Introduction

A newly appointed trustee often doesn't realize they can't touch a single asset until they post a bond. Courts and trust documents routinely require one before a trustee can begin managing property, whether the appointment comes through a will, a court order, or a private trust agreement.

The problem is that many newly appointed trustees don't fully understand what a trustee bond actually guarantees, how a claim works, or what their personal financial exposure is. This confusion leads to delays in the appointment process and costly missteps.

This guide covers exactly what a trustee bond is, how it operates from issuance through claims, who needs one, and how to get it.

TL;DR

- A trustee bond is a fiduciary surety bond guaranteeing that a trustee will faithfully manage trust assets according to law and the trust's terms

- Three parties are bound: the trustee, the beneficiaries or court, and the surety company

- If a trustee mismanages or misappropriates assets, harmed parties can file a claim to recover losses

- Unlike insurance, the trustee must personally repay the surety for any claims paid out

- Premiums are a small percentage of the court-set bond amount, which is based on the trust's total value

What Is a Trustee Bond?

A trustee bond is a type of fiduciary (probate) surety bond — a legally binding three-party contract in which a surety company guarantees to the obligee (a court or the beneficiaries) that the trustee will perform their duties honestly, lawfully, and in accordance with the trust's terms.

As NASBP defines it, fiduciary bonds are "required of those who administer a trust under court supervision." The Surety & Fidelity Association of America (SFAA) frames them as bonds "given by a Court Fiduciary to secure the faithful performance of fiduciaries' duties and compliance with the orders of the court having jurisdiction."

Why It Exists

Trustees hold legal control over assets that belong to someone else — the beneficiaries. The bond closes the accountability gap. If a trustee steals funds, invests recklessly, or otherwise breaches fiduciary duty, there's a financial remedy available to the beneficiaries.

A trustee bond does not protect the trustee — it protects the beneficiaries and the estate. Unlike insurance, the trustee bears the ultimate financial liability for any claims paid. The surety steps in temporarily, then recovers every dollar from the trustee.

When Trustee Bonds Are Required

That protection requirement surfaces across several trust contexts:

- Testamentary trust trustees — appointed under a will after the grantor's death

- Living trust trustees whose trust document or a court mandates bonding

- Bankruptcy trustees, federally regulated under 11 U.S.C. § 322

- Special needs trust trustees managing long-term care assets for vulnerable beneficiaries

When a Bond Can Be Waived

Under Uniform Trust Code Section 702, a bond is required only if the court finds it necessary to protect beneficiaries, or if the trust terms require it and the court hasn't dispensed with that requirement.

A trust document can explicitly waive bonding — but courts retain discretion to require one if circumstances warrant it.

How Does a Trustee Bond Work?

A trustee bond operates as a continuous financial guarantee across three phases: issuance, active coverage, and claims. Each phase determines what the bond does — and doesn't — protect against.

Getting the Bond

Before a trustee can serve, they must obtain the bond and file it with the court. The process involves:

- Complete a bond application — the surety requires personal information, background details, and information about the trust estate

- Submit documentation — a copy of the court order or trust agreement establishing the bond requirement, plus an estate assets breakdown covering cash, securities, real property, and liabilities

- Underwriting review — the surety assesses the applicant's creditworthiness and the nature of the trust to determine the premium rate

- Pay the premium — once approved, the trustee pays the bond premium and files the bond with the court

Courts set the bond amount based on their assessment of what's needed to protect beneficiaries — typically tied to the overall value of the trust estate being managed, though statutes in states like California, Florida, Texas, and Illinois give courts discretion to specify the exact amount, increase it, or reduce it over time.

Active Coverage and What It Guarantees

While active, the bond covers the trustee's faithful performance of fiduciary duties. The Uniform Trust Code defines those duties as good-faith administration, loyalty to beneficiaries, prudent investment, and proper control and protection of trust property.

Types of misconduct that can trigger a claim:

- Theft or misappropriation of trust funds

- Self-dealing or undisclosed conflicts of interest

- Reckless or imprudent investment decisions

- Failure to follow the trust's distribution terms

- Failure to maintain proper accounting records

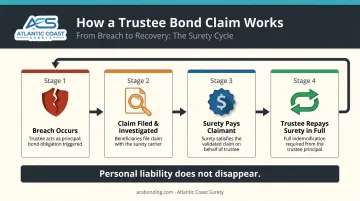

How a claim works: Beneficiaries or interested parties who suspect a breach file a claim with the surety. The surety investigates and, if the claim is valid, pays the claimant up to the full bond amount.

Once the surety pays, the trustee is legally obligated to reimburse the surety in full — plus interest and fees. This indemnification obligation is what makes a surety bond a genuine accountability tool, not a safety net. The trustee's personal financial exposure doesn't disappear just because the surety paid.

Renewal and Termination

Trustee bonds are issued for annual terms and require renewal each year the trustee continues serving. At each renewal, the surety conducts a fresh underwriting review, and the premium may change based on updated credit history or changes in the trust's value.

Renewal premiums remain due until the bond is properly discharged. Under UTC Section 702 and similar state statutes in Florida, Texas, and Illinois, courts can modify or terminate a bond. Termination occurs when:

- The court formally discharges the trustee

- The trustee is removed or resigns and a successor is bonded

- The court otherwise orders termination

Who Needs a Trustee Bond?

Two factors drive most trustee bond requirements: whether a court is involved and what the trust document says. Understanding which applies to your situation determines whether a bond is mandatory, discretionary, or waivable.

Court-Appointed Trustees

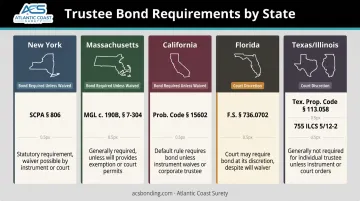

Court-appointed trustees almost universally need a bond. Requirements differ by state:

| State | Rule |

|---|---|

| New York | SCPA § 806 requires testamentary trustees to file a bond unless the will directs otherwise |

| Massachusetts | Testamentary trustees must furnish a bond with surety unless waived by trust terms or court |

| California | Bond required when the trust instrument mandates it, the court finds it necessary, or a court-appointed trustee wasn't named in the trust |

| Florida, Texas, Illinois | Follow UTC structure — bond required when the court finds it necessary or trust terms require it |

Privately Appointed Trustees

Even trustees named in a private trust document may need a bond if:

- The trust document itself mandates bonding

- The court exercises discretion to require one

- Beneficiaries petition the court for a bond requirement

Conversely, if the trust document explicitly waives bonding, that waiver may be honored — unless a court overrides it to protect beneficiaries.

Roles That Carry Heightened Bonding Obligations

- Bankruptcy trustees — under 11 U.S.C. § 322, a selected trustee must file a bond within seven days of selection

- Special needs trust trustees — responsible for long-term care assets held for individuals with disabilities; Texas Estates Code § 1301.101 requires a bond or equivalent security unless the court finds it unnecessary

- Trustees managing trusts with minor or incapacitated beneficiaries — courts take a conservative approach given the beneficiaries' inability to protect their own interests

How to Get a Trustee Bond

Here's what to expect from application to filing.

Step-by-Step

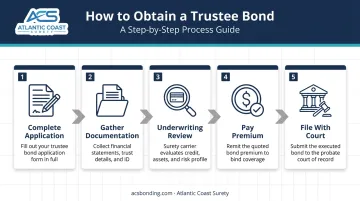

- Obtain a bond application — complete the surety's probate bond application with personal, financial, and estate details

- Gather documentation — court order or trust agreement establishing the requirement, estate assets and liabilities breakdown, and any will or trust copy

- Submit for underwriting — the surety reviews creditworthiness, background, and estate complexity

- Pay the approved premium — once underwriting is complete, pay the premium to bind coverage

- File with the court — submit the executed bond to the court or provide it to the obligee as required before beginning trustee duties

What Affects the Premium

Bond cost depends on two primary factors:

- Bond amount: Courts set this based on the trust's total value, so larger estates carry higher premiums

- Credit history: The trustee's personal credit score drives the premium rate more than any other factor — stronger credit means lower rates

Applicants with less-than-perfect credit can generally still obtain a trustee bond, though the premium reflects that added risk. Underwriters also review prior bond claims, judgments, and any criminal history involving dishonesty when making their decision.

Working With a Specialized Bond Agency

For probate fiduciaries and trustees who need to meet court deadlines, working with a bond-only agency can reduce delays significantly. Atlantic Coast Surety, a wholesale surety bond broker with 20+ years of experience, places probate and trustee bonds through A-rated, T-listed (Treasury-listed) surety carriers. Their in-house underwriting authority allows for faster decisions on time-sensitive matters, since courts typically won't confirm a trustee appointment until the bond is on file.

Atlantic Coast Surety works through retail insurance agents and attorneys. If you're an agent or attorney with a client who needs a trustee bond, you can reach their team at (201) 661-2381 or contact Anthony Spina directly at aspina@acsbonding.com.

Frequently Asked Questions

How much does a trustee bond cost?

The cost is a percentage of the total bond amount, which courts typically set based on the trust's value. The specific rate depends on the trustee's credit history — applicants with strong credit pay lower rates, while those with weaker credit pay more. Contact a surety bond specialist for an accurate quote based on your specific circumstances.

Why would a trustee need a bond?

Courts and trust documents require trustee bonds to protect beneficiaries. If a trustee mismanages, misappropriates, or otherwise breaches fiduciary duty, the bond provides a financial remedy so harmed parties can recover losses without pursuing the trustee through separate litigation alone.

What is the difference between a trustee and a surety?

The trustee is the individual appointed to manage the trust — the principal in the bond whose performance is being guaranteed. The surety is the bonding company that backs the bond and pays valid claims. The trustee must repay the surety in full for any claims paid, so personal financial liability remains.

Can a trustee bond requirement be waived?

Yes — a trust document can explicitly waive the bonding requirement, and courts often honor this. But courts retain discretion to require a bond regardless, particularly when beneficiaries petition for one or when circumstances suggest additional oversight is warranted to protect vulnerable parties.

How long does a trustee bond last?

Trustee bonds are issued in annual terms and must be renewed each year for the duration of the trustee's service. Each renewal involves a fresh underwriting review, and premiums continue until the court formally discharges the bond.

What happens if a claim is filed against a trustee bond?

The surety investigates the claim and, if valid, pays the claimant up to the bond amount. The trustee is then obligated to repay the surety in full — the bond ensures beneficiaries have a recovery path, not that the trustee escapes personal financial liability for misconduct.