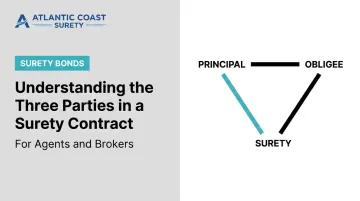

Many contractors, fiduciaries, and licensed professionals encounter surety bonds as a requirement without fully understanding the legal structure behind them. That gap matters: the three-party design determines who pays premiums, who receives protection, and who is on the hook if a claim is filed.

This article breaks down each party — the principal, the obligee, and the surety — defining their roles, responsibilities, and how they interact across real bond scenarios, from municipal construction projects to probate court appointments.

Key Takeaways

- A surety bond is a tripartite contract: the principal performs, the obligee is protected, and the surety guarantees.

- The principal pays the premium but receives no personal coverage — the bond protects the obligee.

- Unlike insurance, surety bonds include an indemnity agreement — the principal must reimburse the surety for any claims paid.

- Obligees range from federal agencies to probate courts to private project owners, depending on bond type.

- A-rated, Treasury-listed sureties ensure the financial guarantee behind any bond is credible and enforceable.

What Makes a Surety Bond a Three-Party Agreement

As defined by the SFAA, a surety bond is a written agreement guaranteeing performance, payment, or compliance by one party to another — with a third party standing behind that guarantee. The three parties are the principal, the obligee, and the surety.

This tripartite structure is what sets surety bonds apart from standard contracts or insurance policies. In a typical two-party contract, both parties bear their own risk. In a surety bond, the surety steps between them — guaranteeing the principal's performance to the obligee.

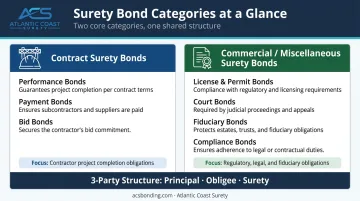

Two Broad Bond Categories

Surety bonds generally fall into two categories:

- Contract surety bonds — primarily construction-related, guaranteeing that contractors will complete work and pay subcontractors and suppliers

- Commercial (miscellaneous) surety bonds — required by statute, regulation, or ordinance, including license and permit bonds, court bonds, fiduciary bonds, and compliance bonds

The three-party structure appears in both categories. A municipality requiring a developer to post a subdivision bond, a probate court appointing an estate administrator, a licensing board requiring a waste hauler to carry a compliance bond — in every case, the same three roles are present. The specific entities filling those roles vary by bond type, but the underlying legal framework remains consistent across all of them.

The Principal: The Party with the Obligation

The principal is the party required to obtain the bond. Typically a contractor, licensed business, or court-appointed fiduciary, the principal is the one whose performance is being guaranteed.

A key point many principals miss: they pay the premium, but the bond doesn't protect them. It protects the obligee. The principal's obligation runs to the obligee — the bond simply guarantees the obligee that obligation will be met.

What the Underwriting Review Covers

Before issuing a bond, the surety evaluates whether the principal is a creditworthy risk. According to NASBP, this prequalification process reviews financial strength and the ability to perform, covering:

- Financial statements (balance sheet, income statement, cash flow) for the past three years

- Corporate and personal bank statements

- Tax returns and work-in-progress schedules

- Business references, key personnel resumes, and prior bonding history

At Atlantic Coast Surety, the underwriting process for contractor principals is equally comprehensive , covering ownership structure, bonding history, largest completed contracts, subcontracting practices, and detailed project financing data. Once a full underwriting package is on file, Atlantic Coast Surety can establish a bond line that makes future bond requests significantly faster to process.

The Indemnity Agreement: The Critical Document

After underwriting, the principal signs a General Indemnity Agreement (GIA) , and this is what makes surety structurally different from insurance.

As explained by NASBP, the GIA obligates the principal (and any co-indemnitors) to reimburse the surety in full for any claims paid, including attorneys' fees, expenses, and costs. The agreement can also grant the surety rights to contract funds, equipment, materials, accounts receivable, and real property.

At Atlantic Coast Surety, personal indemnity is typically required from all business owners, meaning individual liability extends beyond the corporate entity. Think of it like a mortgage application in reverse: the financial scrutiny is just as deep, but there's no collateral securing the bond if the surety gets the underwriting decision wrong.

Common Principal Types

- Contractors bidding on public works projects

- Waste haulers required to post license bonds for municipal compliance

- Estate administrators and executors appointed by probate courts

- Subdivision developers bonding site improvements for municipalities

- ERISA plan fiduciaries handling employee benefit plan assets

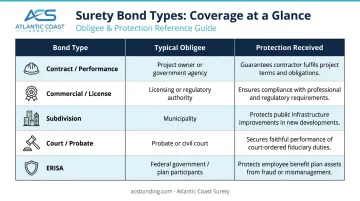

The Obligee: The Party Seeking Protection

The obligee is the party requiring the bond — and the party protected if the principal fails to perform. The obligee doesn't pay for the bond; they set the requirement and receive the financial guarantee.

Obligee Types Across Bond Categories

Obligees vary widely depending on the bond type:

| Bond Type | Typical Obligee | Protection Received |

|---|---|---|

| Contract / Performance | Project owner or government agency | Completion of contracted work; payment to subcontractors |

| Commercial / License | Licensing or regulatory authority | Contractor compliance with license terms |

| Subdivision | Municipality | Completion of required site improvements |

| Court / Probate | Probate or civil court | Faithful performance of fiduciary duties |

| ERISA | Federal government / plan participants | Protection against fraud or dishonesty by plan handlers |

What the Obligee Actually Receives

When the obligee requires a bond, they are transferring the financial risk of the principal's non-performance to the surety. If the principal defaults, the obligee can file a claim with the surety and receive compensation up to the full bond penalty amount.

For federal construction contracts, the Miller Act under 40 U.S.C. 3131 requires performance and payment bonds on contracts exceeding $100,000 for public buildings or public works. For ERISA plans, 29 U.S.C. 1112 mandates bond coverage equal to 10% of funds handled — minimum $1,000, maximum $500,000 (or $1,000,000 for plans holding employer securities).

That claim right is what gives the bond its practical value. A bond without an enforceable claim mechanism is just paperwork — the obligee's ability to collect is what makes the guarantee real.

The Surety: The Guarantor Behind the Bond

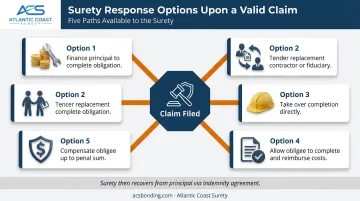

The surety is the bonding company that issues the bond and stands behind the financial guarantee. If the principal defaults and a valid claim is filed, the surety is required to act — either arranging for the obligation to be fulfilled or compensating the obligee up to the bond's penal sum.

What the Surety Does During Underwriting

The surety's prequalification process is a core benefit to the obligee, not just an internal risk check. By thoroughly evaluating the principal's qualifications before issuing a bond, the surety reduces the likelihood that a claim will ever be filed. The AGC/NASBP claims guide notes that the principal remains primarily liable while the surety is secondarily liable — meaning the surety's guarantee only activates when the principal has already failed.

When a valid claim is filed, the surety may:

- Finance the principal to help them complete the obligation

- Find and tender a replacement contractor or fiduciary

- Take over completion directly

- Allow the obligee to complete the work and reimburse the costs

- Compensate the obligee up to the bond's penal sum

After paying a claim, the surety pursues reimbursement from the principal under the indemnity agreement. The surety is fronting the payment temporarily — not absorbing the final loss. That distinction matters because it also explains why the surety's own financial strength is critical: a carrier that can't pay is no guarantee at all.

Why A-Rated and T-Listed Carriers Matter

Not all sureties carry the same financial weight. Principals and obligees alike should verify that their bonding company is:

- AM Best A-rated: independently verified financial strength, confirming the carrier can meet its obligations when claims arise

- Treasury-listed (T-listed): holds a Certificate of Authority from the Bureau of the Fiscal Service to write federal bonds under Treasury Circular 570

Atlantic Coast Surety works exclusively with A-rated and Treasury-listed surety providers. For retail brokers placing bonds through Atlantic Coast Surety, that carrier standard applies across the board — whether the bond is a performance bond on a $2 million construction contract or an ERISA fidelity bond for a small employee benefit plan.

How All Three Parties Interact: A Real-World Example

The three-party structure is clearest in a specific scenario. Consider a contractor bonded for a municipal road improvement project:

- The obligee acts first. The municipality requires a performance bond as a condition of awarding the contract. Without the bond, the contractor cannot proceed.

- The principal applies. The contractor submits a full underwriting package — financial statements, work history, contract details, bid results, and an indemnity agreement — to the surety through their broker.

- The surety underwrites and issues. After reviewing the contractor's financials and project details, the surety issues the bond. The contractor pays the premium.

- Default scenario. If the contractor abandons the project mid-construction, the municipality files a claim. The surety investigates, then either arranges for a replacement contractor or compensates the municipality up to the bond amount. The surety then pursues the original contractor for full repayment under the indemnity agreement.

The same three-party structure applies across other bond types:

- Probate bond: A probate court (obligee) requires an estate executor (principal) to post a bond before accessing estate assets. If the executor mismanages funds, the court and beneficiaries have a claim against the bond.

- Subdivision bond: A municipality (obligee) requires a developer (principal) to bond required site improvements. The bond amount is set by the municipal engineer's cost estimate. If the developer fails to complete roads or utilities, the municipality can draw on the bond to fund completion.

- Waste hauler license bond: A licensing board (obligee) requires a waste hauler (principal) to post a compliance bond as a condition of licensure. Violations of license terms give the board grounds to file a claim.

The bond type changes — the underlying mechanics don't. What shifts is the industry context, the claim trigger, and the dollar exposure involved.

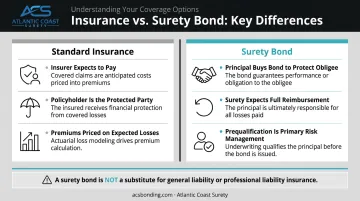

Surety Bonds vs. Insurance: A Key Distinction

Surety bonds and insurance share some surface similarities, but they work differently in ways that matter for risk planning.

In a standard insurance contract:

- The insurer expects to pay covered claims

- The policyholder is the protected party

- Premiums are actuarially priced based on expected losses

In a surety bond:

- The principal purchases the bond to protect the obligee — not themselves

- The surety does not expect to absorb losses; it expects reimbursement from the principal

- Prequalification, not actuarial pricing, is the primary risk management tool

As NASBP notes, surety companies require a signed indemnity agreement precisely because they don't expect to bear the final loss. The GIA is the mechanism that makes the principal — not the surety — responsible for any claims paid.

This distinction has a direct practical consequence: a surety bond is not a substitute for general liability or professional liability insurance. Many principals need both. A performance bond protects the project owner if a contractor defaults. It does not protect the contractor from a negligence claim, a job-site injury, or property damage. Knowing exactly what the bond covers — and who it protects — prevents gaps in a complete risk management program.

Frequently Asked Questions

Who are the three parties in a surety bond?

The three parties are the principal (the party required to perform and who obtains the bond), the obligee (the party requiring the bond and receiving its protection), and the surety (the bonding company guaranteeing the principal's performance to the obligee).

Who is the obligee on a surety bond?

The obligee is the party protected by the bond — most commonly a government agency, project owner, court, or licensing authority. The obligee sets the bonding requirement and has the right to file a claim if the principal fails to perform.

What is a 3rd party surety bond?

"3rd party surety bond" is an informal name for the standard surety structure — it simply refers to the surety company acting as the third party that guarantees the principal's performance to the obligee. All surety bonds follow this three-party design.

What is the difference between a surety bond and insurance?

Insurance protects the policyholder from covered losses, and the insurer expects to pay valid claims. A surety bond protects the obligee. Unlike insurance, the principal is contractually required to reimburse the surety for any claims paid under the indemnity agreement.

What happens when a principal fails to perform on a surety bond?

The obligee files a claim with the surety. If valid, the surety either remedies the situation directly (such as arranging project completion) or compensates the obligee up to the bond's penal sum. The surety then recovers that full amount from the principal under the indemnity agreement, which requires the principal to cover all costs paid.