Introduction

Getting declined for a contract bond doesn't always mean the project is off the table. Skilled, experienced contractors face bond declinations for reasons that have nothing to do with their ability to complete the work — a tough loss year, a credit gap, negative working capital, or a project scope that pushes past standard market limits.

Standard surety carriers underwrite to a set of benchmarks. When an applicant falls outside those benchmarks, they decline. What most standard carriers won't do is work through mitigation options — that's a conversation that only happens with specialists who know where the tools exist.

This article covers 8 solutions surety specialists use to get hard-to-place contract bonds written, including funds control, collateral arrangements, sub back bonds, and contract restructuring.

TL;DR

- Funds control and collateral are the most widely used tools to reduce surety exposure when a contractor's financials raise concerns

- The SBA Surety Bond Guarantee Program backs bonds for small contractors who can't qualify through standard markets — up to $9 million, or $14 million on federal contracts

- Structural solutions — sub back bonds, cosigners, and breaking up contracts — address risk at the project level, not just the financial level

- Combinations work best: most hard-to-place situations call for more than one tool at once

What Makes a Contract Bond "Hard to Place"?

A hard-to-place contract bond is a performance, payment, or bid bond that standard surety carriers decline to write because the contractor or project falls outside their normal underwriting appetite. NASBP calls this "non-standard underwriting" — accounts that don't meet the full criteria expected in a standard market submission.

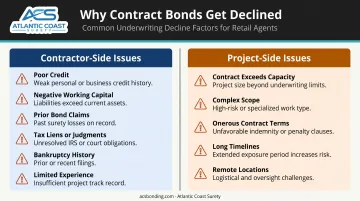

Contractor-Side Issues

These are the most common triggers for a declination:

- Poor personal or business credit

- Negative or insufficient working capital (NASBP benchmarks working capital at roughly 10% of the requested bonding program)

- Prior bond claims or defaults

- Tax liens or judgments

- Bankruptcy history

- Limited years in business or narrow project experience

Project-Side Issues

Some bonds are hard to place because of the job itself, not the contractor:

- Contract value that exceeds the contractor's current capacity

- Unusually complex or unfamiliar scope

- Onerous contract terms

- Long completion timelines

- Unique or remote project locations

Both types of issues can exist simultaneously. That raises the difficulty, but a hard-to-place bond is rarely an unplaceable one. Specialty market access and the right risk-mitigation tools can still get it written.

Solutions 1–4: Financial and Collateral-Based Tools

Solution 1: Funds Control

Funds control (also called funds administration) redirects project payments through a third-party administrator who controls how money flows on the job. Instead of contract proceeds going directly to the contractor, they go into a separate account managed by the administrator, who then disburses payments to subcontractors, suppliers, and labor based on approved invoices.

According to NASBP, when a surety can control and mitigate payment risk, it becomes more willing to issue bonds it might otherwise decline.

Funds control is typically required when a contractor has:

- Negative or thin working capital

- A history of payment issues on prior jobs

- Cash management concerns noted during underwriting

- Financial instability that stops short of being disqualifying

It can be used on its own or paired with collateral for additional protection. The key appeal to the surety: even if the contractor's cash management is questionable, the money stays on the project.

Solution 2: Collateral

Where funds control manages cash flow, collateral gives the surety a direct claim on assets if a performance or payment failure occurs. Common forms include:

- Cash deposits held by the surety for the bond's duration

- Irrevocable Letters of Credit (ILOC) from the contractor's bank

- Free-and-clear real estate (though most carriers prefer cash or ILOC due to the complexity of liquidating property)

Collateral is held until the bond is released at project completion. Like a security deposit, it lowers the surety's net exposure without changing the bond's face amount.

The amount of collateral required varies by carrier and by the degree of risk — some situations may call for partial collateral while others require dollar-for-dollar coverage of the bond amount.

Solution 3: Irrevocable Letter of Credit (ILOC)

An ILOC is a written bank commitment guaranteeing that the surety will be paid if a valid claim is made. The contractor's bank (not the contractor) stands behind the payment obligation, making it one of the most effective risk offsets available.

Key characteristics:

- Must be issued on a surety-required form with a specific expiration date

- The bank's obligation to pay is independent of the contractor's performance on the underlying contract

- A draw on the ILOC converts to a loan from the bank to the contractor

The tradeoff: an ILOC ties up a contractor's bank line of credit. It's best suited for contractors who have adequate credit capacity with their bank but don't have the liquidity to post a cash deposit directly.

Solution 4: SBA Surety Bond Guarantee Program

The SBA Surety Bond Guarantee (SBG) Program was created specifically for small businesses that can't qualify through standard surety markets. The SBA guarantees a portion of the bond to the surety, reducing the carrier's risk exposure enough to write accounts they'd otherwise decline.

Current program limits (as of 2025):

- Up to $9 million for general contracts and subcontracts

- Up to $14 million for federal contracts, when a contracting officer certifies the guarantee is necessary

SBA guarantee percentages:

- 90% for contracts up to $100,000, and for 8(a), HUBZone, Veteran-Owned, and Service-Disabled Veteran-Owned small businesses

- 80% for all other contracts

SBA fees: Performance and payment bond guarantees carry a small business fee of 0.6% of the contract price. Bid bond guarantees have no SBA fee.

One notable advantage: the bond looks identical to a standard bond. The project owner has no visibility into the SBA guarantee behind it — an important consideration for emerging contractors who don't want their financial limitations visible during bidding.

In FY2025, the SBA reported $10.6 billion in guarantees supporting over 2,200 small businesses through this program. Contractors must work through an SBA-authorized surety agent to access it.

Solutions 5–8: Structural and Relationship-Based Tools

Solution 5: Cosigner (Additional Indemnitor)

A cosigner (called an additional indemnitor in surety terminology) is a financially stronger individual or entity who co-signs the General Indemnity Agreement (GIA). This gives the surety additional financial backing behind the principal, expanding the pool of assets it can pursue if a claim occurs.

The best cosigner candidates have:

- Direct ties to the contractor (parent company, partner, key stakeholder)

- Relevant construction or industry experience

- Demonstrable personal or corporate financial strength

A cosigner works best when the contractor has solid experience and a strong track record but doesn't yet have the financial depth to qualify independently. It's not a permanent fix — it should be paired with a plan to improve the contractor's own balance sheet over time. Cosigning the indemnity agreement carries real financial exposure, and both parties need to understand that clearly before proceeding.

Solution 6: Sub Back Bonds (Subcontractor Bonds)

Requiring subcontractors to carry their own performance and payment bonds shifts a substantial portion of project risk off a capacity-strained GC's plate and onto the subcontractors' sureties.

Consider the scale of exposure involved: NAHB data shows that builders subcontract an average of 84% of construction costs. Even in commercial work, subcontracted scope typically represents the majority of a project's total value. When subs carry their own bonds, the GC's surety is no longer the last line of defense for that portion of the work.

Sureties look favorably on GCs who have a documented subcontractor bonding policy because it signals risk management discipline — not just for the current job, but as an ongoing practice. NASBP notes that subcontract bonds also provide independent surety prequalification of each sub — financial vetting that most GCs wouldn't conduct on their own.

Sub back bonds add roughly 1%–3% to a subcontractor's bid price, so they have a cost — but for a GC trying to qualify for a bond they couldn't otherwise get, that tradeoff is often worth it.

Solution 7: Breaking Up Contracts

Sometimes the simplest fix is restructuring. If a single contract exceeds a contractor's current bonding capacity, breaking it into multiple smaller contracts — each within the contractor's bondable limit — can make an otherwise impossible bond workable.

Example: A contractor whose capacity maxes out at $500,000 per single bond cannot take a $2 million umbrella contract as written. But if the scope can be divided into four distinct $500,000 contracts (say, four separate site improvement packages), each bond is individually within reach.

This approach has real limitations:

- The contract must be divisible into genuinely independent scopes — a single building cannot be split this way

- The obligee must agree to the restructuring, which requires upfront negotiation

- It won't work for projects where the scope is inherently unified or sequential

When it does apply, it's a clean solution that requires no additional financial tools — just a cooperative obligee and a scope that lends itself to logical division.

Solution 8: Funds Administration Holdback

This solution combines funds control with a built-in collateral buffer. Standard funds administration manages all project disbursements through a third-party administrator.

The holdback layer adds a defined dollar amount — typically a retainage percentage of the contract — that stays in the funds administration account for the entire project duration. That held amount functions as built-in collateral: the surety knows a cash buffer is accessible if needed, without requiring the contractor to post separate collateral upfront.

The key distinction from standard funds control comes down to that cash buffer:

| Feature | Standard Funds Control | Funds Administration Holdback |

|---|---|---|

| Controls disbursements | ✅ Yes | ✅ Yes |

| Holds cash buffer for surety | ❌ No | ✅ Yes |

| Acts as collateral substitute | ❌ No | ✅ Yes |

This solution fits contractors who have some financial strength — enough to generate the holdback amount through the contract's retainage — but not enough to post full collateral independently. NASBP has documented that funds-control situations requiring a 10% working capital deposit produced a 0% loss ratio — a track record that explains why sureties accept this structure as a genuine collateral alternative.

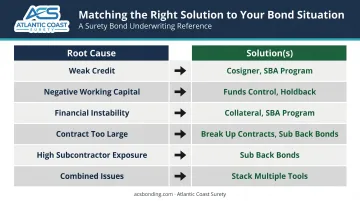

How to Match the Right Solution to Your Situation

No single tool fits every hard-to-place scenario. The right starting point is diagnosing why the bond is difficult to place.

| Root Cause | Solutions to Consider |

|---|---|

| Weak credit or credit gaps | Cosigner, SBA program |

| Negative working capital or cash flow concerns | Funds control, funds administration holdback |

| Financial instability (broader) | Collateral (cash or ILOC), SBA program |

| Contract too large for current capacity | Break up contracts, sub back bonds |

| High subcontractor exposure | Sub back bonds |

| Combination of financial + project issues | Stack multiple tools |

Combinations are common — and often necessary. A contractor with credit issues and a large project might pair the SBA program with funds control. A GC with thin working capital on a heavily subcontracted job might use funds control alongside sub back bonds.

Knowing which combination applies to your situation is where an experienced surety specialist earns their value. Atlantic Coast Surety has spent 20+ years working through standard and specialty markets to identify which tools — or combinations of tools — address a surety's specific underwriting concerns. As a bond-only wholesale agency, we have direct relationships with carriers experienced in non-standard submissions, not just standard market carriers with limited appetite for complex placements.

One practical note: don't wait until a project deadline creates pressure. Setting up funds control, arranging an ILOC with a bank, or beginning the SBA application process all take time. Proactive outreach to a surety specialist gives you that time — and when underwriters feel rushed, they reach for the easiest answer, which is often a declination.

Frequently Asked Questions

Is it difficult to get a surety bond?

For contractors with solid credit and financials, the standard process is relatively straightforward. Difficulty increases with credit issues, limited financial history, prior claims, or complex projects — the scenarios where the eight solutions in this guide directly apply.

How much does a $100,000 surety bond cost?

Surety bond premiums typically run 0.5%–3% of the contract amount, so a $100,000 bond generally costs between $500 and $3,000. Hard-to-place situations or use of the SBA program tend to push rates toward the higher end of that range.

What are the 3 C's of surety?

Sureties evaluate contractors on Character (trustworthiness and track record), Capacity (experience and ability to complete the work), and Capital (financial strength). Weakness in any one area can trigger a declination.

What is the difference between a hard-to-place bond and a standard bond?

Standard bonds go through routine underwriting for qualified applicants. Hard-to-place bonds carry elevated risk that standard carriers won't accept, so they require specialty market access, additional risk-mitigation tools, or a combination of both.

Can I use more than one solution for a hard-to-place bond?

Yes — combining solutions is common and often necessary. Pairing funds control with collateral, or using the SBA program alongside sub back bonds, is a typical approach for situations where risk exists on multiple dimensions.

Does working with a specialty surety agency improve my chances of getting bonded?

Significantly. Specialty agencies have relationships with carriers experienced in non-standard accounts and understand how to structure submissions that standard agents and standard carriers lack the market access or experience to evaluate properly.