Introduction

Not all performance bonds are created equal. Signing the wrong one without understanding its implications can expose contractors and project owners to serious financial risk.

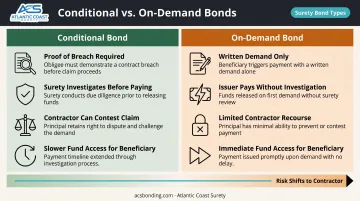

Contractors and project owners across the US regularly encounter performance bond requirements in contracts, but the two core types (conditional and on-demand) function very differently. A conditional bond requires the beneficiary to prove breach and demonstrate actual loss before the surety pays. An on-demand bond allows the beneficiary to draw funds immediately, regardless of whether the contractor is actually at fault.

That distinction matters enormously. For contractors, accepting an on-demand bond in a disputed situation can mean paying out significant sums before any resolution is reached. For project owners, requiring a conditional bond means accepting a longer claims process when things go wrong.

This article breaks down how each bond type works in practice, where each typically appears, and what to weigh before signing.

Key Takeaways

- Conditional bonds require proof of contractor breach and actual financial loss before the surety pays, the standard form in US domestic contracts.

- On-demand bonds allow the beneficiary to call funds immediately, with no requirement to prove default.

- The contract or tender documents determine which type is required; contractors rarely get to choose.

- Bond premiums are a percentage of contract value, with on-demand bonds generally costing more than conditional bonds.

- Bond wording controls legal function: a label of "on-demand" means nothing if the language implies conditions.

Conditional vs. On-Demand Performance Bonds: Quick Comparison

| Feature | Conditional Bond | On-Demand Bond |

|---|---|---|

| Claim trigger | Proven breach + demonstrated financial loss | Written demand only — no proof of default required |

| Obligation type | Secondary (tied to underlying contract) | Primary/autonomous ("pay first, argue later") |

| Typical issuer | Surety/insurance company | Bank |

| Common context | US domestic construction, government, commercial contracts | International projects, FIDIC-based contracts |

| Risk to contractor | Lower — unfair calls can be contested | Higher — funds can be drawn without proven fault |

| Premium cost | Generally lower | Generally higher due to greater issuer exposure |

The table above reflects general market practice — but two practical exceptions apply before treating these categories as fixed:

- Bond title ≠ bond type. Courts have found that a bond described as "on-demand" can still function as conditional if the wording requires preconditions before payment — as illustrated in Vossloh Aktiengesellschaft v Alpha Trains (UK) Ltd, cited by both CMS Law and Fenwick Elliott.

- Mixed-form bonds require line-by-line review. Some bonds are payable on demand in insolvency situations but otherwise conditional. These instruments don't fit neatly into either category and warrant careful review before execution.

What Is a Conditional Performance Bond?

How It's Defined

A conditional performance bond is a surety instrument where the bonding company only pays if specific pre-defined conditions are satisfied. Most commonly, this means two things must be true: the contractor failed to fulfill their contractual obligations, and the beneficiary suffered a quantifiable financial loss as a direct result.

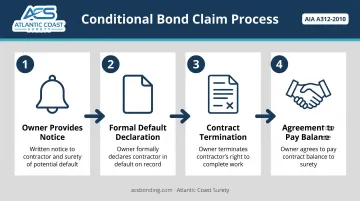

Under the AIA A312-2010 (one of the most widely used standard performance bond forms in US construction), the surety's obligation doesn't arise until the owner has provided notice of considering contractor default, formally declared default, terminated the construction contract, and agreed to pay the contract balance to the surety or a replacement contractor. That's a multi-step process, not a simple claim submission.

The Claim Process

The beneficiary must present real evidence to support a conditional bond claim:

- Documentation of the contractor's non-performance (missed deadlines, substandard work, financial insolvency)

- Quantified financial loss — typically the additional cost to complete the work with a replacement contractor

- Compliance with all notice requirements specified in the bond

Sureties investigate before paying. The Surety Information Office confirms that performance bond claims involve notice and default analysis, surety investigation, and review of both bond terms and the underlying contract before any payment or completion option is selected.

Where Conditional Bonds Are Used

In the US, conditional performance bonds are the dominant form. They appear across:

- Construction contracts — from residential builds to large commercial projects

- Government and public works — federal construction contracts above the applicable threshold require performance bonds under the Miller Act (40 U.S.C. § 3131), with bond amounts generally equal to the original contract price per FAR 28.102-2

- Subdivision development agreements — municipalities require bonds guaranteeing site improvement completion

- Commercial service contracts — where proving breach is an accepted and reasonable standard

Federal sureties must also be approved under Treasury Circular 570 and meet FAR 28.202 requirements — a further layer of accountability built into the US framework.

Contractor Protections and Beneficiary Trade-Offs

Conditional bonds offer contractors meaningful protection. Because the beneficiary must substantiate a claim with evidence, a call cannot succeed simply because an owner is dissatisfied or alleges a breach without proof. Contractors facing a disputed claim have the opportunity to contest it before funds are drawn.

The trade-off for beneficiaries: access to funds isn't immediate. Proving breach and quantifying loss takes time, which can complicate project completion if a contractor defaults mid-construction and a replacement is needed quickly.

What Is an On-Demand Performance Bond?

How It Works

An on-demand bond — also called an unconditional bond or demand guarantee — operates on a different basis entirely. The surety or bank must pay the beneficiary upon a valid written demand, without any requirement to prove contractor default or demonstrate financial loss. The bond obligation exists independently from the underlying contract.

Pinsent Masons describes this as a "pay first, argue later" mechanism, where the beneficiary's demand itself is treated as conclusive evidence of entitlement. The issuer cannot investigate or challenge the merits of the underlying dispute before paying.

Key mechanics at a glance:

- Payment triggered by written demand alone — no proof of default required

- Bond obligation is independent of the underlying construction contract

- Issuer has no right to investigate or delay based on disputed facts

The only recognized exception is clear fraud. Per Taylor Wessing's analysis of Power Projects Sanayi v Star Assurance Company Limited, the issuer must honor the bond according to its terms unless there is clear fraud of which the issuer has notice at the time of demand.

Clifford Chance also identifies narrow contractual exceptions where the issuer may resist a demand if it can positively establish the beneficiary has no right to call — but these cases are uncommon and jurisdiction-dependent.

Where On-Demand Bonds Appear

On-demand bonds are standard in international construction and infrastructure. FIDIC's 2019 briefing note confirms the increasing use of on-demand bonds in international projects, under which a bank is obligated to honor the bond because it is payable on demand. The World Bank's Standard Procurement Documents for Works — built on FIDIC 2017 Red Book conditions — allow performance security in either demand guarantee or performance bond form, with demand guarantees subject to the ICC's Uniform Rules for Demand Guarantees (URDG 758).

Common contexts include:

- Cross-border construction contracts

- Projects governed by FIDIC conditions

- Infrastructure financing in regions where beneficiaries require maximum financial certainty

Risk Implications for Contractors

Given how widely on-demand bonds appear in international work, contractors need to understand what they're agreeing to. These instruments shift risk sharply toward the contractor. Because a call requires no proven fault, contractors face the possibility of significant funds being drawn during a legitimate dispute — before any adjudication occurs. This creates real cash flow exposure that can strain operations. On large projects where bond values represent meaningful capital, that exposure can become a serious operational problem before any dispute is even heard.

Conditional vs. On-Demand: Which Bond Is Right for Your Project?

You Usually Don't Get to Choose

In most cases, the type of performance bond required is dictated by the contract, tender documents, or the obligee. Contractors should review these documents thoroughly before signing — not after — to understand their exposure.

The contract framework generally determines the answer:

- Expect a conditional bond for domestic US construction, subdivision development, government contracts, and most commercial service agreements

- Expect an on-demand bond for international projects, especially those governed by FIDIC contracts or in jurisdictions where demand guarantees are the legal norm

- When the contract is silent or ambiguous, get clarity in writing before execution — don't assume based on the label alone

Cost Considerations

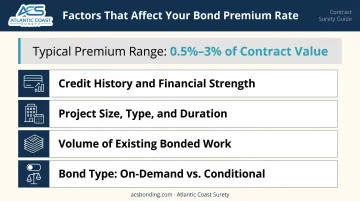

According to NASBP, performance bond premiums are a percentage of the contract value, with well-qualified contractors with strong financials securing rates toward the lower end of the available range. Newer firms or those with limited credit history may fall toward the higher end.

Key factors that affect your rate:

- Credit history and financial strength

- Project size, type, and duration

- Volume of existing bonded work in progress

- Bond type — on-demand bonds generally carry higher premiums because the issuer assumes greater risk without the ability to evaluate the underlying claim before paying

Why Bond Wording Matters More Than the Label

A bond labeled "on-demand" doesn't automatically function as one. Courts have ruled — as in Vossloh — that if the overall instrument requires conditions to be met before payment, those conditions control regardless of how the bond is described.

Ambiguous wording creates risk for both sides:

- Beneficiaries who assume they have an on-demand right may face a contested conditional claims process

- Contractors who assume they're protected by a conditional bond's evidence requirements may find the language doesn't support that reading

Bond language should be reviewed by someone with genuine surety expertise before the contract is executed — not after a dispute arises.

Working with a Specialized Surety Agency

Insurance agents and brokers whose clients face performance bond requirements — whether standard or specialty — benefit from partnering with a wholesale surety specialist. Atlantic Coast Surety, a bond-only agency based in Mahwah, NJ, with 20+ years of experience, provides access to A-rated, T-listed carriers across both standard and specialty markets.

Their in-house underwriting authority enables faster placement on complex or non-standard bond forms. For agents navigating unusual contract frameworks or wording questions, working with a dedicated surety wholesaler provides both technical depth and competitive rates.

Conclusion

The distinction between conditional and on-demand performance bonds isn't academic — it determines who bears financial risk and when funds can be accessed.

Conditional bonds create a claims process grounded in evidence, protecting contractors from unfounded calls while giving sureties the ability to investigate before paying. On-demand bonds prioritize the beneficiary's immediate access to funds, regardless of whether fault has been established. The right bond is simply the one the contract requires — understood clearly by all parties before signing.

For contractors, agreeing to an on-demand bond without recognizing the implications can mean serious cash flow disruption during a disputed call. For project owners, conditional bonds offer a structured resolution process that takes time. Both parties are better served by consulting an experienced surety professional who can review bond language and identify the right instrument before a contract is signed.

Frequently Asked Questions

What is a conditional performance bond?

A conditional performance bond is a surety instrument where the bonding company only pays out if the beneficiary proves the contractor breached the contract and that a financial loss resulted. It's the standard performance bond form in US domestic construction and commercial contracts, and it gives contractors meaningful protection against unfounded claims.

How much does a performance bond cost?

Performance bond premiums are a percentage of the contract value, averaging lower rates for contractors with solid financials and a clean credit history. Key rate factors include project size, duration, bonding history, and the contractor's financial strength. On-demand bonds generally cost more than conditional bonds because issuers assume greater risk without evaluating the underlying claim.

What are the two types of performance bonds?

The two core types are conditional bonds, which require proof of contractor breach and demonstrated financial loss before payment, and on-demand bonds, which pay upon a written demand without requiring proof of default. The choice between them directly affects claim rights, risk allocation, and premium cost.

Can a contractor challenge an on-demand performance bond call?

Successful challenges are rare. The primary recognized exception is clear fraud: if the beneficiary's call is fraudulent and the issuer has notice of it, payment may be withheld. Courts otherwise uphold on-demand bond calls as long as they are not in obvious breach of the underlying contract terms.

Which type of performance bond is most common in the US?

Conditional performance bonds are far more common in US domestic construction and commercial contracts. On-demand bonds appear primarily in international projects — particularly those governed by FIDIC contracts — or in specific contract frameworks that require demand guarantees rather than traditional surety bonds.