Confusing a bid bond with a performance bond, or missing a payment bond requirement entirely, can disqualify a bid or leave a project owner without adequate protection. This guide breaks down what procurement bonds are, how they function, and what contractors and commercial buyers need to understand before signing a contract or submitting a bid.

Key Takeaways

- A procurement bond is a surety instrument guaranteeing that a party will fulfill a specific obligation in a procurement or supply transaction

- Three parties are always involved: the principal (contractor or buyer), the obligee (project owner or supplier), and the surety (the bonding company)

- Bid bonds, performance bonds, and payment bonds are the most common types — each protecting a different stage of the contract lifecycle

- Premiums typically range from 0.5% to 3% of the bond amount, making bonds more capital-efficient than cash deposits or letters of credit

- If the principal defaults, the surety compensates the obligee and then seeks reimbursement from the principal

What Is a Procurement Bond?

A procurement bond is a surety instrument that binds three parties — principal, obligee, and surety — to ensure a specific obligation within a procurement transaction is fulfilled. If the principal fails to perform, the surety compensates the obligee up to the bond's stated maximum (the penal sum).

In competitive bidding environments and large-scale supply agreements, project owners have no reliable way to independently verify a contractor's financial credibility. A bond fills that gap more efficiently than cash deposits — without requiring either party to tie up significant capital.

What a Procurement Bond Is Not

How claims work — and who absorbs losses — differs from other financial instruments:

- Insurance pays losses and keeps them; a surety pays out, then recovers from the principal

- Letters of credit require cash collateral upfront; bonds are obtained for a fraction of the guaranteed amount

- Direct payment guarantees pay on demand; a bond only triggers if the principal actually defaults

As NASBP and SFAA describe it, surety bonds function more like credit instruments than traditional insurance. The principal remains primarily liable and must reimburse the surety for any losses paid out.

Two Distinct Uses of the Term

The phrase "procurement bond" can describe two different things:

- Bonds required during a procurement process — bid bonds, performance bonds, and payment bonds that contractors submit to project owners

- Purchase guarantee bonds — used in supply chain contexts where a buyer guarantees to a supplier that contracted purchases will be made

In federal contracting, performance and payment bonds are governed by the Miller Act (40 U.S.C. Chapter 31), with FAR 28.102-1 requiring these bonds on federal construction contracts exceeding $150,000.

How Does a Procurement Bond Work?

A procurement bond moves through a defined sequence: underwriting, issuance, active performance, and — if things go wrong — a claim. All three parties play a role at each stage.

The Three Parties

| Party | Role | Liability |

|---|---|---|

| Principal | Purchases the bond; must perform the obligation | Reimburses surety if a claim is paid |

| Obligee | Requires the bond; receives its protection | Files a claim if the principal defaults |

| Surety | Underwrites and issues the bond | Compensates obligee up to the penal sum |

The surety's evaluation before issuing a bond is rigorous. According to NASBP and SFAA, underwriters assess the principal's reputation, management team, track record, working capital, and financial strength — not just credit scores. This prequalification is part of what makes a surety bond meaningful to the obligee.

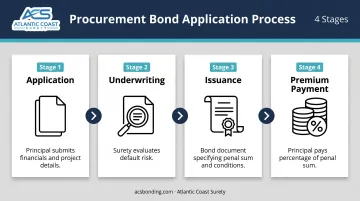

From Application to Issuance

That prequalification happens during a structured application process:

- Application — the principal submits financial statements, credit history, and project details; the surety uses these to assess default risk before agreeing to anything

- Underwriting — the surety evaluates default risk and decides whether to issue the bond

- Issuance — if approved, the surety issues a bond document specifying the penal sum, the obligee, and the conditions that trigger a claim

- Premium payment — the principal pays a premium (a percentage of the penal sum, not the full amount) to secure the guarantee

When a Claim Is Filed

A performance bond claim is typically triggered when the obligee declares the principal in default and formally terminates the contract. According to the AGC/SFAA Contract Surety Bond Claims Guide, the surety then investigates and may respond in several ways:

- Tender a replacement contractor to complete the work

- Take over and complete the project directly

- Provide financial or technical support to the principal

- Pay completion costs up to the bond's penal sum

After compensating the obligee, the surety exercises its indemnity rights — pursuing the principal to recover what was paid out. Unlike insurance, where losses transfer to the carrier, surety bonds keep the loss with the party who caused it.

Types of Procurement Bonds

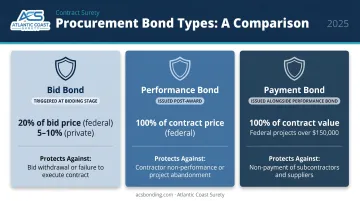

Bid Bonds

Required at the bidding stage, a bid bond guarantees that a contractor will enter into the contract at their bid price if selected, and will provide any required follow-on bonds. If the contractor withdraws after winning, the obligee can claim the difference between the winning bid and the next acceptable bid.

- Federal projects: bid guarantee must be at least 20% of the bid price (capped at $3M) per FAR Subpart 28.1

- Private projects: typically 5% to 10% of the bid price

Performance Bonds

Issued after a bid is accepted, a performance bond guarantees the contractor will complete the work according to contract terms. If the contractor fails or the work is defective, the surety compensates the project owner or arranges for completion.

- Required at 100% of the contract price on federal construction contracts under FAR 52.228-15

- Apply to both public and private construction projects

Payment Bonds

Typically issued alongside performance bonds, a payment bond guarantees that subcontractors, laborers, and material suppliers will be paid. It protects the entire supply chain from non-payment.

- Also required at 100% of the contract value on federal projects over $150,000

- Claimants must provide written notice and documentation such as invoices, subcontracts, and delivery records

Purchase Guarantee Bonds

While the bond types above apply primarily to construction, purchase guarantee bonds operate in a broader supply chain context — particularly in renewable energy and large infrastructure projects. They guarantee that a buyer will purchase specified materials or components from a supplier as contracted. If the buyer doesn't follow through, the supplier can claim against the bond for financial losses.

This makes purchase guarantee bonds a practical alternative to letters of credit: they secure supply agreements without requiring the buyer to tie up cash upfront.

Where Procurement Bonds Are Required

Public Sector

Bond requirements in public contracting aren't optional — they're statutory.

- Federal contracts: the Miller Act mandates performance and payment bonds on construction contracts exceeding $150,000, enforced through FAR 28.102-1

- State and local contracts: NASBP confirms that nearly all 50 states have enacted "Little Miller Act" statutes with parallel requirements

State thresholds vary considerably. Texas requires a performance bond when a public works contract exceeds $100,000 and a payment bond when it exceeds $25,000 under Texas Government Code 2253.021. Alabama's threshold under Ala. Code 39-1-1 is $50,000.

Contractors working across multiple states should confirm each jurisdiction's requirements before bidding — each state sets its own threshold.

Private Sector and Commercial Contexts

Private projects aren't bound by the Miller Act, but bond requirements still appear regularly:

- Large private construction projects where owners want financial protection

- Renewable energy developments securing turbine, panel, or battery supply agreements

- Commercial contracts where one party needs assurance of another's financial commitment before committing inventory or resources

How Much Does a Procurement Bond Cost?

The cost of a procurement bond is expressed as a premium — a percentage of the bond's penal sum. Industry benchmarks from AIA Contract Documents put the typical range at 0.5% to 3% of the contract amount, with well-qualified applicants securing rates toward the lower end.

To put that in concrete terms: a contractor purchasing a $500,000 performance bond at a 1% premium pays $5,000 — while the bond provides $500,000 in coverage to the project owner without requiring that capital to be set aside. That's the core efficiency advantage bonds have over cash deposits or letters of credit, where Chubb notes that pledging collateral ties up capital and affects existing credit lines.

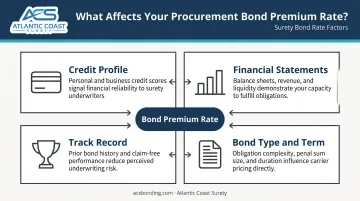

What Affects Your Rate

Surety underwriters look at several factors when pricing a bond:

- Credit profile — personal and business credit history

- Financial statements — working capital, net worth, liquidity

- Track record — completed projects, bonding history, references

- Bond type and term — performance bonds vs. bid bonds carry different risk profiles

Applicants with strong financials and a clean bonding history qualify for lower rates. Those with weaker credit or limited history may pay more — or require placement through specialty markets rather than standard carriers.

That's where market access matters. Atlantic Coast Surety is a bond-only agency with 20+ years placing contract bonds through A-rated, T-listed carriers across both standard and specialty markets. For retail agents and their contractor clients, that breadth of access means the right rate for the account — not just the rate a single carrier is willing to offer.

Frequently Asked Questions

What is a bond in procurement?

A procurement bond is a surety instrument where a licensed bonding company guarantees that a principal will fulfill a specific contractual obligation — winning a bid, completing work, or paying subcontractors. If the principal fails, the surety compensates the obligee and then seeks reimbursement from the principal.

How much does a procurement bond cost?

Premiums typically range from 0.5% to 3% of the bond's penal sum, depending on the applicant's credit, financial strength, and bond type. A $100,000 bond might cost $500 to $3,000 per year, with businesses that have strong financials generally qualifying for rates on the lower end of that range.

What happens if a contractor defaults on a procurement bond?

The obligee files a claim with the surety, which investigates and, if valid, compensates the obligee up to the bond's penal sum. Resolution may come through a replacement contractor, direct completion, or a cash settlement. The surety then seeks reimbursement from the principal under the indemnity agreement.

How is a procurement bond different from a letter of credit?

A letter of credit requires the applicant to pledge or collateralize cash, directly limiting available capital and affecting credit lines. A procurement bond is obtained for a premium that's a fraction of the covered amount, leaving the principal's capital free for operations.

Who typically needs a procurement bond?

Procurement bonds are most commonly required for contractors bidding on public or private construction projects, commercial businesses entering large supply or service agreements, and developers — such as those in renewable energy — who must guarantee material purchase commitments to suppliers.

Are procurement bonds the same as bid bonds?

A bid bond is one type of procurement bond — specifically used at the bidding stage to guarantee a contractor will honor their bid if selected. The broader category also includes performance bonds, payment bonds, and supply guarantee bonds, each covering a different obligation across the contract lifecycle.