They're not the same product. Not even close.

Getting this wrong has real consequences: a surety bond cannot satisfy an insurance requirement, and insurance cannot substitute for a bond. Misidentifying which product you need can leave you non-compliant, financially exposed, or paying for coverage that doesn't actually protect what you think it does.

This article breaks down what each product is, how they differ across six key dimensions, and how to determine what your business actually needs.

Key Takeaways

- Surety bonds are three-party agreements guaranteeing performance to an obligee; insurance is a two-party contract protecting the policyholder against loss

- Insurance transfers risk to the insurer permanently — if a claim is paid, you owe nothing more

- Unlike insurance, bond claims must be repaid by the principal — bonds work more like a guaranteed line of credit

- Bond underwriting assumes zero claims will occur; insurance pricing is built around the certainty that losses will happen

- Most contractors and licensed businesses need both: bonds satisfy third-party obligations, while insurance covers their own losses

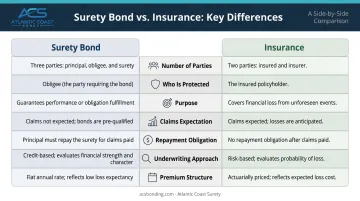

Surety Bonds vs. Insurance: Quick Comparison

The table below breaks down the core differences across seven key dimensions:

| Dimension | Surety Bond | Insurance |

|---|---|---|

| Number of parties | 3 (principal, obligee, surety) | 2 (insurer and insured) |

| Who is protected | The obligee (third party) | The policyholder |

| Purpose | Guarantees performance or payment | Transfers risk of financial loss |

| Claims expectation | No claim expected | Losses are expected and priced in |

| Repayment obligation | Principal must repay the surety | No repayment after claim |

| Underwriting approach | Credit-based, selective | Actuarial, portfolio-based |

| Premium structure | Single upfront payment per bond term | Recurring (monthly or annual) |

Both products require a premium payment and can be obtained through a licensed professional. Beyond that, the two products operate on fundamentally different principles — and confusing them can lead to costly gaps in protection.

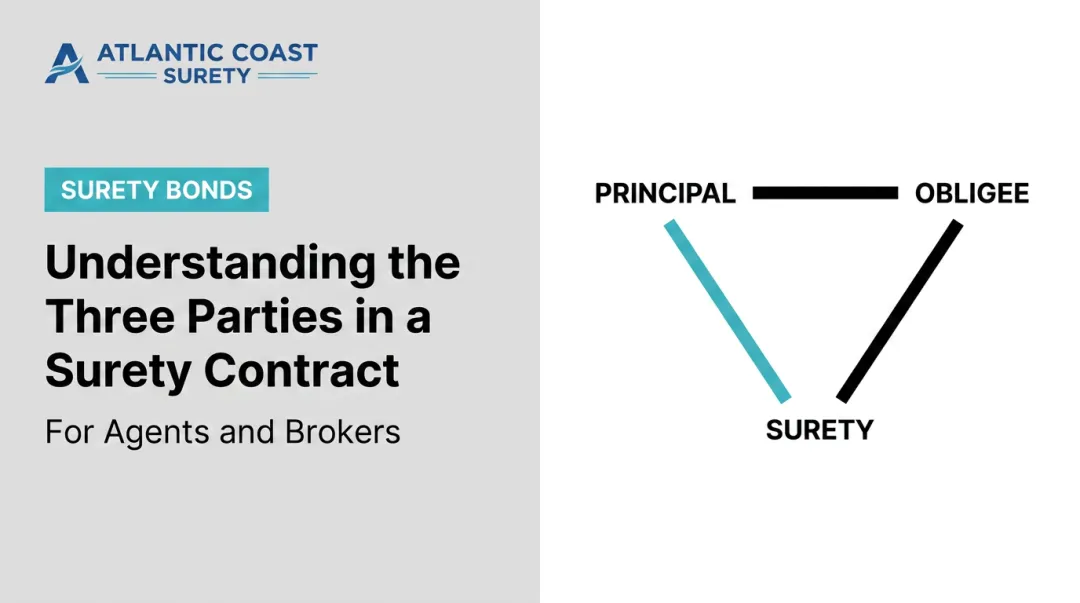

What Is a Surety Bond?

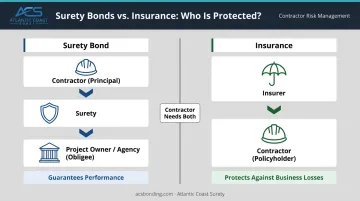

A surety bond is a legally binding three-party agreement. The surety (the bonding company) guarantees to the obligee (a project owner, government agency, or other third party) that the principal (the contractor or business) will fulfill a specific contractual or legal obligation.

The principal applies for the bond, pays the premium, and signs an indemnity agreement. That indemnity agreement is the defining feature: if the surety ever pays out a claim, the principal is legally required to reimburse the surety in full. This is why NASBP describes surety underwriting as a form of credit, much like a lending arrangement. The surety is extending trust, not absorbing risk.

Types of Surety Bonds

The four major categories cover most business scenarios:

- Contract bonds — bid bonds, performance bonds, and payment bonds used in construction and public projects

- Commercial/license & permit bonds — required by government agencies for business licensing (contractor compliance bonds, BMC-84 freight broker bonds, and similar)

- Fidelity bonds — protect against employee dishonesty, including ERISA fidelity bonds required for employee benefit plan fiduciaries

- Specialty bonds — subdivision improvement bonds, court and probate bonds, wage and welfare bonds, and others

How Surety Underwriting Works

Surety underwriting is not actuarial. The surety evaluates the specific applicant's financial strength, credit history, business experience, and track record, with the expectation that no claim will ever be filed. It's closer to a mortgage application than a standard insurance application.

That distinction matters when choosing who places your bond. Atlantic Coast Surety is a bond-only wholesale broker with 20+ years of experience and in-house underwriting authority across its full bond portfolio, providing faster decisions and access to both standard and specialty markets through A-rated, T-listed carriers.

When a Surety Bond Is Required

Common scenarios include:

- Contractors bidding on federal construction projects (performance and payment bonds are legally required under 40 U.S.C. § 3131 for contracts over $100,000)

- Businesses obtaining state or municipal licenses

- ERISA plan fiduciaries, who must carry a fidelity bond equal to at least 10% of funds handled (minimum $1,000, capped at $500,000 generally)

- Subdivision developers posting improvement bonds with local governments

A single business can carry multiple bonds simultaneously — each tied to a specific project, license, or obligation rather than providing blanket coverage.

What Is Insurance?

Insurance is a two-party contract between a policyholder and an insurer. The insurer agrees to pay for covered losses in exchange for a premium. Unlike surety bonds, there is no repayment obligation — risk is fully transferred to the insurer.

Premiums from many policyholders are pooled to fund future claims. As the Insurance Information Institute explains, insurance works by distributing the large losses of a few across a large number of premium payers. Losses are expected and factored into pricing from the start — this is what makes insurance an actuarial product rather than a credit product.

Common Business Insurance Types

For contractors and commercial businesses, the most relevant policies include:

- General liability — covers third-party bodily injury and property damage

- Commercial auto — covers vehicles used in business operations

- Workers' compensation — covers employee injuries on the job

- Errors and omissions (E&O) — covers professional mistakes or negligent advice

- Inland marine — covers tools, equipment, and materials in transit

- Business income interruption — covers lost revenue when operations are disrupted

Each policy is tailored to the business's operations and activates when a covered loss actually occurs. That distinction — absorbing loss rather than guaranteeing performance — is what separates insurance from surety bonds.

The Key Differences Between Surety Bonds and Insurance

Who Is Actually Protected

This is the most fundamental difference. Insurance protects the policyholder — the business that bought the policy. A surety bond protects the obligee — the project owner, government agency, or third party that required the bond.

The contractor who purchases a performance bond receives no financial benefit if a claim is paid — the bond pays the project owner directly.

Repayment Obligation After a Claim

With insurance, a paid claim ends the financial transaction (subject to deductibles). With a surety bond, a paid claim is just the beginning of the principal's obligation.

Under the indemnity agreement, the principal must reimburse the surety for the full claim amount. The surety may also pursue personal guarantees from the business owner — and in some cases, their spouse. Bond claims are costly, reputationally damaging, and not "absorbed" by the surety the way insurance losses are.

What Triggers a Claim

- Insurance claims are triggered by a covered incident: an accident, injury, property damage, or professional error

- Surety bond claims are triggered by failure to perform — project abandonment, insolvency, or failure to pay subcontractors and suppliers. No physical damage needs to occur

Underwriting Philosophy

Insurance underwriting accepts a broad pool of risks and prices premiums to cover expected losses across that pool. Surety underwriting is selective and credit-based — each applicant is evaluated individually with the expectation that no claim will ever be filed.

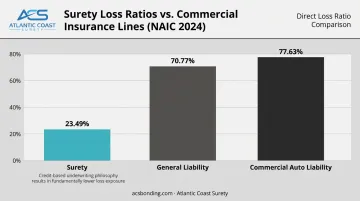

The numbers bear this out. NAIC's 2024 market share data shows surety's direct loss ratio was 23.49%, compared to 77.63% for commercial auto liability and 70.77% for general liability. The surety market is underwriting against the near-elimination of losses, not the absorption of them.

Premium Structure

- Insurance premiums recur monthly or annually as an ongoing business expense

- Surety bond premiums are typically a one-time upfront payment per bond term, calculated as a percentage of the bond's face value

According to NASBP, surety premiums generally range from 0.5% to 3% of the bond amount for most applicants — meaning a $50,000 bond typically costs $250 to $1,500 upfront. Applicants with stronger financials qualify for better rates; those with limited credit or financial history may be directed to specialty market options.

Scope and Specificity

Insurance policies are broad — designed to cover a business's general operations over a policy period. Surety bonds are highly specific: each bond is issued for a particular project, obligation, or license.

A contractor may simultaneously hold a performance bond on one project, a payment bond on another, and a license compliance bond for municipal work — each covering a distinct obligation.

Which Do You Need — A Surety Bond, Insurance, or Both?

The answer depends entirely on who is asking and what they're requiring.

| Situation | What You Need |

|---|---|

| Government agency requires a performance bond for a project | Surety bond |

| Client contract requires proof of general liability | Insurance |

| Federal construction contract over $100,000 | Both (bonds required by law; insurance required by contract) |

| State requires a license bond to operate | Surety bond |

| Business needs protection against on-site accidents | Insurance |

| Contractor working on public or commercial projects | Both |

For Contractors

Most contractors working on commercial or government projects need both products — and neither can substitute for the other. Performance and payment bonds satisfy the project owner's or agency's requirement that the contractor will perform. General liability and workers' compensation insurance protect the contractor's own business from losses.

The two products serve different stakeholders and cover different risks. Using one in place of the other leads to non-compliance, unprotected exposure, or both.

For Commercial Businesses and License Holders

Businesses like waste haulers, auto dealers, mortgage brokers, and freight brokers often carry a license and permit bond (required by a regulator or municipality) alongside separate commercial insurance. The bond protects the licensing body or public; the insurance protects the business itself.

Choose a surety bond when you need to prove to a third party that you will fulfill an obligation. Choose insurance when you need to protect your own business from unexpected losses. For most contractors and licensed commercial businesses, the answer is both — each product handles a different obligation, and neither can cover what the other is designed to do.

Frequently Asked Questions

Is a surety bond the same as an insurance contract?

No. A surety bond is a three-party guarantee that protects the obligee (a third party), while insurance is a two-party contract that protects the policyholder. The key distinction is repayment: if a surety pays a bond claim, the principal must repay the surety in full. Insurance claims require no such repayment.

How much do you pay on a $50,000 surety bond?

Using NASBP's published premium range of 0.5% to 3%, a $50,000 bond typically costs between $250 and $1,500 upfront as a one-time premium. Applicants with strong financials qualify for rates at the lower end; those with limited credit history or capitalization generally pay more or may need to go through a non-standard surety carrier.

Can a surety bond replace insurance?

No. They protect different parties and cover entirely different risks. A surety bond satisfies a third party's requirement for performance assurance; insurance protects your own business from unexpected losses. Most contractors and licensed businesses need both, and no regulatory or contractual requirement for one will be satisfied by the other.

Who pays the surety bond premium — the contractor or the project owner?

The principal — the contractor or business being bonded — purchases the bond and pays the premium, even though the bond protects the obligee. Contractors typically factor the bond cost into their project bid.

What happens if a surety bond claim is filed?

The surety investigates and, if the claim is valid, may pay the obligee up to the bond's face value. The principal is then obligated to reimburse the surety in full under the indemnity agreement. Unlike insurance, this repayment obligation carries real financial and reputational consequences for the principal.

Do contractors need both a surety bond and business insurance?

Yes, in most cases. Bonds are required by project owners or government agencies to guarantee performance; insurance protects the contractor's business from liability, injuries, and property losses. The two products address different risks for different stakeholders and are designed to work alongside each other, not replace one another.