The gap isn't understanding what a bond is. Most contractors know a performance bond protects the project owner if they fail to complete the work. The real gap is understanding what a surety bond agent actually does — and why choosing the right one directly affects how much work a contractor can bid, win, and execute simultaneously.

The agent is the person who makes the bonding program work. Get this relationship right, and bonding becomes a growth tool. Get it wrong, and it becomes a ceiling.

Key Takeaways

- A surety bond agent is a licensed intermediary who connects contractors with surety companies and manages the bonding process on their behalf.

- Agents evaluate a contractor's financial profile before approaching any underwriter — flagging weaknesses before they trigger a denial.

- A skilled agent advocates for your qualifications directly with underwriters, going beyond form submissions to make a case for approval.

- Bond-only specialists offer deeper carrier relationships and access to specialty markets most general agents can't reach.

- The right agent builds your bonding capacity over time, positioning you for larger contracts as your business grows.

What Is a Surety Bond Agent?

A surety bond agent — sometimes called a surety bond producer — is a licensed intermediary who represents contractors in the surety market. As NASBP defines it, surety bond producers are "business professionals who specialize in providing contract surety bonds to contractors, subcontractors, and other construction project participants."

Three parties are involved in every surety bond transaction:

- The principal — the contractor who needs the bond

- The obligee — the project owner requiring the bond

- The surety — the company that financially backs the bond

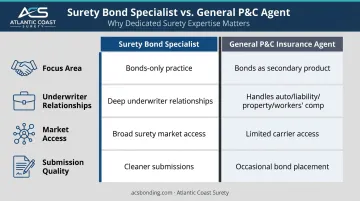

The agent sits outside this triangle. They represent the contractor in obtaining the bond from the surety, but they are not the surety company itself, not the project owner's representative, and not the same as a general property/casualty insurance agent who occasionally places a bond.

That distinction matters more than most contractors realize. A general P&C agent handles auto, liability, workers' comp, and property coverage — bonds are a secondary product. A surety specialist's entire practice is built around bond placement. That focus translates directly into stronger underwriter relationships, broader market access, and cleaner submissions that are less likely to stall or come back with unfavorable terms.

Licensing Requirements

Licensing is what separates a qualified surety specialist from a generalist broker who handles bonds as an afterthought. Per NASBP licensing standards, agents must be licensed by the state department of insurance in every state where they operate — a process requiring coursework, a written examination, and a background check. That requirement exists because surety underwriting has a technical foundation that general P&C training doesn't cover.

What Does a Surety Bond Agent Do for Contractors?

A surety agent's role spans the full arc of a contractor's bonding relationship — from initial qualification through long-term capacity growth. It's not a transactional service that activates only when a bond is needed.

Prequalification and Financial Assessment

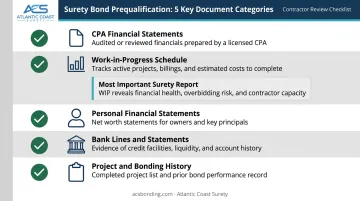

Before approaching any surety company, the agent evaluates the contractor's financial health internally. This includes reviewing:

- CPA-prepared financial statements (typically three years)

- Work-in-progress (WIP) schedule

- Personal financial statements from all owners

- Bank lines of credit and recent bank statements

- Project history, backlog, and bonding history

According to IRMI, the WIP schedule is "one of the most important reports produced by contractors and is relied on heavily by the surety." Overbillings and underbillings translate directly onto the balance sheet — and an agent who catches those discrepancies before submission prevents them from becoming reasons for denial.

A skilled agent identifies gaps early: incomplete WIP data, low assurance-level financial statements, missing affiliated company financials, or accounting basis mismatches that obscure true job profitability. Fixing these before submission is far better than explaining them to an underwriter who's already skeptical.

Matching Contractors with the Right Surety Company

Surety companies aren't interchangeable. They have different underwriting appetites, capacity thresholds, and specialties. An agent who works with multiple markets — both standard and specialty — matches each contractor to the surety whose risk tolerance fits their profile.

Standard markets work well for contractors with established financial histories, clean bonding records, and strong credit. Specialty markets serve contractors who don't fit that mold: newer companies, contractors with prior losses, those with credit challenges, or those pursuing niche project types like waste hauling, subdivision bonds, or transportation bonds.

An agent without access to specialty markets simply can't help certain contractors — even capable ones with legitimate bonding needs.

Negotiating Bonding Capacity with Underwriters

The agent acts as the contractor's advocate with the underwriter: presenting strengths, providing context for weaknesses, and negotiating both the single-project limit and the aggregate bonding line. The underwriter relationship matters enormously here.

Agents who pressure underwriters directly tend to get the safest possible answer, which is often a decline. A declined bond creates a record that complicates every future approval attempt. The agent's job is to present the file persuasively — not push for a rushed decision.

Atlantic Coast Surety has built carrier relationships over 20+ years specifically to present contractor files at the right time, in the right way, to maximize approval outcomes.

Ongoing Advisory and Business Support

The agent's job doesn't end at bond issuance. A good agent advises on how financial decisions affect bonding capacity, when to pursue program expansion, and how to manage backlog relative to bonding limits. They also refer contractors to construction-focused CPAs, attorneys, and bankers who understand the specific demands of the surety relationship.

How a Surety Bond Agent Helps You Through the Bonding Process

The bonding process follows a defined sequence, and the agent's job is to move you through each stage efficiently and with the strongest possible presentation.

Application and Document Collection

The agent collects everything needed to build a complete underwriting submission:

- CPA-prepared corporate financial statements (past three years, or an opening balance sheet for new companies)

- Personal financial statements from all owners

- Three months of corporate and personal bank statements

- Corporate tax return (most recent year)

- Work-in-progress schedule covering all active contracts — bonded and unbonded

- Project history: five largest completed contracts with contract prices, owners, and design professionals

- Business references: suppliers, subcontractors, and architects

- Key personnel resumes and organization chart

- Details on the specific bond being requested

Documentation requirements vary by bond type and size. For performance bonds specifically, the submission also includes how the job was bid, the spread between the low and second-low bidder, and the current dollar amount of work in progress.

Underwriting Submission and Presentation

The agent doesn't just forward documents. They build a submission package that contextualizes the contractor's profile: operational depth, personnel experience, banking relationships, project references, and a forward-looking view of anticipated bond needs.

Company brochures, reference letters, and architect contacts aren't afterthoughts. Underwriters weigh the human capital behind the numbers just as heavily as the financials in construction bonding.

Bond Issuance and Capacity Setting

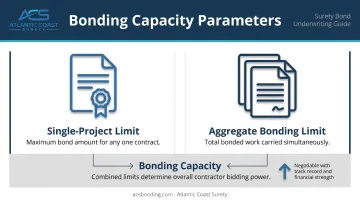

At approval, the surety establishes two key parameters:

- Single-project limit: The maximum bond amount for any one contract

- Aggregate bonding limit: The total bonded work the contractor can carry simultaneously

As CFMA explains, bonding capacity is "the maximum amount of surety credit a surety company will provide to a contractor," encompassing both single-job and aggregate limits. Both numbers control which projects a contractor can bid. A strong agent negotiates both upward from the start.

Renewals, Claims, and Capacity Growth

Once a contractor establishes a bond line, future requests move faster. The agent monitors performance, manages renewals, assists if a claim is filed, and builds the ongoing case for increased capacity as the contractor's financial profile strengthens.

Capacity growth milestones that support higher limits include: audited financial statements showing revenue growth, a larger confirmed bank credit line, a clean claims history, and a track record of successfully completing contracts at or near the current single-project limit.

What to Look for in a Surety Bond Agent

Not every agent is equally equipped to serve a contractor's bonding needs. The right agent should:

- Specialize in construction bonding — not handle it as one product among many

- Work with multiple surety markets — both standard and specialty

- Hold valid state licenses in every state where the contractor operates

- Have established underwriter relationships — not just carrier appointments

Before engaging an agent, ask these questions directly:

- How many surety companies do you work with?

- What percentage of your clients are contractors?

- Are you licensed in the states where I work?

- Do you have access to specialty markets for harder-to-place accounts?

- Do you have in-house underwriting authority, and for what bond types?

The Bond-Only Specialist Advantage

Working with a bond-only agency changes the dynamic in practice. Because their entire practice is surety, they develop deeper underwriter relationships, reach a broader range of specialty markets, and build stronger submission packages than generalist agents who handle bonds occasionally.

Atlantic Coast Surety operates exclusively in surety — no property, casualty, or other insurance lines. With 20+ years of experience and in-house underwriting authority granted by their carrier partners, the firm works with A-rated, T-listed providers, meaning bonds placed meet the financial strength standards required for federal and public works contracts.

Their access to both standard and specialty markets means they can serve established contractors and emerging ones alike, including those with prior losses, credit challenges, or niche project types.

For contractors evaluating options, the difference shows up most when a bond is difficult to place — and that's exactly when the depth of a specialist's carrier relationships matters most.

Conclusion

A surety bond agent is not an administrative middleman. They are an active advocate whose expertise, surety relationships, and financial insight directly shape how much bonded work a contractor can pursue and on what terms.

Contractors who invest in the right bonding partner early are better positioned to grow their bonding capacity, qualify for larger projects, and avoid the financial missteps that erode bonding capacity before a contractor realizes the damage. That makes the choice of bonding partner one of the more consequential early decisions in a contractor's growth.

If you're looking to establish or expand a bonding program, Atlantic Coast Surety is a bond-only wholesale broker with 20+ years placing contract and commercial bonds through A-rated, T-listed surety markets. The firm works directly with contractors to structure programs around their financials and project pipeline. Contact Anthony M. Spina at aspina@acsbonding.com or call 201.661.2381 to discuss your situation.

Frequently Asked Questions

How much does a contractor surety bond cost?

According to NASBP, performance and payment bond premiums typically run 0.5%–3% of the contract price. Actual rates depend on the contractor's credit, financial strength, bonding history, and the type of bond. A surety bond agent can obtain quotes from multiple markets to find competitive rates.

What are the three C's a surety considers before bonding a contractor?

The three C's are Character (integrity and reputation), Capacity (ability to complete the work based on experience and resources), and Capital (financial strength as shown through statements and net worth). A surety bond agent helps contractors present each of these effectively before the underwriter ever sees the file.

Do I need a surety bond agent, or can I go directly to a surety company?

Most surety companies require or strongly prefer working through a licensed agent. Going through an agent gives the contractor an advocate who can shop multiple markets, present the submission strategically, and negotiate capacity — approaching underwriters directly often results in declinations that are hard to reverse.

What is the difference between a surety bond agent and a surety company?

The surety company financially backs the bond and pays claims if the contractor defaults. The agent is the licensed intermediary who represents the contractor, prepares the submission, and negotiates with the surety on the contractor's behalf.

What information does a surety bond agent need from a contractor?

Core items typically include:

- CPA-prepared company financial statements

- Work-in-progress schedule

- Personal financial statements from all owners

- Three months of bank statements

- Corporate tax return and project history with references

- Details about the specific bond being requested

How do I find a good surety bond agent?

Look for agents who specialize in construction bonding, hold valid state licenses, work with multiple surety markets, and can provide references from other contractors. Avoid defaulting to whoever handles your general business insurance — a bond-only specialist knows surety underwriting, carrier relationships, and submission strategy in ways a generalist typically does not.