalification "takes time" and that contractors should prepare before bidding — not after contract award. Underwriters typically need:

- Current financial statements

- Work-on-hand schedules

- Business history and project details

Plan for 1 to 3 weeks minimum.

Subdivision and site improvement bonds are typically the slowest. These involve large dollar amounts, obligee-specific bond form reviews, and sometimes negotiation between the surety and the municipality over bond language. Expect 2 to 4 weeks, sometimes longer when the development agreement needs back-and-forth approval.

What Factors Affect How Long Surety Bond Approval Takes?

Five factors drive the vast majority of approval delays. Most are within your control.

Bond Amount

Dollar amount is the most direct factor. Lower-value bonds — particularly under $25,000 — are often pre-approved with minimal review. Once you cross certain thresholds, carriers shift into full underwriting mode.

Atlantic Coast Surety's contractor compliance bond program illustrates this clearly: bonds up to $25,000 require only basic applicant information, while amounts above that threshold trigger a credit check. For performance and subdivision bonds, the thresholds are higher, but the same logic applies — larger obligations demand deeper financial review.

Credit Profile

Merchants Bonding explains that credit matters because a surety bond is a credit obligation — the surety is essentially extending a guarantee on your behalf, so they assess your creditworthiness accordingly. Strong credit often qualifies applicants for fast-track programs. Weaker credit pushes the file into manual underwriting, which adds days or weeks and may require additional documentation or collateral.

Atlantic Coast Surety's FAQ puts it directly: "It depends on the type of bond and your credit score, which is the biggest factor that determines how high your quote is going to be." The same principle applies to speed, not just price.

Obligee Requirements

Not all bond forms are interchangeable. Government agencies, courts, and municipalities often require specific language, endorsements, or approved bond forms.

When a municipality requires its own custom subdivision bond form, the surety's underwriting team must review and accept that language before issuing. This step adds time regardless of how strong the applicant's financials are.

Application Completeness

This is the most common source of preventable delays — and the most controllable. Incomplete submissions stall the process immediately. Common culprits include:

- Missing financial statements

- Unsigned indemnity agreements

- Incorrect entity name on the application

- Absent co-indemnitor signatures

Atlantic Coast Surety is direct about this: "Any information we request is necessary." Submitting a complete package the first time is the single most reliable way to keep the timeline short.

Carrier Access and In-House Authority

For specialty and harder-to-place bonds, working with an agency that has relationships across multiple A-rated, Treasury-listed carriers matters. When the first carrier declines or needs more time, an agency with in-house underwriting authority can pivot quickly rather than starting over.

Atlantic Coast Surety holds in-house authority for certain bond types, which avoids the back-and-forth of external carrier submissions for eligible bonds — keeping timelines shorter without sacrificing market quality.

Instant-Issue vs. Fully Underwritten Surety Bonds

These two categories operate on completely different timelines, and knowing which one applies to your bond upfront saves a lot of confusion.

Instant-issue bonds are pre-approved by surety companies based on bond type and amount alone. The applicant provides basic information — name, address, license number — and the system returns an approval almost immediately, with no credit pull or financial review. Most small license and permit bonds fall into this category.

Fully underwritten bonds require the surety to evaluate creditworthiness, financial statements, business history, and sometimes project-specific details before issuing. This protects the surety on larger, more complex obligations. Performance bonds, subdivision bonds, and large court bonds all fall here.

How do you know which applies to your bond? Three quick signals:

- A flat-rate online quote with no financials required points to instant-issue

- A request for financial statements or a custom quote signals full underwriting

- Bond amounts above $25,000–$50,000 typically trigger underwriting review, regardless of bond type

Knowing which category applies before you start affects your timeline by days — sometimes weeks.

How to Speed Up Your Surety Bond Approval

You can't bypass underwriting, but you can avoid the delays that come from avoidable mistakes.

1. Gather everything before you submit. For underwritten bonds, that means financial statements, entity formation documents, the obligee's required bond form, and any co-indemnitor signatures. For court bonds, include the court order specifying the bond amount. Incomplete submissions reset the clock.

2. Once the underwriter has your file, respond to document requests the same day if possible. Delays in returning materials slow the entire process — and that lag falls on you.

3. Resist the urge to pressure underwriters. When underwriters feel rushed, they are more likely to choose the safest answer — which is a declination. Patience and responsiveness consistently produce better outcomes than urgency.

4. Work with a bond-only specialist from the start. A general insurance agent may not know which carrier to approach, what documentation is required, or how to structure the submission — and that trial-and-error adds time.

Atlantic Coast Surety focuses exclusively on surety bonds across commercial, contract, subdivision, court, and ERISA categories. That means retail agents reach the right carrier the first time, without the back-and-forth common at generalist shops.

What to Prepare Before Applying for a Surety Bond

Having the right documents ready before you apply is one of the most direct ways to cut approval time. Missing paperwork is the most common cause of preventable delays — and different bond types require very different information. Here's what each category typically requires:

License and permit bonds:

- Applicant name, business name, and address

- Bond amount and obligee name

- License number and bond form from the licensing authority

Court and fiduciary bonds (probate, guardianship, ERISA):

- Complete copy of court order specifying the bond amount

- Estate asset breakdown: cash, stocks, personal property, real estate

- Estate liabilities and number of heirs

- Relationship of applicant to deceased, ward, or minor

- For ERISA bonds: plan name, number of employees with fund access, whether employer securities are held, and plan asset amount

Contract, performance, and subdivision bonds:

- Three years of CPA-prepared corporate fiscal year-end financial statements

- Current personal financial statements (concurrent with corporate year-end)

- Three months of corporate and personal bank statements

- Corporate tax returns for the most recent year

- Work-in-progress schedule separating bonded and unbonded work

- For subdivision bonds: municipal engineer's cost estimate, development agreement, and financing documentation

Submitting a complete package upfront gives underwriters everything they need to move quickly — and avoids the back-and-forth that stretches simple approvals into multi-day processes.

Frequently Asked Questions

How long does it take for a bond request to be approved?

Most surety bond requests are approved within 1 to 3 business days. Simple license and permit bonds can be issued same-day, while complex contract or subdivision bonds can take 1 to 4 weeks depending on bond amount and underwriting depth. The key factor is whether your bond requires full financial underwriting or qualifies for an instant-issue program.

How much do you pay on a $100,000 bond?

It depends on bond type. Construction performance bonds generally run 0.5% to 3% of the contract amount, according to NASBP — so roughly $500 to $3,000 on a $100,000 bond, with stronger credit pushing rates toward the lower end. Court and probate bonds use carrier-specific rate structures that differ significantly.

Can I get a surety bond with bad credit?

Bad credit doesn't disqualify you from most bonds, but it changes the process. Expect higher premiums, possible collateral requirements, and additional documentation requests as the surety takes a closer look at the underlying risk. Some carriers offer non-standard programs specifically for credit-challenged applicants.

What is the difference between a surety bond and insurance?

A surety bond is a three-party agreement between the principal (you), the obligee (who requires the bond), and the surety (who backs your obligations). Unlike insurance — which protects the policyholder — a surety bond protects the obligee, and you're expected to reimburse the surety for any claims paid. It functions more like a credit facility than a policy.

Does the bond amount affect how long approval takes?

Yes, directly. Lower-value bonds are often pre-approved with minimal review. Higher-value bonds trigger full underwriting that requires financial statements, credit review, and sometimes project-specific analysis. The larger the obligation, the more the surety needs to evaluate before committing.