Missing documents are one of the most common reasons pre-approval stalls. Underwriters cannot evaluate what they haven't seen, and incomplete submissions create back-and-forth that delays everything.

This checklist covers what you'll need — organized by category and bond type — so you can submit a complete, organized packet the first time.

Key Takeaways:

- Document requirements vary by bond type, bond amount, and applicant profile

- Both personal and business financials are typically required, even for business bonds

- CPA-prepared financial statements carry more weight than internally prepared ones

- Submitting a complete packet upfront is the single biggest factor in faster pre-approval

- Specialty markets exist for applicants with credit challenges or complex profiles

What Is Bond Pre-Approval and Why Does It Matter?

Surety bond pre-approval is a preliminary underwriting assessment, separate from the bond itself, in which the surety evaluates your creditworthiness, financial strength, and professional qualifications before committing to issue coverage.

Pre-approval signals to project owners, obligees, and municipalities that you are bondable. In competitive bidding and contract award situations, that signal can be the difference between winning and losing a job.

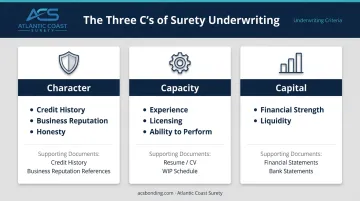

The Three C's Surety Underwriters Evaluate

According to the SBA's surety bonding guidance, underwriters assess applicants across three core dimensions:

| The "C" | What It Measures | Documents That Support It |

|---|---|---|

| Character | Credit history, business reputation, honesty | Personal credit authorization, personal ID, background disclosures |

| Capacity | Experience, licensing, ability to perform | Resume, work history, WIP schedule, contractor license |

| Capital | Financial strength and liquidity | Financial statements, tax returns, bank statements, personal financial statement |

Gaps in any one of these three areas can delay or derail pre-approval — which is why assembling the right documentation upfront matters.

Core Documents Every Bond Applicant Needs

These documents are required for virtually every bond type, regardless of size or category.

Completed Bond Application

Most surety agencies provide their own application form. Atlantic Coast Surety uses internal forms — including an Application Supplementary Questionnaire and an Indemnity Fact Sheet — for most bond types, while carrier-specific forms apply for certain products like ERISA bonds.

Complete every field accurately. Partial or inconsistent answers are a leading trigger for underwriting delays — and they create credibility problems before the underwriter even opens the file.

Government-Issued Photo ID

Required for the applicant and any co-indemnitors (spouses, business partners). Acceptable forms include:

- Driver's license

- Passport

- State-issued ID

Surety bonds involve personal indemnification — owners are personally liable under the General Agreement of Indemnity, so the surety must verify the identity of everyone who signs.

Personal Credit Authorization

Applicants must authorize the surety to pull a personal credit report. NASBP guidance confirms that sureties routinely review personal credit of owners — and in some cases, spouses — as part of the underwriting process.

Personal credit serves as a proxy for character, particularly for smaller bonds or businesses without an extensive operating history. It's reviewed alongside financial statements to give underwriters a complete picture of the applicant.

Personal Financial Statement

A signed, dated personal financial statement listing all personal assets, liabilities, and net worth. Many applicants use the SBA's Form 413 for this purpose, though most surety agencies — including Atlantic Coast Surety — provide their own version.

This document matters because the indemnity agreement makes owners personally liable. Underwriters want to understand personal net worth alongside business financials — the two together paint the full picture.

Professional Resume or Work History

Particularly important for contractor and license bonds. Underwriters are assessing capacity: your track record of completing similar projects, relevant licenses held, and years of industry experience. A resume with verifiable project history directly influences how an underwriter evaluates risk — and can be the deciding factor on borderline applications.

Financial Documents for Bond Pre-Approval

Financial documentation is where most pre-approval submissions are either strengthened or undermined. The depth of documentation required scales with bond size and complexity.

Business Financial Statements (2–3 Years)

NASBP's contract surety guidance specifies that contractors should provide fiscal year-end financial statements for at least the past three years. Standard components include:

- Balance sheet

- Income statement (profit and loss)

- Statement of cash flows

- Footnote disclosures

CPA-prepared or CPA-reviewed statements carry significantly more weight than internally prepared ones. Surety Bond Quarterly notes that CPA-prepared financials help underwriters assess whether character, capacity, and capital align with their underwriting appetite. Atlantic Coast Surety requires CPA-prepared corporate financial statements as its standard across bond types — not internally prepared statements.

NASBP distinguishes three assurance levels: compilations (no assurance), reviews (limited assurance), and audits (highest assurance). Which level is required depends on the carrier and bond amount — thresholds vary by carrier, so confirm requirements directly with your surety.

Business Tax Returns (2–3 Years)

Federal business tax returns for the past two to three years complement the financial statements. They give underwriters an independently verifiable income history — one that carries more credibility than internally prepared numbers alone.

Personal Tax Returns (2–3 Years)

Personal federal tax returns for all owners with a significant ownership stake. For the SBA's Surety Bond Guarantee program, the relevant threshold is 20% ownership or greater under 13 CFR Part 115. For sole proprietors, business and personal returns are typically the same document.

Bank Statements (3–6 Months)

The most recent three to six months of business bank account statements. Underwriters are evaluating liquidity and cash flow patterns — specifically, whether the business has adequate working capital to perform on bonded obligations.

NASBP notes a useful benchmark: sureties typically look for approximately 10% of the requested bonding program in working capital. A $2 million bonding program suggests roughly $200,000 in working capital as a baseline.

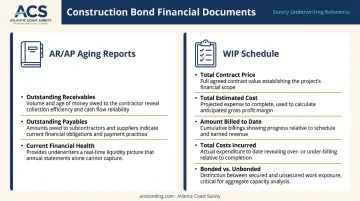

Accounts Receivable/Payable Aging Reports and WIP Schedules

For construction and contract bonds specifically:

- AR/AP aging reports show current financial health and outstanding obligations beyond what annual statements capture

- Work-in-progress (WIP) schedules are required for contractors and should include total contract price, total estimated cost, amount billed to date, total costs incurred, and — critically — a distinction between bonded and unbonded work

Atlantic Coast Surety's WIP format tracks contract identification, financial performance data, change orders, gross profit, retainage, and estimated cost to complete. Contractor-prepared formats are acceptable if they cover these fields, but a CPA-prepared WIP carries more underwriting weight.

Business and Project-Specific Documents

Business Formation and Licensing Documents

- Articles of incorporation or organization

- Operating agreements (for LLCs and partnerships)

- Contractor's license or professional license relevant to the bonded work

These establish legal standing and confirm the applicant has the authority to perform the bonded obligation. An unlicensed contractor cannot be bonded for work requiring a license.

Project Documents for Contract and Construction Bonds

For performance and payment bonds, the surety is underwriting the specific project — not just the company. Required items typically include:

- Bid specifications and project contract or subcontract

- Contract value and project timeline

- Owner/developer contact information

- Bonding method (competitive bid, negotiated, design-build)

Contract terms directly affect the underwriting decision. Unusual risk allocations, aggressive liquidated damages provisions, or shortened completion timelines are red flags that underwriters weigh carefully.

Current WIP Schedule (Contractor Bond Schedule)

A WIP schedule lists all currently bonded projects with contract values, percentage completed, and projected completion dates. Underwriters use it to assess whether a contractor has capacity for additional bonded work. Both bonded and unbonded projects consume working capital, so the full picture matters.

A complete WIP schedule should include:

- Contract name and value for each active project

- Percentage of work completed to date

- Projected completion date

- Whether each project is bonded or unbonded

Subdivision and Site Development Bonds: Additional Requirements

Subdivision bonds carry a distinct and more extensive document set compared to standard contract bonds. Atlantic Coast Surety's subdivision process specifically requires:

- Municipal engineer's cost estimate (with engineer name and contact)

- Municipality-specific bond form, if required by the local government

- Developer's own improvement cost estimates

- Signed contracts or bids from improvement contractors

- Residential or commercial development details (number of units, price range, phasing)

- Full project financing breakdown, including acquisition and development loan details

Subdivision bonds are underwritten against both the developer's financial strength and the municipality's specific requirements. Neither variable exists in standard contract bonding, which is why the document requirements are more extensive.

Additional Documents for Specialized Bond Types

Probate and Fiduciary Bonds

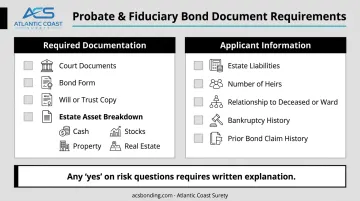

Court-appointed fiduciaries, estate administrators, and guardians need to provide a more legally focused document set. Based on Atlantic Coast Surety's probate bond intake process, required items include:

- Complete copy of all court documents (letters testamentary, letters of administration, or guardianship order)

- The specific bond form required by the court

- Copy of the will or trust, if applicable

- Estate asset breakdown: cash, stocks, personal property, real estate

- Estate liabilities: mortgage, credit card, and other outstanding debts

- Number of heirs

- Applicant's relationship to the deceased or ward

- Bankruptcy history and any prior bond claims

Underwriters also ask a series of risk assessment questions — including whether any applicant has been convicted of a felony, has suits or judgments filed against them, or has had prior custody of estate assets. Any "yes" response requires full written explanation.

The bond amount is set by the court. In many jurisdictions, it's calculated as a multiple of the estate's personal property value — for example, Charleston County Probate Court notes bonds may be required at one-and-a-half times the total value of personal property.

ERISA Fidelity Bonds

Unlike probate bonds, ERISA bonds are federally mandated. ERISA requires that every person who handles funds of an employee benefit plan must be bonded. The bond amount must be at least 10% of plan assets handled in the prior year, with a minimum of $1,000 and a maximum of $500,000 ($1,000,000 for plans holding employer securities).

For ERISA fidelity bond placement, Atlantic Coast Surety (operating through NGM Insurance Company and Spring Valley Mutual Insurance Company in Minnesota) requires the ERISA Bond Information Sheet capturing:

- Number of employees (trustees/administrators) with access to plan funds

- Whether the plan covers union or multi-employer funds

- Any history of dishonesty losses

- Presence of non-qualifying assets or ESOP/employer securities

- Total plan assets (which determines the required bond amount)

- Most recent Form 5500 filing details

A notable program feature: Atlantic Coast Surety's ERISA bonds include an automatic inflation guard endorsement, which increases the bond penalty as plan assets grow — but only when the full ERISA-required bond amount is purchased at inception.

License and Permit Bonds

Compared to probate and ERISA bonds, license and permit bonds are the most straightforward to underwrite. Required documents include:

- State or municipal licensing requirement specifying the required bond amount

- Business license or license application

- Proof of industry certifications or training, where required

- Personal credit authorization (credit is the primary underwriting factor for most small license bonds)

For contractor compliance bonds, Atlantic Coast Surety applies a $25,000 threshold: bonds at or below this amount may qualify for streamlined approval, while bonds above it trigger a mandatory credit check.

How to Prepare and Submit Your Bond Pre-Approval Packet

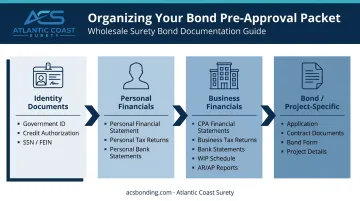

Organize Before You Submit

Group documents into four categories before initiating pre-approval:

- Identity documents — government ID, credit authorization, SSN/FEIN

- Personal financials — personal financial statement, personal tax returns, personal bank statements

- Business financials — CPA-prepared financial statements, business tax returns, business bank statements, WIP schedule, AR/AP aging reports

- Bond/project-specific — application, contract documents, bond form, project details

Submitting a complete, organized packet in one pass reduces back-and-forth and moves the file through underwriting faster. Atlantic Coast Surety accepts submissions by email at ANNAB@ACSBONDING.COM or by fax at 201-661-7364.

Common Document Mistakes That Cause Delays

- Stale financials: Statements more than 12 months old may not be accepted for larger bonds

- Internally prepared financials: For significant bond amounts, underwriters expect CPA-prepared statements

- Missing co-indemnitor information: Spouses and business partners above certain ownership thresholds must be included

- Incomplete project documents: For contract bonds, missing contract terms or WIP schedules create gaps that underwriters must chase down

- Unanswered application questions: Any blank field — especially on background/risk questions — flags the file for follow-up

What Happens After Submission

The surety reviews the complete file, may request clarification or additional items, and issues either a pre-approval with a bond rate or a declination. Turnaround varies widely — some bonds are approved within minutes, while large construction bonds requiring full financial review take several days or more.

Once a bond line is established, subsequent requests move significantly faster.

That speed depends in part on working with a specialist who knows exactly what each carrier requires. Atlantic Coast Surety has operated exclusively in surety for over 20 years, with access to both standard and specialty markets — so they can identify the right documents for a specific bond type and match applications to the right carrier from the start.

Frequently Asked Questions

What documents do I need to provide for bond pre-approval?

The core documents are: completed application, government-issued photo ID, personal financial statement, business financial statements for the past two to three years, business and personal tax returns, bank statements, and any bond- or project-specific documents. Exact requirements vary by bond type and amount — contract bonds require significantly more than small license bonds.

How do I get pre-approved for a bond?

Complete the bond application, gather your financial and business documents, and submit the full package to a surety company or bond agency for underwriting review. A bond-only agency shops your application across multiple surety markets based on your financial profile and bond type, which directly affects both approval odds and the premium rate you receive.

How much income do I need to be pre-approved for a $300,000 bond?

Surety underwriting has no single income threshold. Underwriters evaluate overall net worth, liquidity, debt load, and business performance relative to the bond amount. As a benchmark, NASBP notes sureties typically look for roughly 10% of the requested bonding program in working capital, though requirements vary by carrier and bond type.

How long does surety bond pre-approval take?

Pre-approval can range from minutes (small license and permit bonds with strong credit) to several weeks (large construction bonds requiring full financial review). Submitting a complete document package upfront is the single biggest factor in shortening turnaround time. Once a bond line is established with a surety, additional bond requests move considerably faster.

Can I get a surety bond with bad credit?

Poor credit doesn't automatically disqualify an applicant. NASBP describes non-standard underwriting programs specifically designed for emerging, small, and minority-owned businesses, and the SBA's Surety Bond Guarantee program provides an additional pathway. Applicants with credit challenges typically face higher premium rates or collateral requirements. An agency with access to specialty markets, such as Atlantic Coast Surety, can identify carriers most likely to approve non-standard applications at competitive rates.

Does applying for bond pre-approval affect my credit score?

Most surety underwriters pull a personal credit report as part of pre-approval, and practices vary by carrier. Submitting applications to multiple surety companies in a short window may trigger separate inquiries, so working through a single agency that shops multiple markets on your behalf helps limit unnecessary credit pulls.