Both uses are legitimate. Both matter in real estate. But they involve separate processes, separate approval criteria, and separate consequences when something goes wrong.

This guide covers both meanings, with primary focus on surety bond approval — the process that contractors, developers, and their insurance agents navigate when a municipality or project owner requires a bond before work can begin.

Key Takeaways

- Bond approval means either a lender approving a home loan (mortgage bond) or a surety company issuing a guarantee for a contractor or developer

- Surety underwriters evaluate three factors: character, capacity, and capital

- Simple license and permit bonds below the standard underwriting threshold can often be issued the same day; subdivision and performance bonds require full underwriting that may take days to weeks

- A denial is not permanent — a specialty bond agency can access markets unavailable through standard carriers

- Incomplete documentation is one of the most common causes of delays and denials

What Does Bond Approval Mean in Real Estate?

The phrase gets used two ways, and confusing them creates real problems.

The Mortgage Bond Context

In a real estate purchase agreement, "bond approval" refers to a buyer securing financing from a lender. According to the National Association of Realtors, a financing contingency is a condition that must be met before a purchase can be completed.

In practice, this approval is often drafted as a suspensive condition in the Offer to Purchase — meaning the entire transaction is suspended until the buyer obtains financing by a specified deadline. If approval isn't secured in time, the agreement typically becomes null and void.

The Surety Bond Context

Surety bond approval is an entirely different process. The Surety & Fidelity Association of America (SFAA) defines a surety bond as a three-party written agreement in which:

- The principal (contractor, developer, or business) obtains the bond

- The surety (insurance company) guarantees the principal's performance

- The obligee (municipality, project owner, or government agency) is protected

The surety isn't lending money. It's vouching for someone's ability to complete a project or fulfill a legal obligation — and agreeing to step in financially if they don't. That's why surety underwriting evaluates financial strength, work history, and project capacity rather than creditworthiness alone.

Who Needs Surety Bond Approval in Real Estate?

- Subdivision developers applying for infrastructure improvement bonds required by municipalities

- General contractors bidding on public or private projects requiring bid, performance, and payment bonds

- Licensed contractors required by state or local authorities to hold a license and permit bond as a condition of operating

Approval in Principle vs. Final Approval

These aren't the same thing — and acting on the wrong one can stall a project:

- Approval in principle: The surety has provisionally agreed to issue the bond, pending additional documentation, a property valuation, or project review. The bond is not yet executable.

- Final approval: The bond is fully executed and ready to be filed with the obligee. This is the version that satisfies a municipal requirement or contract condition.

Types of Real Estate Bonds That Require Approval

| Bond Type | What It Guarantees | Who Requires It |

|---|---|---|

| Subdivision Improvement Bond | Developer completes roads, utilities, drainage per approved plans | Municipalities (e.g., Miami-Dade calculates amounts from engineer's cost estimates) |

| Performance Bond | Contractor completes work per contract terms | Project owners, public agencies; required by federal law on contracts exceeding the Miller Act threshold |

| Payment Bond | Contractor pays subcontractors and material suppliers | Same as performance bonds; often issued together at no additional charge |

| License & Permit Bond | Contractor complies with licensing laws and regulations | State and local licensing authorities |

Not every bond type goes through the same approval process — and the table above only tells part of the story.

The underwriting depth varies significantly across these types. According to Merchants Bonding, most compliance bonds below the standard threshold are instant issue — no underwriting required. Subdivision and performance bonds require a full review of financials, project scope, and contractor history before a surety will commit.

That difference in scrutiny reflects the difference in risk — and it directly shapes how long approval takes and what documentation you'll need to prepare.

The Surety Bond Approval Process: Step by Step

Step 1 — Prepare Your Application Package

Before submitting anything, gather:

- CPA-prepared financial statements (three years, or an opening balance sheet for new companies)

- Personal financial statements

- Three months of corporate and personal bank statements

- Corporate tax returns

- Certificate of insurance

- Resumes of key personnel

- For construction bonds: contractor questionnaire, bonding history, and work-in-progress schedule

- For subdivision bonds: municipal engineer's cost estimate, improvement contracts, and financing details

A complete submission avoids delays — incomplete applications are one of the most common reasons the process stalls.

Step 2 — Submit to a Bond Agency or Surety

For straightforward bonds, applicants submit to a single surety or bond agency. For complex bonds — subdivision improvements, large performance bonds — a wholesale agency like Atlantic Coast Surety submits to multiple underwriters simultaneously to find the best terms, handling that coordination on the applicant's behalf.

Step 3 — Underwriting Review

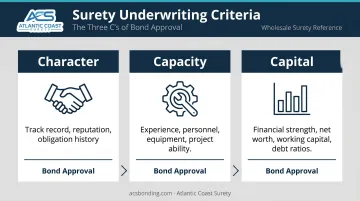

NASBP identifies the Three C's of surety underwriting:

- Character — your track record, reputation, and history of meeting obligations

- Capacity — your ability to complete the work (experience, personnel, equipment)

- Capital — financial strength, working capital, net worth, and debt ratios

The underwriter may request additional documentation during this stage. Pressuring underwriters to speed up the review often backfires. When underwriters feel rushed, they default to the safest decision — a declination. And a declined bond is significantly harder to get approved the second time.

Step 4 — Rate and Terms

Once approved, the surety issues a premium quote. Per NASBP, performance and payment bond premiums are a percentage of the contract amount, determined by underwriting factors including contractor experience and financial strength. License and permit bonds are priced differently and vary by bond amount and jurisdiction. Atlantic Coast Surety offers competitive rates through A-rated and T-listed providers.

Step 5 — Issuance and Filing

After accepting the terms and paying the premium, the surety executes the bond document. It's then delivered to the obligee — the municipality, project owner, or licensing authority — typically via overnight courier, with timing coordinated through the agency.

Because Atlantic Coast Surety works across multiple A-rated, T-listed surety markets, each submission gets reviewed by several carriers. That broader reach tends to produce more competitive pricing and shortens the time to a final decision.

Key Factors That Affect Bond Approval

Credit History

Credit scores — both personal and corporate — are a primary input in surety underwriting. Atlantic Coast Surety describes credit score as "the biggest factor that determines how high your quote is going to be." No universal minimum score applies to all bond types; lower-risk bonds may skip credit checks entirely, while construction and subdivision bonds require thorough credit review. What's clear is that stronger credit means lower premiums and fewer conditions.

Financial Strength and Working Capital

NASBP states that sureties typically require a defined percentage of the requested bonding program in working capital (current assets minus current liabilities). Underwriters also review:

- Net worth

- Debt-to-worth ratios

- Activity and coverage ratios

- Whether the applicant uses percentage-of-completion accounting (preferred by most sureties)

A developer or contractor with strong liquidity and low debt is a better underwriting risk.

Project Experience and Track Record

For construction and subdivision bonds, underwriters want to see comparable project history. A contractor applying for a large performance bond should have successfully completed projects of similar size and complexity. The absence of that track record, not just poor financials, can be enough to slow or stop an approval.

Single Job Size and Aggregate Workload

Underwriters evaluate the specific project being bonded alongside the applicant's total active workload across all projects — bonded and unbonded. Two factors draw particular scrutiny:

- Overextension: Taking on too much simultaneously is a warning sign, regardless of financials

- Aggregate exposure: A contractor already stretched across several large projects may face tighter review on any new application

What to Do If Your Bond Application Is Denied

Review the Denial Reason

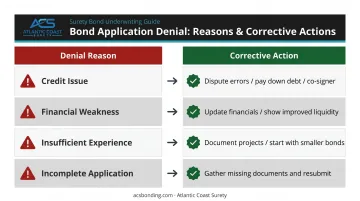

Request a written explanation. The corrective path depends entirely on which factor triggered the denial:

- Credit issue → dispute errors, pay down debt, or provide a co-signer

- Financial weakness → provide updated financials or demonstrate improved liquidity

- Insufficient experience → document completed projects more thoroughly or start with smaller bonds

- Incomplete application → gather missing documents and resubmit

Take Corrective Action Before Reapplying

Depending on the denial reason, corrective steps typically fall into one of these categories:

- Resolving credit issues and waiting for scores to improve

- Bringing in a co-signer or additional indemnitor with stronger financials

- Reducing the requested bond amount

- Completing a smaller project to build a stronger experience record

Denial is rarely permanent. That said, reapplying to the same carrier with the same unchanged information is unlikely to produce a different result.

Work With a Specialty Bond Agency

Standard carriers apply uniform underwriting criteria. Applicants who don't fit that profile are often declined outright, even when a specialty market would write the bond without issue.

Wholesale agencies with access to non-standard markets, like Atlantic Coast Surety, review the complete underwriting picture — financials, experience, project type, and bond size — to identify placement options that a general insurance agent or direct application may not reach.

Frequently Asked Questions

What does bond approval mean?

Bond approval means either a lender has agreed to fund a home purchase (mortgage context) or a surety company has agreed to issue a surety bond after reviewing an applicant's credit, financials, and project qualifications. The two are distinct processes with separate approval criteria and no overlap in how they're evaluated.

How long does the bond approval process take?

Simple license and permit bonds below the standard threshold are often approved the same day or within 24 hours. Construction and subdivision bonds requiring full underwriting can take several days to several weeks, depending on documentation completeness and bond complexity.

Can you be denied a surety bond?

Yes. Surety bond applications are denied when credit, financial strength, or project experience falls short of underwriting standards. Denial is not always permanent. Reapplying with stronger documentation, a co-signer, or through a specialty market frequently results in approval.

What is the difference between a mortgage bond and a surety bond in real estate?

A mortgage bond is a home loan secured against real property. A surety bond is a three-party guarantee that a contractor or developer will fulfill contractual or legal obligations. They serve different purposes — one finances a property purchase, the other guarantees performance of an obligation.

Do subdivision developers need surety bond approval?

Yes. Most municipalities require developers to obtain a subdivision improvement bond before construction begins. The bond amount is typically calculated from a municipal engineer's cost estimate, and approval requires underwriting of the developer's finances, project scope, and completion capacity.

What credit score is needed for surety bond approval?

No universal minimum applies. Low-risk license and permit bonds below the standard threshold often involve no credit check, while construction and subdivision bonds require full credit review. Stronger scores result in lower premiums and fewer conditions, but underwriters weigh the full financial picture — not any single number.